Videos

Suppose that each firm in a competitive industry has the following costs:

Total cost: TC = 50 + ½ q2

Marginal cost: MC = q

where q is an individual firm’s quantity produced.

The market

Demand: QD = 120 − P

where P is the

a. What is each firm’s fixed cost? What is its variable cost? Give the equation for

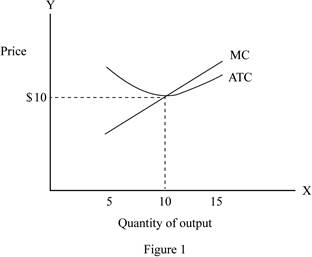

b. Graph average-total-cost curve and the marginal-cost curve for q from 5 to 15. At what quantity is average-total-cost curve at its minimum? What is marginal cost and average total cost at that quantity?

c Give the equation for each firm’s supply curve.

d. Give the equation for the market supply curve for the short run in which the number of firms is fixed.

e. What is the

f. In this equilibrium, how much does each firm produce? Calculate each firm’s profit or loss. Is there incentive for firms to enter or exit?

g. In the long run with free entry and exit, what is the equilibrium price and quantity in this market?

h. In this long-run equilibrium, how much does each firm produce? How many firms are in the market?

Subpart (a):

Calculate average total cost.

Explanation of Solution

The total cost equation, marginal cost equation and demand equation are given below:

The fixed cost and variable cost of each firm are determined from Equation (1). Here, the fixed cost is a part of the total cost and will not change in response to a change in quantity. The variable cost is a part of the total cost and it changes in response to a change in quantity. So, the fixed cost is $50 and the variable cost is

Average total cost equation is represented below:

Or

Concept introduction:

Average total cost: The average total cost is the total cost per unit of the output produced by a firm.

Subpart (b):

Draw average total cost curve.

Explanation of Solution

Figure 1 represents the average total cost curve and marginal cost curve.

From the above figure, the x-axis shows the quantity of the output and the y-axis shows the price level.

From the graph, the average total cost is at its minimum, when they produce 10 units of output. The average total cost and marginal cost are at the quantity of 10 units of output.

Concept introduction:

Average total cost: The average total cost is the total cost per unit of the output produced by a firm.

Subpart (c):

Supply curve.

Explanation of Solution

In the perfect competition, the supply curve is even, as the marginal cost curve is beyond the intersecting point of the average total cost curve.

Supply curve for each firm is shown below:

Concept introduction:

Marginal cost curve: The marginal cost is the additional cost incurred on the additional production and its curve is U-shaped, which represents the combination of price level and quantity of output.

Subpart (d):

Quantity supply.

Explanation of Solution

In the short-run, there are currently 9 firms. So, the market supply curve is determined by using the following formula:

Hence, the short-run market supply curve is shown below:

Concept introduction:

Supply: Supply refers to the total value of the goods and services that are available for the purchase at a particular price in a given period of time.

Subpart (e):

Equilibrium price and quantity.

Explanation of Solution

The equilibrium quantity and price are determined by using the following formula:

Substitute the respective values in Equation (8) to calculate the equilibrium quantity and price.

Thus, the equilibrium price is $12.

Substitute the price of $12 in Equation (3) to calculate the equilibrium quantity.

Thus, the equilibrium quantity is 108 units.

Concept introduction:

Equilibrium price: It is the price at which the quantity demanded of a good or service is equal to the quantity supplied.

Equilibrium: It is the market price and quantity determined by equating the supply to the demand. At this equilibrium point, the supply will be equal to the demand and there will be no excess demand or supply in the economy. Thus, the economy will be at equilibrium.

Subpart (f):

Calculate profit.

Explanation of Solution

In the short-run equilibrium, each firm produces 12 units

Profit can be calculated by using the following formula:

Substitute the respective values in Equation (9) to calculate the profit.

Thus, the profit is $22.

Since the firms have positive value in making profit, there will be a benefit for the firm entering the market.

Concept introduction:

Profit: Profit refers to the excess revenue after subtracting the total cost from the total revenue.

Subpart (g):

Equilibrium quantity.

Explanation of Solution

In the long-run, the firm earns zero economic profit, so the price is equal to the minimum average total cost. Since the average total cost is $10, the equilibrium price is also be $10.

Equilibrium quantity can be determined by using Equation (3), when the equilibrium price is $10.

Thus, the long-run equilibrium quantity is 110.

Concept introduction:

Equilibrium: It is the market price and quantity determined by equating the supply to the demand. At this equilibrium point, the supply will be equal to the demand and there will be no excess demand or supply in the economy. Thus, the economy will be at equilibrium.

Subpart (h):

Number of firms in the long run.

Explanation of Solution

In the long-run, the firm produces 10 units of output. This is because in the long-run, the production price of the firm is equal to the minimum average total cost. The average total cost is 10 units. Also, there are 11 firms

Long run: Thelong run refers to the time, which changes the production variable to adjust to the market situation.

Want to see more full solutions like this?

Chapter 13 Solutions

Essentials of Economics (MindTap Course List)

- Assume that a firm in a competitive market faces the following cost information. If the market price for this firm's product is $40, calculate the profit maximizing level of output for this firm using marginal analysis. It may help to create your own cost table and fill in columns for Marginal Cost and Average Total Cost based on the Total Cost information below. a.What is the level of profit for this firm at the profit maximizing output? b.To convince yourself that the quantity you found is indeed the profit maximizing quantity, try calculating what the profit would be at the next higher level of output. What did you find? c. What do you predict will happen in this market over the long run?arrow_forwardSuppose the market for peaches is perfectly competitive. The short-run average total cost and marginal cost of growing peaches for an individual grower are illustrated in the figure to the right. Assume that the market price for peaches is $28.00 per box. What is the profit-maximizing quantity for peach growers to produce? boxes. (Enter your response as an integer.) Price (dollars per box) 40- 36- 32- 28- 24- 20- 16- 12- 8- 4- 0 10 20 30 40 50 60 70 80 Output (boxes of peaches per day) MC ATC 90 100 oo Qarrow_forwardSuppose that each firm in a competitive industry has the following costs: where q is an individual firm’s quantity produced. The market demand curve for this product is where P is the price and Q is the total quantity of the good. Currently, there are 9 firms in the market. What is each firm’s fixed cost? What is its variable cost? Give the equation for average total cost. Graph average-total-cost curve and the marginal-cost curve for q from 5 to 15. At what quantity is average-total-cost curve at its minimum? What is marginal cost and average total cost at that quantity? Give the equation for each firm’s supply curve. Give the equation for the market supply curve for the short run in which the number of firms is fixed. What is the equilibrium price and quantity for this market in the short run? In this equilibrium, how much does each firm produce? Calculate each firm’s profit or loss. Is there incentive for firms to enter or exit? In the long run with…arrow_forward

- Suppose that each firm in a competitive industry has the following costs: Total cost: TC = 50 + 0.5Q^2The market demand curve for this product is: Qd= 120 −PThere are 9 firms in the market.a) What are each firm’s: fixed cost, variable cost, marginal cost, and average total cost? Graph the average-total-cost curve and the marginal-cost curve.b) Give the equation for each firm’s supply curve.the average-total-cost curve at its minimum? What is marginal cost and average totalc) Give the equation for the market supply curve for the short run in which the numbercost at that quantity?arrow_forwardSuppose the market for peaches is perfectly competitive. The short-run average total cost and marginal cost of growing peaches for an individual grower are illustrated in the figure to the right. Assume that the market price for peaches is $30.00 per box. What is the profit-maximizing quantity for peach growers to produce? boxes. (Enter your response as an integer.) At this level of output, profit will be $. (Enter your response rounded to the nearest dollar.) Peach growers will earn positive economic profit in the short run at any market price above $ per box. (Enter your response rounded to one decimal place.) Price (dollars per box) 40- 36- 32- 28- 24 20 16- 12- 8 4- 10 MC 20 30 40 50 60 70 80 Output (boxes of peaches per day) ▬▬ ATC 90 100 Qarrow_forwardSuppose that each firm in a competitive industry has the following costs: Total cost: TC = 50 + 1/2q2 Marginal cost: MC = q where q is an individual firm's quantity produced. The market demand curve for this product is Demand: QD where P is the price and Q is the total quantity of the good. Currently, there are 9 firms in the market. = 120 – P а. What is each firm’s fixed cost? What is its variable cost? Give the equation for average total cost. b. Graph average-total-cost curve and the marginal-cost curve for q from 5 to 15. At what quantity is average-total-cost curve at its minimum? What is marginal cost and average total cost at that quantity? с. Give the equation for each firm's supply curve. d. Give the equation for the market supply curve for the short run in which the number of firms is fixed. е. What is the equilibrium price and quantity for this market in the short run? In this equilibrium, how much does each firm produce? Calculate each firm's profit or ^ loss. Is there…arrow_forward

- In a perfectly competitive market demand function of a good is Q" = -30P+ 2250 and supply function is Q° = 20P. Firms that are active in this market have an identical cost function of 0* – 6Q² + 30Q Calculate the short run market price and short run profit of each firms. b. How many firms are active in market in short run? c. What will be the long run price in market? d. How many firms are active in market in long run? a.arrow_forwardWill a profit-maximizing firm in a competitive market ever produce a positive level of output in the range where the marginal cost is falling? Give an explanation.arrow_forwardAssume that a firm in a competitive market faces the following cost information. If the market price for this firm's product is $40, calculate the profit maximizing level of output for this firm using marginal analysis. a.Approximately where do you think the price will end up in this market over the long run? b.Last, instead of assuming a given price, how would you go about finding the equilibrium price if you were given information on market demand?arrow_forward

- Consider the market for tilapia. Ripple Rock Fish Farms, a small family fishery in Ohio, and The Fishin’ Company, a large corporate supplier, are both producers of tilapia. The marginal cost curves for both firms are shown in the accompanying graph. a. Suppose the market price of tilapia is $2.50 per pound. Move point A to Ripple Rock’s quantity sold. Move point B to The Fishin’ Company’s quantity sold. b. How many pounds of tilapia do they collectively supply?________thousand pounds c. To achieve efficient production, The Fishin’ Company should supply _____ ("more", or "less", or "the same") it is currently producing, and Ripple Rock should supply __________ ("more", or "less", or "the same") it is currently producing.arrow_forwardConsider a competitive industry with a large number of firms, all of which have identical cost functions c(y) = y2 + 1 if y > 0 and c(y) = 0 ify = 0. The demand curve for this industry is D(p)= 52-p.1. Find marginal cost and average cost functions.2. What is the competitive price in this market?3. What will be the number of firms in the industry?arrow_forwardA perfectly competitive industry is in long-run equilibrium. Each of the identical firms has a long- run cost function C = 100 + q². As a result, a firm's marginal cost function is MC = 2q. In the long-run competitive equilibrium, (a) How much does the firm produce? (b) What is the equilibrium price? (c) If the market quantity demanded at the equilibrium price is Q = 2500, how many firms are in the market?arrow_forward

Economics (MindTap Course List)EconomicsISBN:9781337617383Author:Roger A. ArnoldPublisher:Cengage Learning

Economics (MindTap Course List)EconomicsISBN:9781337617383Author:Roger A. ArnoldPublisher:Cengage Learning