Concept explainers

Videos

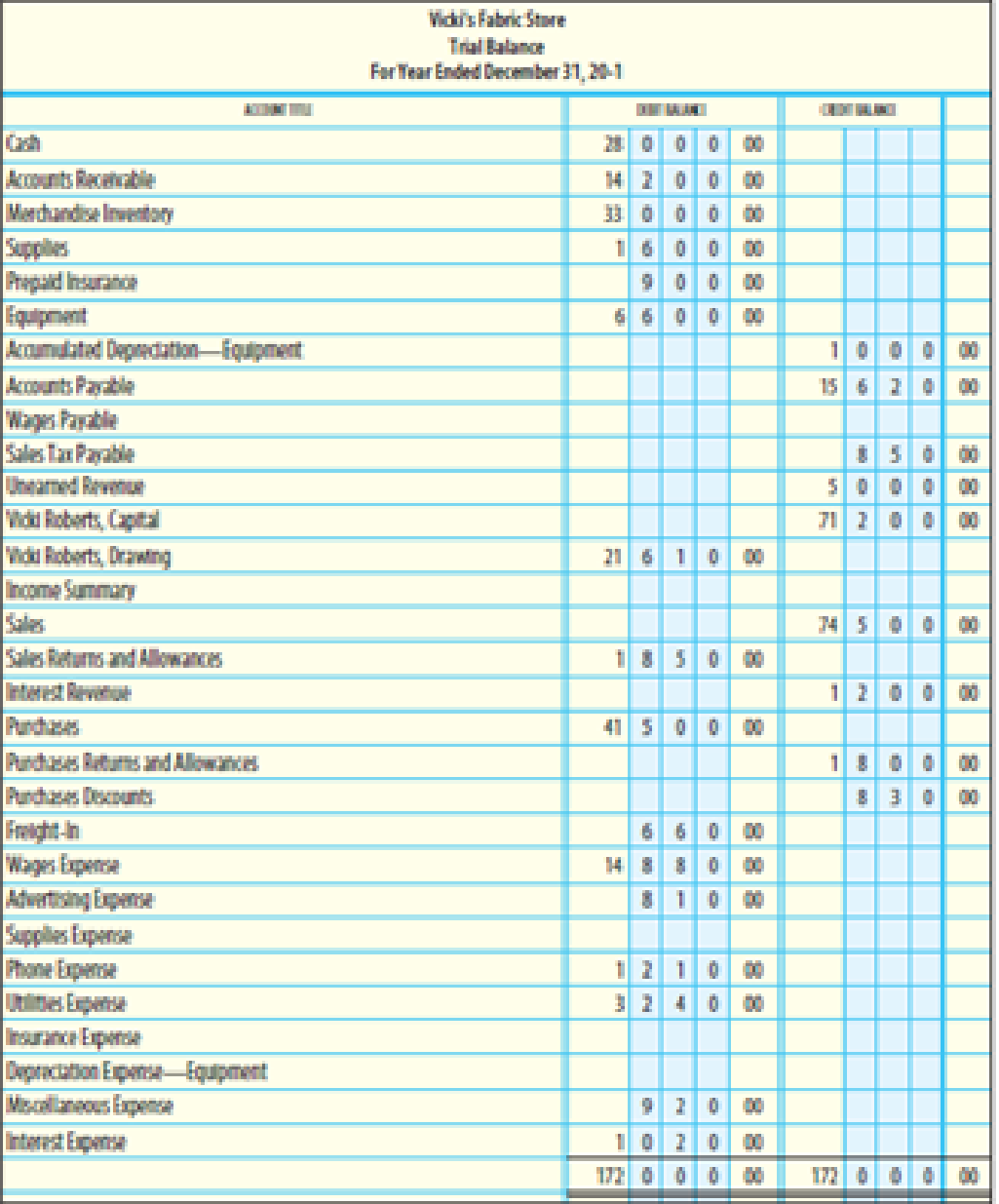

WORK SHEET, ADJUSTING, CLOSING, AND REVERSING ENTRIES Vicki’s Fabric Store shows the

At the end of the year, the following adjustments need to be made:

(a and b) Merchandise inventory as of December 31, $31,600.

(c) Unused supplies on hand, $1,150.

(d) Insurance expired, $350.

(e)

(f) Wages earned but not paid (Wages Payable), $520.

(g) Unearned revenue on December 31, 20-1, $1,200.

REQUIRED

- 1. Prepare a work sheet.

- 2. Prepare

adjusting entries . - 3. Prepare closing entries.

- 4. Prepare a post-closing trial balance.

- 5. Prepare reversing entry(ies).

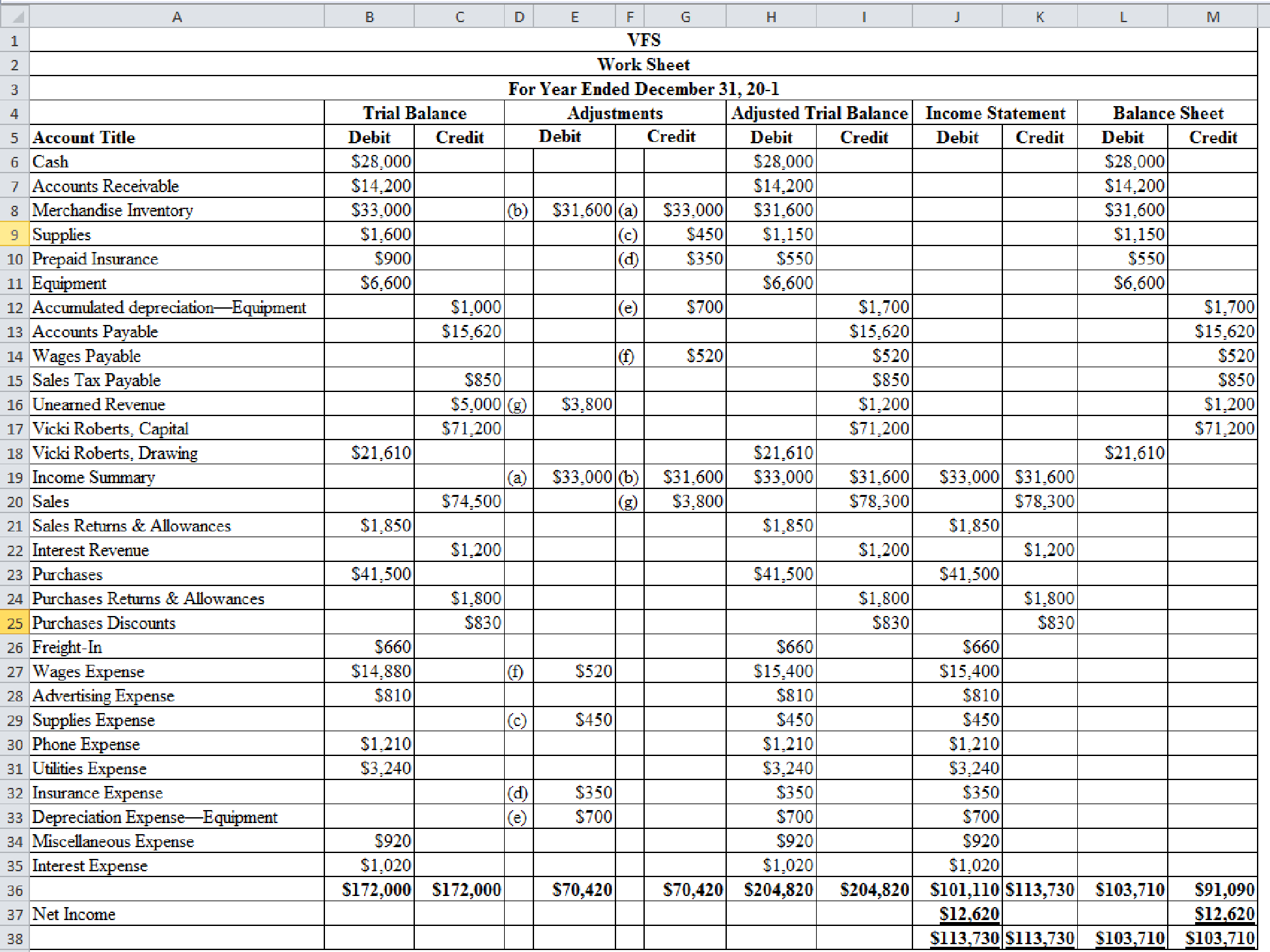

1.

Prepare a worksheet of VFS.

Explanation of Solution

Prepare a worksheet of VFC.

Figure (1)

2.

Prepare adjusting entries.

Explanation of Solution

Adjustment entries:

Adjusting entries are those entries which are made at the end of the year to update all the balances in the financial statements to show the true financial information and to maintain the records according to accrual basis principle.

Prepare adjusting entries of VFS.

| Date | Account titles and Explanation | Debit | Credit | |

| 20-1 | ||||

| December 31 | (a) | Income Summary | $33,000 | |

| Merchandise Inventory | $33,000 | |||

| December 31 | (b) | Merchandise Inventory | $31,600 | |

| Income Summary | $31,600 | |||

| December 31 | (c) | Supplies Expense | $450 | |

| Supplies | $450 | |||

| December 31 | (d) | Insurance Expense | $350 | |

| Prepaid Insurance | $350 | |||

| December 31 | (e) | Depreciation expense - Equipment | $700 | |

| Accumulated depreciation - Equipment | $700 | |||

| December 31 | (f) | Wages Expense | $520 | |

| Wages Payable | $520 | |||

| December 31 | (g) | Unearned Revenue | $3,800 | |

| Sales | $3,800 |

Table (1)

3.

Prepare closing entries.

Explanation of Solution

Closing entries: The journal entries prepared to close the temporary accounts to Retained Earnings account are referred to as closing entries. The revenue, expense, and dividends accounts are referred to as temporary accounts because the information and figures in these accounts is held temporarily and consequently transferred to permanent account at the end of accounting year.

Prepare closing entries of VFS.

| Date | Account titles and Explanation | Debit | Credit |

| 20-1 | Closing Entries | ||

| December 31 | Sales | $78,300 | |

| Interest Revenue | $1,200 | ||

| Purchases Returns & Allowances | $1,800 | ||

| Purchases Discounts | $830 | ||

| Income Summary | $82,130 | ||

| December 31 | Income Summary | $68,110 | |

| Sales Returns & Allowances | $1,850 | ||

| Purchases | $41,500 | ||

| Freight-In | $660 | ||

| Wages Expense | $15,400 | ||

| Advertising Expense | $810 | ||

| Supplies Expense | $450 | ||

| Phone Expense | $1,210 | ||

| Utilities Expense | $3,240 | ||

| Insurance Expense | $350 | ||

| Depreciation Exp. - Equipment | $700 | ||

| Miscellaneous Expense | $920 | ||

| Interest Expense | $1,020 | ||

| December 31 | Income Summary | $12,620 | |

| VRS's Capital | $12,620 | ||

| December 31 | VRS's Capital | $21,610 | |

| VRS's Drawing | $21,610 |

Table (2)

4.

Prepare post-closing trail balance.

Explanation of Solution

Post-closing trial balance:

The post-closing trial balance is a summary of all ledger accounts, and it shows the debit and the credit balances after the closing entries are journalized and posted. The post-closing trial balance contains only permanent (balance sheet) accounts, and the debit and the credit balances of permanent accounts should agree.

Prepare a post-closing trail balance of VFS.

| VFS | ||

| Post-Closing Trial Balance | ||

| December 31, 20-1 | ||

| Account Title | Debit | Credit |

| Cash | $28,000 | |

| Accounts Receivable | $14,200 | |

| Merchandise Inventory | $31,600 | |

| Supplies | $1,150 | |

| Prepaid Insurance | $550 | |

| Equipment | $6,600 | |

| Accumulated Depreciation—Equipment | $1,700 | |

| Accounts Payable | $15,620 | |

| Wages Payable | $520 | |

| Sales Tax Payable | $850 | |

| Unearned Revenue | $1,200 | |

| Vicki Roberts, Capital | $62,210 | |

| Total | $82,100 | $82,100 |

Table (3)

5.

Prepare reversing entry.

Explanation of Solution

Reversing entries:

Several Adjusting entries are needed to update all the balances in the financial statements in order to project true financial information and to maintain the records according to accrual basis principle. Some of these adjusting entries must be reversed at the beginning of a next accounting period to simplify the recording of transactions. Reversing entry is the opposite of adjusting entry.

Prepare reversing entry of VFS.

| Date | Account titles and Explanation | Debit | Credit |

| 20-2 | Reversing Entry | ||

| January 1 | Wages Payable | $520 | |

| Wages Expense | $520 |

Table (4)

Want to see more full solutions like this?

Chapter 15 Solutions

College Accounting, Chapters 1-9 (New in Accounting from Heintz and Parry)

- John Neff owns and operates Waikiki Surf Shop. A year-end trial balance is provided on page 561. Year-end adjustment data for the Waikiki Surf Shop are shown below. Neff uses the periodic inventory system. Year-end adjustment data are as follows: (a, b)A physical count shows that merchandise inventory costing 51,800 is on hand as of December 31, 20--. (c, d, e)Neff estimates that customers will be granted 2,000 in refunds of this years sales next year and the merchandise expected to be returned will have a cost of 1,200. (f)Supplies remaining at the end of the year, 600. (g)Unexpired insurance on December 31, 2,600. (h)Depreciation expense on the building for 20--, 5,000. (i)Depreciation expense on the store equipment for 20--, 3,000. (j)Wages earned but not paid as of December 31, 1,800. (k)Neff also offers boat rentals which clients pay for in advance. Unearned boat rental revenue as of December 31 is 3,000. Required 1. Prepare a year-end spreadsheet. 2. Journalize the adjusting entries. 3. Compute cost of goods sold using the spreadsheet prepared for part (1).arrow_forwardThe trial balance of Jillson Company as of December 31, the end of its current fiscal year, is as follows: Here are the data for the adjustments. ab. Merchandise Inventory at December 31, 54,845.00. c. Store supplies inventory (on hand), 488.50. d. Insurance expired, 680. e. Salaries accrued, 692. f. Depreciation of store equipment, 3,760. Required Complete the work sheet after entering the account names and balances onto the work sheet.arrow_forwardThe following accounts appear in the ledger of Celso and Company as of June 30, the end of this fiscal year. The data needed for the adjustments on June 30 are as follows: ab.Merchandise inventory, June 30, 54,600. c.Insurance expired for the year, 475. d.Depreciation for the year, 4,380. e.Accrued wages on June 30, 1,492. f.Supplies on hand at the end of the year, 100. Required 1. Prepare a work sheet for the fiscal year ended June 30. Ignore this step if using CLGL. 2. Prepare an income statement. 3. Prepare a statement of owners equity. No additional investments were made during the year. 4. Prepare a balance sheet. 5. Journalize the adjusting entries. 6. Journalize the closing entries. 7. Journalize the reversing entry as of July 1, for the wages that were accrued in the June adjusting entry. Check Figure Net income, 14,066arrow_forward

- A partial work sheet for The Fan Shop is presented here. The merchandise inventory at the beginning of the year was 52,300. P. G. Ochoa, the owner, withdrew 30,500 during the year. Required 1. Prepare an income statement. 2. Journalize the closing entries. Check Figure Cost of Goods Sold, 206,120arrow_forwardA partial work sheet for McKnight Music Store is presented here. The merchandise inventory at the beginning of the fiscal period was 48,473. W. J. McKnight, the owner, withdrew 40,000 during the year. Required 1. Prepare an income statement. 2. Journalize the closing entries. Check Figure Cost of Goods Sold, 192,521arrow_forwardBay Book and Software has two sales departments: Book and Software. After recording and posting all adjustments, including the adjustments for merchandise inventory, the accountant prepared the adjusted trial balance (shown on the next page) at the end of the fiscal year. Merchandise inventories at the beginning of the year were as follows: Book Department, 53,410; Software Department, 23,839. The bases (and sources of figures) for apportioning expenses to the two departments are as follows (rounded to the nearest dollar): Sales Salary Expense (payroll register): Book Department, 45,559; Software Department, 35,629 Advertising Expense (newspaper column inches): Book Department, 550 inches; Software Department, 450 inches Depreciation Expense, Store Equipment (property and equipment ledger): Book Department, 7,851; Software Department, 2,682 Store Supplies Expense (requisitions): Book Department, 205; Software Department, 199 Miscellaneous Selling Expense (volume of gross sales): Book Department, 240; Software Department, 110 Rent Expense and Utilities Expense (floor space): Book Department, 9,000 square feet; Software Department, 7,000 square feet Bad Debts Expense (volume of gross sales): Book Department, 1,029; Software Department, 441 Miscellaneous General Expense (volume of gross sales): Book Department, 364; Software Department, 156 Required Prepare an income statement by department to show income from operations, as well as a nondepartmentalized income statement (using the Total columns) to show net income for the entire company.arrow_forward

- SALES RETURNS AND ALLOWANCES ADJUSTMENT At the end of year 1, MCs estimates that 2,400 of the current years sales will be returned in year 2. Prepare the adjusting entry at the end of year 1 to record the estimated sales returns and allowances and customer refunds payable for this 2,400. Use accounts as illustrated in the chapter.arrow_forwardAdjusting Entries: Prepare the correct adjusting entries using the following information.1) The warehouse employees counted the ending inventory on hand at December 31, 2003. Their ending inventory balance is $40,000. (Remember we are using the periodic inventory method.)2) The supplies department counted the supplies on hand. The balance of supplies at December 31 is $600. 3) The note payable is due in 5 years and was initiated on April 1, 2003. The note payable requires annual interest payments of 10% payable on March 31 of each year. (Note: I used 275 days out of 365 to prorate the interest expense on the note payable)4) The company has estimated that bad debt expense is equal to one half of a percent (.005) of net sales (sales less sales discounts and returns) .5) December salaries and wages will be paid on January 5, 2004. December salaries and wages are $5,000. 6) Two of the fixed assets have not been completely depreciated. These two items are a…arrow_forwardBrian Burns uses perpetual inventory system and LIFO All credit sales discounts are recorded using the net method – customers receive a 3 percent discount if they pay within 30 days. Purchase discounts are recorded using the net method All depreciation is straight line. Additional Information for Journal Entries Brian Burns records accruals for utilities expense as an adjusting journal entry at the end of each year. They pay utilities once a year on January 31st for the prior year. NOTE: There is no payment for utilities on January 31st of 2022 because January 1 of 2022 is the first day of operations. January 1 Sold 10,000 shares of common stock for $95 per share. Borrowed $2,000,000 at 8 percent with interest payable semi-annually (on July 1 and January 1). Purchased 1,000 units of inventory at $150 a piece on credit from Biggie Smalls Inc. Terms are 2/10; n/60 Paid $480,000 for 2 years of rent in advance…arrow_forward

- Brian Burns uses perpetual inventory system and LIFO All credit sales discounts are recorded using the net method – customers receive a 3 percent discount if they pay within 30 days. Purchase discounts are recorded using the net method All depreciation is straight line. Additional Information for Journal Entries Brian Burns records accruals for utilities expense as an adjusting journal entry at the end of each year. They pay utilities once a year on January 31st for the prior year. NOTE: There is no payment for utilities on January 31st of 2022 because January 1 of 2022 is the first day of operations. How would you put these dollar amounts on the statement of cash flows for the year ended on December 31, 2022 below: January 1 Sold 10,000 shares of common stock for $95 per share. Borrowed $2,000,000 at 8 percent with interest payable semi-annually (on July 1 and January 1). Purchased 1,000 units of inventory at…arrow_forwardBrian Burns uses perpetual inventory system and LIFO All credit sales discounts are recorded using the net method – customers receive a 3 percent discount if they pay within 30 days. Purchase discounts are recorded using the net method All depreciation is straight line. Additional Information for Journal Entries Brian Burns records accruals for utilities expense as an adjusting journal entry at the end of each year. They pay utilities once a year on January 31st for the prior year. NOTE: There is no payment for utilities on January 31st of 2022 because January 1 of 2022 is the first day of operations. January 1 Sold 10,000 shares of common stock for $95 per share. Borrowed $2,000,000 at 8 percent with interest payable semi-annually (on July 1 and January 1). Purchased 1,000 units of inventory at $150 a piece on credit from Biggie Smalls Inc. Terms are 2/10; n/60 Paid $480,000 for 2 years of rent in advance…arrow_forwardBrian Burns uses perpetual inventory system and LIFO All credit sales discounts are recorded using the net method – customers receive a 3 percent discount if they pay within 30 days. Purchase discounts are recorded using the net method All depreciation is straight line. Additional Information for Journal Entries Brian Burns records accruals for utilities expense as an adjusting journal entry at the end of each year. They pay utilities once a year on January 31st for the prior year. NOTE: There is no payment for utilities on January 31st of 2022 because January 1 of 2022 is the first day of operations. January 1 Sold 10,000 shares of common stock for $95 per share. Borrowed $2,000,000 at 8 percent with interest payable semi-annually (on July 1 and January 1). Purchased 1,000 units of inventory at $150 a piece on credit from Biggie Smalls Inc. Terms are 2/10; n/60 Paid $480,000 for 2 years of rent in advance…arrow_forward

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage