Videos

Recording Sales with Discounts and Returns and Analyzing Gross Profit Percentage

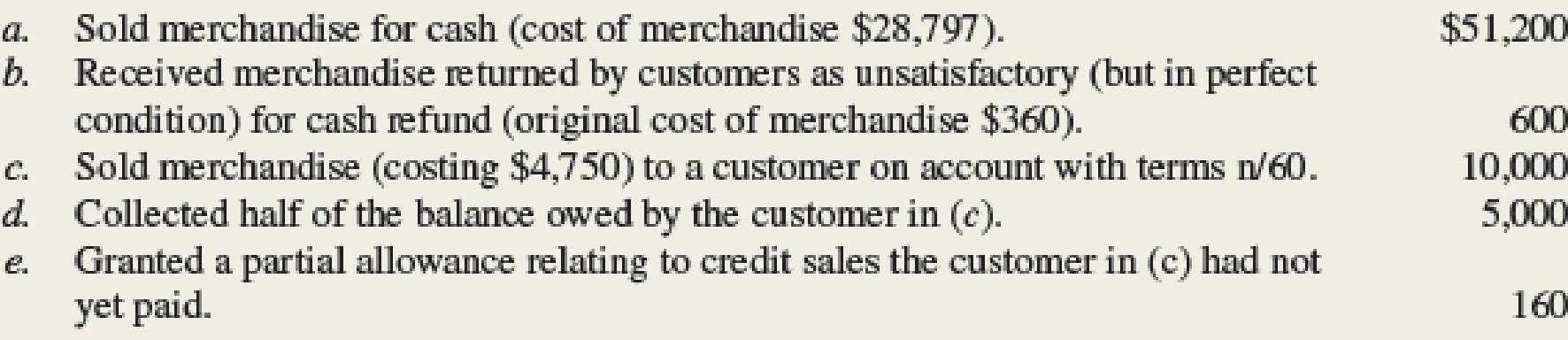

Hair World Inc. is a wholesaler of hair supplies. Hair World uses a perpetual inventory system. The following transactions (summarized) have been selected for analysis:

Required:

- 1. Compute Net Sales and Gross Profit for Hair World. No additional sales returns/allowances are expected.

- 2. Compute the gross profit percentage (using the formula shown in this chapter and rounding to one decimal place).

- 3. Prepare

journal entries to record transactions (a)–(e). - 4. Hair World is considering a contract to sell merchandise to a hair salon chain for $15,000. This merchandise will cost Hair World $10,000. Would this contract increase (or decrease) Hair World’s dollars of gross profit and its gross profit percentage?

1.

Calculate the sales revenue and gross profit of Incorporation H.

Explanation of Solution

Sales revenue:

Sales revenue is the amount received by the company from the sale of goods and services during day-to-day operations of the company within specified period of time.

Gross Profit:

Gross Profit is the difference between the net sales, and the cost of goods sold. Gross profit usually appears on the income statement of the company.

Calculate the sales revenue and gross profit of Incorporation H as follows:

| Particulars | Amount($) |

| Sales Revenue (1) | 61,200 |

| Less: Sales Returns and Allowances(2) | (760) |

| Net Sales | 60,440 |

| Less: Cost of Goods Sold (3) | 33,187 |

| Gross Profit | 27,253 |

Table (1)

Working note 1:

Calculate the value of sales revenue:

Working note 2:

Calculate the sales returns and allowances:

Working note 3:

Calculate the cost of goods sold:

Therefore, the net sales and gross profit of Incorporation H are $60,440 and $27,253 respectively.

2.

Calculate the gross profit percentage of Incorporation H.

Explanation of Solution

Gross Profit Percentage:

Gross profit is the financial ratio that shows the relationship between the gross profit and net sales. It represents gross profit as a percentage of net sales. Gross Profit is the difference between the net sales revenue, and the cost of goods sold. It can be calculated by dividing gross profit and net sales.

Calculate the gross profit percentage of Incorporation H as follows:

Therefore, the gross profit percentage of Incorporation H is 45.1%.

3.

Prepare journal entries to record the transaction from (a) to (e).

Explanation of Solution

Journal Entry:

Journal entry is the method of recording monetary business transactions in chronological order. It records the debit and credit aspects of each transaction to abide by the double-entry system.

Prepare journal entries to record the transaction from (a) to (e) as follows:

a. Record the sales revenue and cost of goods sold:

| Date | Account Title and Explanation |

Debit ($) |

Credit ($) |

| Cash | 51,200 | ||

| Sales Revenue | 51,200 | ||

| (To record the sales revenue received in cash ) |

Table (2)

- Cash is an asset and it increases the value of assets. Therefore, debit cash by $51,200.

- Sales revenue is component of stockholders’ equity and it increases the value of stockholder’s equity. Therefore, credit sales revenue by $51,200.

| Date | Account Title and Explanation |

Debit ($) |

Credit ($) |

| Cost of goods sold | 28,797 | ||

| Inventory | 28,797 | ||

| (To record the cost of goods sold incurred during the year) |

Table (3)

- Cost of goods sold is a component of stockholders’ equity and it decreases the value of stockholder’s equity. Therefore, debit cost of goods sold by $28,797.

- Inventory is an asset and it decreases the value of asset. Therefore, credit inventory by $28,797.

b. Record the sales return and the cost of inventory used for production.

| Date | Account Title and Explanation |

Debit ($) |

Credit ($) |

| Sales revenue | 600 | ||

| Cash | 600 | ||

| (To record the sales returns from customer) |

Table (4)

- Sales revenue is a component of stockholders’ equity and it increases the value of stockholder’s equity. Therefore, debit sales revenue by $600.

- Cash is an asset and it decreases the value of assets. Therefore, credit cash by $600

| .Date | Account Title and Explanation |

Debit ($) |

Credit ($) |

| Inventory | 360 | ||

| Cost of goods sold | 360 | ||

| (To record the cost of inventory return) |

Table (5)

- Inventory is an asset and it increases the value of assets. Therefore, debit inventory by $360.

- Cost of goods sold is a component of stockholders’ equity and it decreases the value of stockholder’s equity. Therefore, credit cost of goods sold by $360.

c. Record the sale of merchandise on account:

| Date | Account Title and Explanation |

Debit ($) |

Credit ($) |

| Accounts Receivable | 10,000 | ||

| Sales Revenue | 10,000 | ||

| (To record the sales revenue received on account) |

Table (6)

- Accounts receivable is an asset and it increases the value of assets. Therefore, debit accounts receivable by $10,000.

- Sales revenue is component of stockholders’ equity and it increases the value of stockholder’s equity. Therefore, credit sales revenue by $10,000.

| Date | Account Title and Explanation |

Debit ($) |

Credit ($) |

| Cost of goods sold | 4,750 | ||

| Inventory | 4,750 | ||

| (To record the cost of inventory return) |

Table (7)

- Cost of goods sold is a component of stockholders’ equity and it decreases the value of stockholder’s equity. Therefore, debit cost of goods sold by $4,750.

- Inventory is an asset and it decreases the value of asset. Therefore, credit inventory by $4,750.

d. Record the cash receipt from customer.

| Date | Account Title and Explanation |

Debit ($) |

Credit ($) |

| Cash | 5,000 | ||

| Accounts Receivable | 5,000 | ||

| (To record the cash received from customers) |

Table (8)

- Cash is an asset and it increases the value of assets. Therefore, debit cash by $5,000.

- Accounts receivable is an asset and it decreases the value of assets. Therefore, credit accounts receivable by $5,000.

e. Record the sales return and allowances:

| Date | Account Title and Explanation |

Debit ($) |

Credit ($) |

| Sales revenue | 160 | ||

| Accounts receivable | 160 | ||

| (To record the sales returns from customer and allowances ) |

Table (9)

- Sales revenue is a component of stockholders’ equity and it decreases the value of stockholder’s equity. Therefore, debit sales returns and allowances by $160.

- Accounts receivable is an asset and it decreases the value of assets. Therefore, credit accounts receivable by $160.

4.

Describe whether the sale of given contract would increase (or decrease) the gross profit and gross profit percentage of Incorporation H.

Explanation of Solution

Describe whether the sales of given contract would increase (or decrease) the gross profit and gross profit percentage of Incorporation H as follows:

In this case, the gross profit percentage is decreased from 45.1% to 42.8% (5), because of the sale of contract.

Working note 4:

Calculate the gross profit from the sale of contract.

Working note 5:

Calculate the gross profit percentage of Company after the sale of contract.

Want to see more full solutions like this?

Chapter 6 Solutions

Fundamentals Of Financial Accounting

- Use the first-in, first-out (FIFO) cost allocation method, with perpetual inventory updating, to calculate (a) sales revenue, (b) cost of goods sold, and c) gross margin for A75 Company, considering the following transactions.arrow_forwardBeginning inventory, purchases, and sales data for portable game players are as follows: The business maintains a perpetual inventory system, costing by the first-in, first-out method. a. Determine the cost of the merchandise sold for each sale and the inventory balance after each sale, presenting the data in the form illustrated in Exhibit 3. b. Based upon the preceding data, would you expect the inventory to be higher or lower using the last-in, first-out method?arrow_forwardUse the last-in, first-out (LIFO) cost allocation method, with perpetual inventory updating, to calculate (a) sales revenue, (b) cost of goods sold, and c) gross margin for A75 Company, considering the following transactions.arrow_forward

- Use the first-in, first-out method (FIFO) cost allocation method, with perpetual inventory updating, to calculate (a) sales revenue, (b) cost of goods sold, and c) gross margin for B75 Company, considering the following transactions.arrow_forwardWhich of the following accounts would be included in the chart of accounts of a merchandising company using the (a) periodic inventory system, (b) perpetual inventory system, or (c) both systems? 1. Purchases 2. Inventory Periodic Inventory System 3. Sales Perpetual Inventory System 4. Purchases Discounts Both Systems 5. Cost of Goods Sold 6. Freight In 7. Delivery Expense Previous Nextarrow_forwardUsing the accounts listed below, review the following transactions for April Anglers and record any required journal entries. April Anglers uses the periodic inventory system: Accounts Payable| Merchandise Inventory Sales Accounts Purchases Sales Discounts Receivable Sales Returns and Cash Purchase Discounts Allowances Cost of Goods Purchase Returns and Sales Tax Payable Sold Allowances PLEASE NOTE: You must enter the account names exactly as written above and all dollar amounts will be with "$" and commas as needed (i.e. $12,345). Oct. 4: April Anglers purchases 80 fishing poles at $40 each with cash. DR CR Oct. 5: April Anglers purchases 120 fishing poles at $30 each on credit. Terms of the purchase are 3/15, n/30, invoice date October 5. DR CR Oct. 12: April Anglers discovers 15 of the fishing poles are damaged from the October 4 purchase and returns them to the supplier for a full refund. DR CR Oct. 13: April Anglers also discovers that 35 of the fishing poles from the October 5…arrow_forward

- Prepare journal entries to record the following merchandising transactions of Chang Company, which applies the perpetual inventory system. (Use a separate account for each receivable and payable; for example, record the purchase on May 2 in Accounts Payable Smith Company ).arrow_forwardAssume that Whitewall Tire Store completed the following perpetual inventory transactions for a line of tires: i (Click the icon to view the transactions.) Read the requirements. Requirement 1. Compute cost of goods sold and gross profit using the FIFO inventory costing method. Begin by computing the cost of goods sold and cost of ending merchandise inventory using the FIFO inventory costing method. Enter the transactions in chronological order, calculating new inventory on hand balances after each transaction. Once all of the transactions have been entered into the perpetual record, calculate the quantity and total cost of merchandise inventory purchased, sold, and on hand at the end of the period. (Enter the oldest inventory layers first.) Date Quantity Dec. 1 11 23 261 29 Totals Purchases Unit Cost Cost of Goods Sold Total Unit Cost Quantity Cost Total Cost Inventory on Hand Unit Quantity Cost C Total Cost More info Dec. 1 Beginning merchandise inventory Dec. 11 Purchase Dec. 23…arrow_forwardMarin, Inc. values its inventory at the lower-of-LIFO-cost-or-market. The following information is available from the company's inventory records as of December 31, 2020. Unit Replacement Estimated Selling Completion & Disposal Normal Profit Item Quantity Cost Cost/Unit Price/Unit Cost/Unit Margin/Unit X490 10,404 $ 12.75 $ 12.19 $ 14.28 $ 3.06 $ 3.47 X512 5,049 7.14 7.65 9.08 0.26 1.84 X682 18,360 19.38 18.97 32.18 3.32 9.18 Z195 12,750 14.54 14.28 20.20 1.43 5.87 Z846 8,772 12.24 13.01 14.23 2.14 1.12arrow_forward

- Assume the perpetual inventory system is used unless stated otherwise. Round all numbers to the nearest whole dollar unless stated otherwise. Journalizing sales transactions—periodic inventory system Journalize the following sales transactions for Sanborn Camera Store using the periodic inventory system. Explanations are not required.arrow_forwardJournalize the sales transactions for Fast Computers assuming the company uses the perpetual inventory system. (Record debits first, then credits. Select the explanation on the last line of the journal entry table.) Apr. 12: Sold computers on account for $8,500 to a customer, terms 1/15, n/60. The cost of the computers is $5,100. Begin by preparing the entry to journalize the sale portion of the transaction. Do not record the expense related to the sale. We will do that in the following step. Date More Info - X Apr, 12 April 12 Sold computers on account for $8,500 to a customer, terms 1/15, n/60. The cost of the computers is $5,100. 21 Accepted a $3,500 return from a customer from April 12. The computer returned had a cost of $2,100. 26 Received payment from the customer on balance due. Choose from any list or ent 4 parts remaining Print Done Check Answerarrow_forwardPrepare journal entries to record the following merchandising transactions of Lowe's, which uses the perpetual inventory system and the gross method. Hint: It will help to identify each receivable and payable; for example, record the purchase on August 1 in Accounts Payable-Aron. August 1 Purchased merchandise from Aron Company for $8,000 under credit terms of 1/10, n/30, FOB destination, invoice dated August 1. August 5 Sold merchandise to Baird Corporation for $5,600 under credit terms of 2/10, n/60, FOB destination, invoice dated August 5. The merchandise had cost $4,000. August 8 Purchased merchandise from Waters Corporation for $7,000 under credit terms of 1/10, n/45, FOB shipping point, invoice dated August 8. August 9 Paid $220 cash for shipping charges related to the August 5 sale to Baird Corporation. August 10 Baird returned merchandise from the August 5 sale that had cost Lowe's $500 and was sold for $1,000. The merchandise was restored to inventory. August 12 After…arrow_forward

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College