Concept explainers

Videos

Rolertyme Company manufactures roller skates. With the exception of the rollers, all parts of the skates are produced internally. Neeta Booth, president of Rolertyme, has decided to make the rollers instead of buying them from external suppliers. The company needs 100,000 sets per year (currently it pays $1.90 per set of rollers).

The rollers can be produced using an available area within the plant. However, equipment for production of the rollers would need to be leased ($30,000 per year lease payment). Additionally, it would cost $0.50 per machine hour for power, oil, and other operating expenses. The equipment will provide 60,000 machine hours per year. Direct material costs will average $0.75 per set, and direct labor will average $0.25 per set. Since only one type of roller would be produced, no additional demands would be made on the setup activity. Other overhead activities (besides machining and setups), however, would be affected. The company’s cost management system provides the following information about the current status of the overhead activities that would be affected. (The supply and demand figures do not include the effect of roller production on these activities.) The lumpy quantity indicates how much capacity must be purchased should any expansion of activity supply be needed. The purchase price is the cost of acquiring the capacity represented by the lumpy quantity. This price also represents the cost of current spending on existing activity supply (for each block of activity).

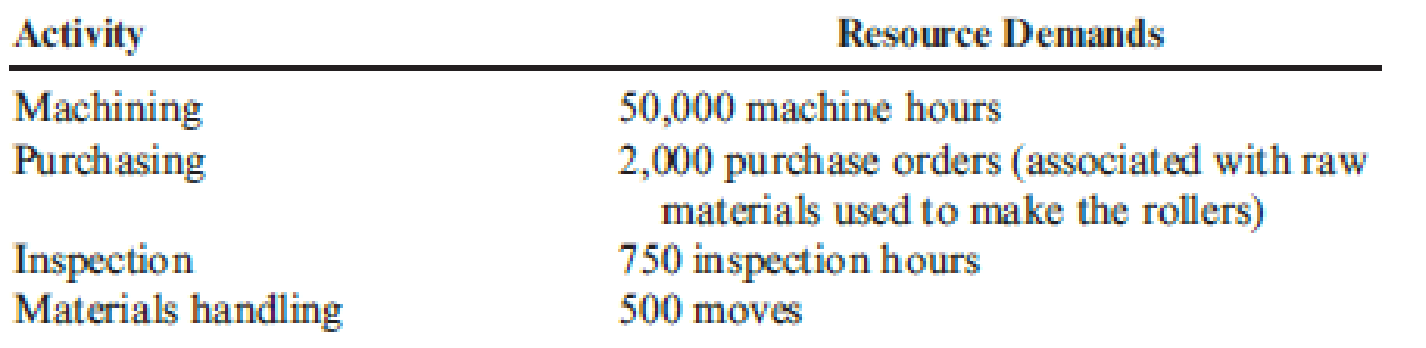

Production of rollers would place the following demands on the overhead activities:

Producing the rollers also means that the purchase of outside rollers will cease. Thus, purchase orders associated with the outside acquisition of rollers will drop by 5,000. Similarly, the moves for the handling of incoming orders will decrease by 200. The company has not inspected the rollers purchased from outside suppliers.

Required:

- 1. Classify all resources associated with the production of rollers as flexible resources and committed resources. Label each committed resource as a short- or long-term commitment. How should we describe the cost behavior of these short- and long-term resource commitments? Explain.

- 2. Calculate the total annual resource spending (for all activities except for setups) that the company will incur after production of the rollers begins. Break this cost into fixed and variable activity costs. In calculating these figures, assume that the company will spend no more than necessary. What is the effect on resource spending caused by production of the rollers?

- 3. Refer to Requirement 2. For each activity, break down the cost of activity supplied into the cost of activity output and the cost of unused activity.

Trending nowThis is a popular solution!

Chapter 3 Solutions

Cornerstones of Cost Management (Cornerstones Series)

- TufStuff, Inc., sells a wide range of drums, bins, boxes, and other containers that are used in the chemical industry. One of the company’s products is a heavy-duty corrosion-resistant metal drum, called the WVD drum, used to store toxic wastes. Production is constrained by the capacity of an automated welding machine that is used to make precision welds. A total of 2,000 hours of welding time is available annually on the machine. Because each drum requires 0.4 hours of welding machine time, annual production is limited to 5,000 drums. At present, the welding machine is used exclusively to make the WVD drums. The accounting department has provided the following financial data concerning the WVD drums: WVD Drums Selling price per drum $ 149.00 Cost per drum: Direct materials (Variable) $52.10 Direct labor (Variable) 3.60 VariableManufacturing overhead…arrow_forwardTufStuff, Incorporated, sells a wide range of drums, bins, boxes, and other containers that are used in the chemical industry. One of the company’s products is a heavy-duty corrosion-resistant metal drum, called the WVD drum, used to store toxic wastes. Production is constrained by the capacity of an automated welding machine that is used to make precision welds. A total of 2,140 hours of welding time is available annually on the machine. Because each drum requires 0.4 hours of welding machine time, annual production is limited to 5,350 drums. At present, the welding machine is used exclusively to make the WVD drums. The accounting department has provided the following financial data concerning the WVD drums: WVD Drums Selling price per drum $ 177.00 Cost per drum: Direct materials $ 52.10 Direct labor ($25 per hour) 5.00 Manufacturing overhead 8.70 Selling and administrative expense 31.20 97.00 Margin per drum $ 80.00 Management believes 6,275…arrow_forwardThe Pittsburgh division of Vermont Machinery, Inc., manufactures drill bits.One of the production processes for a drill bit requires tipping, whereby carbide tips are inserted into the bit to make it stronger and more durable. This tipping process usually requires four or five operators, depending on the weekly workload. The same operators are also assigned to the stamping operation, where the size of the drill bit and the company's logo is imprinted on the bit. Vermont is considering acquiring three automatic tipping machines to replace the manual tipping and stamping operations. If the tipping process is automated, the division's engineers will have to redesign the shapes of the carbide tips to be used in the machine. The new design requires less carbide, resulting in savings on materials. The following financial data have been compiled: Project life: six years. Expected annual savings: reduced labor, $56,000; reduced material, $75,000; other benefits (reduced carpal tunnel syndrome…arrow_forward

- TufStuff, Inc., sells a wide range of drums, bins, boxes, and other containers that are used in the chemical industry. One of the company’s products is a heavy-duty corrosion-resistant metal drum, called the WVD drum, used to store toxic wastes. Production is constrained by the capacity of an automated welding machine that is used to make precision welds. A total of 2,160 hours of welding time is available annually on the machine. Because each drum requires 0.4 hours of welding machine time, annual production is limited to 5,400 drums. At present, the welding machine is used exclusively to make the WVD drums. The accounting department has provided the following financial data concerning the WVD drums: WVD Drums Selling price per drum $ 181.00 Cost per drum: Direct materials $52.10 Direct labor ($26 per hour) 5.20 Manufacturing overhead 9.30 Selling and administrative expense 31.40 98.00 Margin per drum $ 83.00 Management…arrow_forwardUTAH CORP. is a chemical manufacturer that supplies various products to industrial users. The company plans to introduce a new chemical solution called Bysap, for which it needs to develop a standard product cost. The following labor information is available on the production of Bysap. The product, which is bottled in 10-liter containers, is primarily a mixture of Byclyn, Salex, and Protet. The finished product is highly unstable, and one 10-liter batch out of six is rejected at the final inspection. Rejected batches have no commercial value and are thrown out. It takes a worker 35 minutes to process one 10-liter batch of Bysap. Employees work on eight-hour a day, including one hour per day for rest breaks and cleanup. What is the standard labor time to produce one 10-liter batch of Bysap? 2. MAINE INC.’s direct labor costs for the month of May are as follows: Standard direct labor hours allowed 12,500 Actual direct labor…arrow_forwardSensor Systems manufactures an optical switch that it uses in its final product. The switch has the following manufacturing costs per unit: LOADING... (Click the icon to view the costs.) Direct materials $7.00 Direct labor 2.00 Variable overhead 8.00 Fixed overhead 6.50____________________________ Manufacturing product cost $23.50__________________________ _________________________________ LOADING... (Click the icon to view additional information.) Another company has offered to sell Sensor Systems the switch for $19.00 per unit. If Sensor Systems buys the switch from the outside supplier, the idle manufacturing facilities cannot be used for any other purpose, yet none of the fixed costs are avoidable. Prepare an outsourcing analysis to determine whether Sensor Systems should make or buy the switch. (For the Difference column, use a minus sign or parentheses only when the cost of outsourcing…arrow_forward

- QualSupport Corporation manufactures seats for automobiles, vans, trucks, and various recreational vehicles. The company has a number of plants around the world, including the Denver Cover Plant, which makes seat covers. Ted Vosilo is the plant manager of the Denver Cover Plant but also serves as the regional production manager for the company. His budget as the regional manager is charged to the Denver Cover Plant. Vosilo has just heard that QualSupport has received a bid from an outside vendor to supply the equivalent of the entire annual output of the Denver Cover Plant for $35 million. Vosilo was astonished at the low outside bid because the budget for the Denver Cover Plant’s operating costs for the upcoming year was set at $52 million. If this bid is accepted, the Denver Cover Plant will be closed down. The budget for Denver Cover’s operating costs for the coming year is presented below. Denver Cover PlantAnnual Budget for Operating Costs Materials $ 14,000,000…arrow_forwardThe company has an offer from Duvall Valves to produce the part for $2,000 per unit and supply 1,000 valves (the number needed in the coming year). If the company accepts this offer and shuts down production of valves, production workers and supervisors will be reassigned to other areas. The equipment cannot be used elsewhere in the company, and it has no market value. However, the space occupied by the production of the valve can be used by another production group that is currently leasing space for $55,000 per year. What is the incremental savings of buying the valves? (The answer should be stated in a per-unit format and is a positive number)arrow_forwardcompany manufactures desks and computer tables at plants in Texas and Louisiana. At the Texas plant, production costs are $12 for each desk and $20 for each computer table, and the plant can produce at most 120 units per day. At the Louisiana plant, costs are $14 for each desk and $19 per computer table, and the plant can produce at most 150 units per day. The company gets a rush order for 130 desks and 130 computer tables at a time when the Texas plant is further limited by the fact that the number of computer tables it produces must be at least 10 more than the number of desks. How should production be scheduled at each location in order to fill the order at minimum cost? What is the minimum cost?arrow_forward

- ualSupport Corporation manufactures seats for automobiles, vans, trucks, and various recreational vehicles. The company has a number of plants around the world, including the Denver Cover Plant, which makes seat covers. Ted Vosilo is the plant manager of the Denver Cover Plant but also serves as the regional production manager for the company. His budget as the regional manager is charged to the Denver Cover Plant. Vosilo has just heard that QualSupport has received a bid from an outside vendor to supply the equivalent of the entire annual output of the Denver Cover Plant for $20.19 million. Vosilo was astonished at the low outside bid because the budget for the Denver Cover Plant’s operating costs for the upcoming year was set at $23.49 million. If this bid is accepted, the Denver Cover Plant will be closed down. The budget for Denver Cover’s operating costs for the coming year is presented below. Denver Cover Plant Annual Budget for Operating Costs Materials $…arrow_forwardJonfran Company manufactures three different models of paper shredders including the waste container, which serves as the base. While the shredder heads are different for all three models, the waste container is the same. The number of waste containers that Jonfran will need during the following years is estimated as follows: The equipment used to manufacture the waste container must be replaced because it is broken and cannot be repaired. The new equipment would have a purchase price of 945,000 with terms of 2/10, n/30; the companys policy is to take all purchase discounts. The freight on the equipment would be 11,000, and installation costs would total 22,900. The equipment would be purchased in December 20x4 and placed into service on January 1, 20x5. It would have a five-year economic life and would be treated as three-year property under MACRS. This equipment is expected to have a salvage value of 12,000 at the end of its economic life in 20x9. The new equipment would be more efficient than the old equipment, resulting in a 25 percent reduction in both direct materials and variable overhead. The savings in direct materials would result in an additional one-time decrease in working capital requirements of 2,500, resulting from a reduction in direct material inventories. This working capital reduction would be recognized at the time of equipment acquisition. The old equipment is fully depreciated and is not included in the fixed overhead. The old equipment from the plant can be sold for a salvage amount of 1,500. Rather than replace the equipment, one of Jonfrans production managers has suggested that the waste containers be purchased. One supplier has quoted a price of 27 per container. This price is 8 less than Jonfrans current manufacturing cost, which is as follows: Jonfran uses a plantwide fixed overhead rate in its operations. If the waste containers are purchased outside, the salary and benefits of one supervisor, included in fixed overhead at 45,000, would be eliminated. There would be no other changes in the other cash and noncash items included in fixed overhead except depreciation on the new equipment. Jonfran is subject to a 40 percent tax rate. Management assumes that all cash flows occur at the end of the year and uses a 12 percent after-tax discount rate. Required: 1. Prepare a schedule of cash flows for the make alternative. Calculate the NPV of the make alternative. 2. Prepare a schedule of cash flows for the buy alternative. Calculate the NPV of the buy alternative. 3. Which should Jonfran domake or buy the containers? What qualitative factors should be considered? (CMA adapted)arrow_forwardMossfort, Inc., has a division in Canada that makes long-lasting exterior wood stain. Mossfort has another U.S. division, the Retail Division, that operates a chain of home improvement stores. The Retail Division would like to buy the unique, long-lasting wood stain from the Canadian division, since this type of stain is not currently available. The Exterior Stain Division incurs manufacturing costs of 13.45 for one gallon of stain. If the Retail Division purchases the stain from the Canadian division, the shipping costs will be 1.40 per gallon, but sales commissions of 0.75 per gallon will be avoided with an internal transfer. The Retail Division plans to sell the stain for 32.80 per gallon. Normally, the Retail Division earns a gross margin of 35 percent above cost of goods sold. Required: 1. Which Section 482 method should be used to calculate the allowable transfer price? 2. Calculate the appropriate transfer price per gallon. (Round to the nearest cent.)arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning

Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning