Concept explainers

Videos

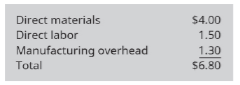

Gent Designs requires three units of part A for every unit of Al that it produces. Currently, part A is made by Gent, with these per-unit costs in a month when 4.000 units were produced:

Variable manufacturing overhead is applied at $1.00 per unit. The other $0.30 of overhead consists of allocated fixed costs. Gent will need 6,000 units of part A for the next year’s production.

Cory Corporation has offered to supply 6,000 units of part A at a price of $7.00 per unit. It Gent accepts the offer, all of the variable costs and $1,200 of the fixed costs will be avoided. Should Gent Designs accept the offer from Cory Corporation?

Want to see the full answer?

Check out a sample textbook solution

Chapter 10 Solutions

Principles of Accounting Volume 2

Additional Business Textbook Solutions

Financial Accounting (12th Edition) (What's New in Accounting)

Horngren's Financial & Managerial Accounting, The Managerial Chapters (6th Edition)

Horngren's Financial & Managerial Accounting, The Financial Chapters (6th Edition)

Horngren's Accounting (12th Edition)

Intermediate Accounting

Horngren's Financial & Managerial Accounting, The Financial Chapters (Book & Access Card)

- Remarkable Enterprises requires four units of part A for every unit of Al that it produces. Currently, part A is made by Remarkable, with these per-unit costs in a month when 4,000 units were produced: Variable manufacturing overhead is applied at $1.60 per unit. The other $0.50 of overhead consists of allocated fixed costs. Remarkable will need 8,000 units of part A for the next years production. Altoona Corporation has offered to supply 8,000 units of part A at a price of $8.00 per unit. If Remarkable accepts the offer, all of the variable costs and $2,000 of the fixed costs will be avoided. Should Remarkable accept the offer from Altoona Corporation?arrow_forwardColonels uses a traditional cost system and estimates next years overhead will be $480,000, with the estimated cost driver of 240,000 direct labor hours. It manufactures three products and estimates these costs: If the labor rate is $25 per hour, what is the per-unit cost of each product?arrow_forwardBobcat uses a traditional cost system and estimates next years overhead will be $800.000, as driven by the estimated 25,000 direct labor hours. It manufactures three products and estimates the following costs: If the labor rate is $30 per hour, what is the per-unit cost of each product?arrow_forward

- Box Springs. Inc., makes two sizes of box springs: queen and king. The direct material for the queen is $35 per unit and $55 is used in direct labor, while the direct material for the king is $55 per unit, and the labor cost is $70 per unit. Box Springs estimates it will make 4,300 queens and 3,000 kings in the next year. It estimates the overhead for each cost pool and cost driver activities as follows: How much does each unit cost to manufacture?arrow_forwardDimitri Designs has capacity to produce 30,000 desk chairs per year and is currently selling all 30,000 for $240 each. Country Enterprises has approached Dimitri to buy 800 chairs for $210 each. Dimitris normal variable cost is $165 per chair, including $50 per unit in direct labor per chair. Dimitri can produce the special order on an overtime shift, which means that direct labor would be paid overtime at 150% of the normal pay rate. The annual fixed costs will be unaffected by the special order and the contract will not disrupt any of Dimitris other operations. What will be the impact on profits of accepting the order?arrow_forwardPower Corp. makes 2 products: blades for table saws and blades for handsaws. Each product passes through the sharpening machine area, which is the chief constraint during production. Handsaw blades take 15 minutes on the sharpening machine and have a contribution margin per blade of $15. Table saw blades take 20 minutes on the sharpening machine and have a contribution margin per blade of $35. If it is assumed that Power Corp. has 5,000 hours available on the sharpening machine to service a minimum demand for each product of 4,000 units, how much will profits increase if 200 more hours of machine time can be obtained?arrow_forward

- Power Corp. makes 2 products: blades for table saws and blades for handsaws. Each product passes through the sharpening machine area, which is the chief constraint during production. Handsaw blades take 15 minutes on the sharpening machine and have a contribution margin per blade of $15. Table saw blades take 20 minutes on the sharpening machine and have a contribution margin per blade of $35. If it is assumed that Power Corp. has 5,000 hours available on the sharpening machine to service a minimum demand for each product of 4,000 units, how many of each product should be made?arrow_forwardPatz Company produces two types of machine parts: Part A and Part B, with unit contribution margins of 300 and 600, respectively. Assume initially that Patz can sell all that is produced of either component. Part A requires two hours of assembly, and B requires five hours of assembly. The firm has 300 assembly hours per week. Required: 1. Express the objective of maximizing the total contribution margin subject to the assembly-hour constraint. 2. Identify the optimal amount that should be produced of each machine part and the total contribution margin associated with this mix. 3. What if market conditions are such that Patz can sell at most 75 units of Part A and 60 units of Part B? Express the objective function with its associated constraints for this case and identify the optimal mix and its associated total contribution margin.arrow_forwardComputador has a manufacturing plant in Des Moines that has the theoretical capability to produce 243,000 laptops per quarter but currently produces 91,125 units. The conversion cost per quarter is 7,290,000. There are 60,750 production hours available within the plant per quarter. In addition to the processing minutes per unit used, the production of the laptops uses 10 minutes of move time, 20 minutes of wait time, and 5 minutes of rework time. (All work is done by cell workers.) Required: 1. Compute the theoretical and actual velocities (per hour) and the theoretical and actual cycle times (minutes per unit produced). 2. Compute the ideal and actual amounts of conversion cost assigned per laptop. 3. Calculate MCE. How does MCE relate to the conversion cost per laptop?arrow_forward

- Lander Parts, Inc., produces various automobile parts. In one plant, Lander has a manufacturing cell with the theoretical capability to produce 450,000 fuel pumps per quarter. The conversion cost per quarter is 9,000,000. There are 150,000 production hours available within the cell per quarter. Required: 1. Compute the theoretical velocity (per hour) and the theoretical cycle time (minutes per unit produced). 2. Compute the ideal amount of conversion cost that will be assigned per subassembly. 3. Suppose the actual time required to produce a fuel pump is 40 minutes. Compute the amount of conversion cost actually assigned to each unit produced. What happens to product cost if the time to produce a unit is decreased to 25 minutes? How can a firm encourage managers to reduce cycle time? Finally, discuss how this approach to assigning conversion cost can improve delivery time. 4. Assuming the actual time to produce one fuel pump is 40 minutes, calculate MCE. How much non-value-added time is being used? How much is it costing per unit? 5. Cycle time, velocity, MCE, conversion cost per unit (theoretical conversion rate actual conversion time), and non-value-added costs are all measures of performance for the cell process. Discuss the incentives provided by these measures.arrow_forwardHatch Manufacturing produces multiple machine parts. The theoretical cycle time for one of its products is 65 minutes per unit. The budgeted conversion costs for the manufacturing cell dedicated to the product are 12,960,000 per year. The total labor minutes available are 1,440,000. During the year, the cell was able to produce 0.6 units of the product per hour. Suppose also that production incentives exist to minimize unit product costs. Required: 1. Compute the theoretical conversion cost per unit. 2. Compute the applied conversion cost per minute (the amount of conversion cost actually assigned to the product). 3. Discuss how this approach to assigning conversion cost can improve delivery time performance. Explain how conversion cost acts as a performance driver for on-time deliveries.arrow_forwardOat Treats manufactures various types of cereal bars featuring oats. Simmons Cereal Company has approached Oat Treats with a proposal to sell the company its top selling oat cereal bar at a price of $27,500 for 20,000 bars. The costs shown are associated with production of 20,000 oat bars currently. The manufacturing overhead consists of $3,000 of variable costs with the balance being allocated to fixed costs. Should Oat Treats make or buy the oat bars?arrow_forward

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning

Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning