Concept explainers

Videos

The general ledger of Zips Storage at January 1, 2018, includes the following account balances:

| Accounts | Debits | Credits |

| Cash | $ 24,600 | |

| Accounts Receivable | 15,400 | |

| Prepaid Insurance | 12,000 | |

| Land | 148,000 | |

| Accounts Payable | $ 6,700 | |

| Deferred Revenue | 5,800 | |

| Common Stock | 143,000 | |

| Retained Earnings | 44,500 | |

| Totals | $200,000 | $200,000 |

The following is a summary of the transactions for the year:

a. January 9 Provide storage services for cash, $134,100, and on account, $52,200.

b. February 12 Collect on accounts receivable, $51,500.

c. April 25 Receive cash in advance from customers, $12,900.

d. May 6 Purchase supplies on account, $9,200.

e. July 15 Pay property taxes, $8,500.

f. September 10 Pay on accounts payable, $11,400.

g. October 31 Pay salaries, $123,600.

h. November 20 Issue shares of common stock in exchange for $27.000 cash.

i. December 30 Pay $2,800 cash dividends to stockholders.

Required:

1. Set up the necessary T-accounts and enter the beginning balances from the

2. Record each of the summary transactions listed above.

3. Post the transactions to the accounts.

4. Prepare an unadjusted trial balance.

5. Record

6. Post adjusting entries.

7. Prepare an adjusted trial balance.

8. Prepare an income statement for 2018 and a classified

9. Record closing entries.

10. Post closing entries

11. Prepare a post-closing trial balance.

Requirement – 1

To prepare: The T-accounts and enter the beginning balance from the trial balance.

Explanation of Solution

T-account:

T-account refers to an individual account, where the increases or decreases in the value of specific asset, liability, stockholder’s equity, revenue, and expenditure items are recorded.

This account is referred to as the T-account, because the alignment of the components of the account resembles the capital letter ‘T’.’ An account consists of the three main components which are as follows:

- (a) The title of the account

- (b) The left or debit side

- (c) The right or credit side

The T-accounts of given item in trial balance are as follows:

| Cash | |||

| Jan. 1 | $24,600 | ||

| Bal. | $20,000 | ||

| Accounts payable | |||

| Jan. 1 | $6,700 | ||

| Bal. | $6,700 | ||

| Common stock | |||

| Jan. 1 | $143,000 | ||

| Bal. | $143,000 | ||

|

Accounts receivables | |||

| Jan. 1 | $15,400 | ||

| Bal. | $15,400 | ||

| Prepaid Insurance | |||

| Jan. 1 | $12,000 | ||

| Bal. | $12,000 | ||

| Deferred revenue | |||

| Jan. 1 | $7,500 | ||

| Bal. | $7,500 | ||

| Land | |||

| Jan. 1 | 148,000 | ||

| Bal. | 148,000 | ||

| Retained earnings | |||

| Jan. 1 | $44,500 | ||

| Bal. | $44,500 | ||

Requirement – 2

To record: The journal entries for given transactions.

Explanation of Solution

Journal:

Journal is the method of recording monetary business transactions in chronological order. It records the debit and credit aspects of each transaction to abide by the double-entry system.

Rules of Debit and Credit:

Following rules are followed for debiting and crediting different accounts while they occur in business transactions:

- Debit, all increase in assets, expenses and dividends, all decrease in liabilities, revenues and stockholders’ equities.

- Credit, all increase in liabilities, revenues, and stockholders’ equities, all decrease in assets, expenses.

The journal entries for given transactions of Company Z are as follows:

| Date | Account Title and Explanation | Debit($) | Credit($) |

| 2018 | Accounts receivable | 52,200 | |

| January 9 | Cash | 134,100 | |

| Service revenue | 186,300 | ||

| (To record the recognized service revenue on account and cash) | |||

| 2018 | Cash | 51,500 | |

| February, 12 | Accounts receivable | 51,500 | |

| (To record cash collection from customer) | |||

| 2018 | Cash | 12,900 | |

| April 25 | Deferred revenue | 12,900 | |

| (To record the cash received in advance from customers) | |||

| 2018 | Supplies | 9,200 | |

| May 6 | Accounts payable | 9,200 | |

| (To record the purchase of supplies on account) | |||

| 2018 | Property tax expense | 8,500 | |

| July 15 | Cash | 8,500 | |

| (To record the payment of repairs and maintenance expense) | |||

| 2018 | Accounts payable | 11,400 | |

| September 10 | Cash | 11,400 | |

| (To record the payables on account ) | |||

| 2018 | Salaries expense | 123,600 | |

| October 31 | Cash | 123,600 | |

| (To record the payment of salaries for the current year) | |||

| 2018 | Cash | 27,000 | |

| ‘November 20 | Common stock | 27,000 | |

| (To record the payment of issuing shares of common stock) | |||

| 2018 | Dividends | 2,800 | |

| December 30 | Cash | 2,800 | |

| (To record the payment of dividends) | |||

Table (1)

Requirement – 3

To post: The transactions to T-accounts.

Explanation of Solution

T-account:

T-account refers to an individual account, where the increases or decreases in the value of specific asset, liability, stockholder’s equity, revenue, and expenditure items are recorded.

This account is referred to as the T-account, because the alignment of the components of the account resembles the capital letter ‘T’.’ An account consists of the three main components which are as follows:

- (a) The title of the account

- (b) The left or debit side

- (c) The right or credit side

T-accounts of above transactions are as follows:

| Cash | |||

| Jan. 1 | $24,600 | July. 15 | $8,500 |

| Jan.9 | $134,100 | Sep. 25 | $11,400 |

| Feb. 12 | $51,500 | Oct. 19 | $123,600 |

| April.25 | $12,900 | Dec. 30 | $2,800 |

| Nov.20 | $27,000 | ||

| Total | $250,100 | Total | $146,300 |

| Bal. | $103,800 | ||

| Supplies | |||

| Jan. 1 | $0 | ||

| May.6 | $9,200 | ||

| $9,200 | |||

| Deferred revenue | |||

| $5,800 | |||

| $12,900 | |||

| $18,700 | |||

| Dividends | |||

| $0 | |||

| $2,800 | |||

| $2,800 | |||

| Salaries expense | |||

| $0 | |||

| $123,600 | |||

| $123,600 | |||

| Accounts receivable | |||

| $15,400 | |||

| $52,200 | $51,500 | ||

| Land | |||

| Jan. 1 | $148,000 | ||

| Bal. | $148,000 | ||

| Common stock | |||

| Jan. 1 | $143,300 | ||

| Bal. | $27,000 | ||

| Service revenue | |||

| Jan. 1 | $0 | ||

| Bal. | $186,300 | ||

| Insurance expense | |||

| Jan. 1 | $0 | ||

| $0 | |||

| Prepaid Insurance | |||

| $12,000 | |||

| $12,000 | |||

| Accounts payable | |||

| $6.700 | |||

| $11,400 | $9.200 | ||

| $4,500 | |||

| Retained earnings | |||

| Jan. 1 | 44,500 | ||

| Bal. | $44,500 | ||

| Property Tax Expense | |||

| $0 | |||

| $8,500 | |||

| Supplies expense | |||

| $0 | |||

| $0 | |||

Requirement – 4

To prepare: The unadjusted trial balance of Company Z.

Explanation of Solution

Unadjusted trial balance:

The unadjusted trial balance is the summary of all the ledger accounts before making adjusting journal entries at the end of the period.

| Company Z | ||

| Unadjusted Trial Balance | ||

| December 31, 2018 | ||

| Accounts | Debit | Credit |

| Cash | $103,800 | |

| Accounts Receivable | 16,100 | |

| Prepaid Insurance | 12,000 | |

| Supplies | 9,200 | |

| Land | 148,000 | |

| Accounts Payable | 4,500 | |

| Deferred Revenue | 18,700 | |

| Common stock | 170,000 | |

| Retained earnings | 44,500 | |

| Dividends | 2,800 | 60,000 |

| Service Revenue | 186,300 | |

| Property Tax expense | 8,500 | |

| Salaries expense | 123,600 | |

| Insurance expense | 0 | |

| Supplies Expense | 0 | |

| Totals | $424,000 | $424,000 |

Table (2)

Therefore, the total of debit, and credit columns of unadjusted trial balance is $424,000 and agree.

Requirement – 5

To record: The given adjusting entries of Company Z.

Explanation of Solution

Adjusting entries:

Adjusting entries refers to the entries that are made at the end of an accounting period in accordance with revenue recognition principle, and expenses recognition principle. The purpose of adjusting entries is to adjust the revenue, and the expenses during the period in which they actually occurs.

Rules of Debit and Credit:

Following rules are followed for debiting and crediting different accounts while they occur in business transactions:

- Debit, all increase in assets, expenses and dividends, all decrease in liabilities, revenues and stockholders’ equities.

- Credit, all increase in liabilities, revenues, and stockholders’ equities, all decrease in assets, expenses.

Adjusting entries of Company R are as follows:

Accrued salaries:

| Date | Accounts title and explanation | Post Ref. | Debit ($) | Credit ($) |

| December 31, 2018 | Deferred Revenue | 11,800 | ||

| Service revenue | 11,800 | |||

| (To record the salaries expense incurred at the end of the accounting year) |

Table (3)

Following is the rule of debit and credit of above transaction:

- Deferred revenue is a liability, and it decreases the value of stockholder’s equity. Therefore, it is debited.

- Service revenue is a component of stockholders’ equity. There is an Increase in stockholders’ equity, therefore it is credited.

Depreciation expense:

| Date | Accounts title and explanation | Post Ref. | Debit ($) | Credit ($) |

| December 31, 2018 | Insurance Expense | 7,000 | ||

| Prepaid Insurance | 7,000 | |||

| (To record the amount of Reduced prepaid insurance due to passage of time) |

Table (4)

Following is the rule of debit and credit of above transaction:

- Insurance expense is an expense, and it decreased the value of stockholder’s equity. Therefore, it is debited.

- Prepaid Insurance is a contra-asset account. There is a decrease in assets, therefore it is credited.

Office supplies expense:

| Date | Accounts title and explanation | Post Ref. | Debit ($) | Credit ($) |

| December 31, 2018 | Supplies expense | 6,300 | ||

| Supplies | 6,300 | |||

| (To record the supplies expense incurred at the end of the accounting year) |

Table (5)

Following is the rule of debit and credit of above transaction:

- Supplies expense is an expense, and it decreased the value of stockholder’s equity. Therefore, it is debited.

- Supplies are an asset account. There is a decrease in assets, therefore it is credited.

Requirement – 6

To post: The adjusting entries to appropriate T-accounts.

Explanation of Solution

| Cash | |||

| Jan. 1 | $24,600 | July. 15 | $8,500 |

| Jan.9 | $134,100 | Sep. 25 | $11,400 |

| Feb. 12 | $51,500 | Oct. 19 | $123,600 |

| April.25 | $12,900 | Dec. 30 | $2,800 |

| Nov.20 | $27,000 | ||

| Total | $250,100 | Total | $146,300 |

| Bal. | $103,800 | ||

| Supplies | |||

| Jan. 1 | $0 | ||

| May.6 | $9,200 | $6,300 | |

| $2,900 | |||

| Deferred revenue | |||

| $5,800 | |||

| 11,800 | $12,900 | ||

| $6,900 | |||

| Dividends | |||

| $0 | |||

| $2,800 | |||

| $2,800 | |||

| Salaries expense | |||

| $0 | |||

| $123,600 | |||

| $123,600 | |||

| Accounts receivable | |||

| $15,400 | |||

| $52,200 | $51,500 | ||

| Land | |||

| Jan. 1 | $148,000 | ||

| Bal. | $148,000 | ||

| Common stock | |||

| Jan. 1 | $143,300 | ||

| Bal. | $27,000 | ||

| Total | $170,000 | ||

| Service revenue | |||

| Jan. 1 | $0 | ||

| Bal. | $186,300 | ||

| $11,800 | |||

| Total | $198,100 | ||

| Insurance expense | |||

| Jan. 1 | $0 | ||

| $7,000 | |||

| Total | $7,000 | ||

| Prepaid Insurance | |||

| $12,000 | |||

| $7,000 | |||

| $5,000 | |||

| Accounts payable | |||

| $6.700 | |||

| $11,400 | $9.200 | ||

| $4,500 | |||

| Retained earnings | |||

| Jan. 1 | 44,500 | ||

| Bal. | $44,500 | ||

| Property Tax Expense | |||

| $0 | |||

| $8,500 | |||

| Supplies expense | |||

| $0 | |||

| $6,300 | |||

Requirement – 7

To prepare: The adjusted trial balance of Company Z.

Explanation of Solution

Adjusted trial balance:

Adjusted trial balance is a summary of all the ledger accounts, and it contains the balances of all the accounts after the adjustment entries are journalized, and posted.

Adjusted trial balance of Company R is as follows:

| Company Z | ||

| Adjusted Trial Balance | ||

| December 31, 2018 | ||

| Accounts | Debit | Credit |

| Cash | 103,800 | |

| Accounts Receivable | 16,100 | |

| Prepaid insurance | 5,000 | |

| Supplies | 2,900 | |

| Land | 148,000 | |

| Accounts payable | 4,500 | |

| Deferred revenue | 6,900 | |

| Common stock | 170,000 | |

| Retained earnings | 44,500 | |

| Dividends | 2,800 | |

| Service revenue | 198,100 | |

| Property tax expense | 8,500 | |

| Salaries expense | 123,600 | |

| Insurance expense | 7,000 | |

| Supplies expense | 6,300 | |

| Totals | $424,000 | $424,000 |

Table (6)

Therefore, the total of debit, and credit columns of adjusted trial balance is $424,000 and agree.

Requirement – 8

To prepare: An income statement for 2018 and classified balance sheet as on December 31, 2018.

Explanation of Solution

Income statement:

This is the financial statement of a company which shows all the revenues earned and expenses incurred by the company over a period of time.

Classified balance sheet:

This is the financial statement of a company which shows the grouping of similar assets and liabilities under subheadings.

Income statement:

Income statement of Company Z is as follows:

| Company Z | ||

| Income statement | ||

| For the year ended December 31, 2018 | ||

| $ | $ | |

| Service revenue (A) | $198,100 | |

| Expenses: | ||

| Property tax | 8,500 | |

| Salaries | 123,600 | |

| Insurance | 7,000 | |

| Supplies | 6,300 | |

| Total expense (B) | 145,400 | |

| Net income

| 52,700 | |

Table (7)

Therefore, the net income of Company Z is $52,700.

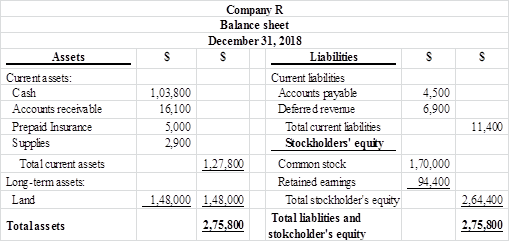

Classified balance sheet:

Classified balance sheet of Company Z is as follows:

Figure (1)

Therefore, the total assets of Company Z are $275,800, and the total liabilities and stockholders’ equity are $275,800.

Working note:

Calculation of ending balance retained earnings

Requirement – 9

To record: The necessary closing entries of Company R.

Explanation of Solution

Closing entries:

Closing entries are those journal entries, which are passed to transfer the final balances of temporary accounts, (all revenues account, all expenses account and dividend) to the retained earnings. Closing entries produce a zero balance in each temporary account.

Closing entries of Company R is as follows:

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| 2018 | Service revenue | 198,100 | ||

| December 31 | Retained earnings | 198,100 | ||

| (To close all revenue account) | ||||

| 2018 | Retained earnings | 145,400 | ||

| December 31 | Property tax expense | 8,500 | ||

| Salaries expense | 123,600 | |||

| Insurance expense | 7,000 | |||

| 0 | Supplies expense | 6,300 | ||

| (To close all the expenses account) | ||||

| 2018 | Retained earnings | 2,800 | ||

| December 31 | Dividends | 2,800 | ||

| (To close the dividends account) | ||||

Table (8)

Requirement – 10

To post: The closing entries to the T-accounts.

Explanation of Solution

| Cash | |||

| Jan. 1 | $24,600 | July. 15 | $8,500 |

| Jan.9 | $134,100 | Sep. 25 | $11,400 |

| Feb. 12 | $51,500 | Oct. 19 | $123,600 |

| April.25 | $12,900 | Dec. 30 | $2,800 |

| Nov.20 | $27,000 | ||

| Total | $250,100 | Total | $146,300 |

| Bal. | $103,800 | ||

| Supplies | |||

| Jan. 1 | $0 | ||

| May.6 | $9,200 | $6,300 | |

| $2,900 | |||

| Deferred revenue | |||

| $5,800 | |||

| 11,800 | $12,900 | ||

| $6,900 | |||

| Dividends | |||

| $0 | |||

| $2,800 | $2,800 | ||

| $0 | |||

| Salaries expense | |||

| $0 | |||

| $123,600 | $123,600 | ||

| $0 | |||

| Accounts receivable | |||

| $15,400 | |||

| $52,200 | $51,500 | ||

| Land | |||

| Jan. 1 | $148,000 | ||

| Bal. | $148,000 | ||

| Common stock | |||

| Jan. 1 | $143,300 | ||

| Bal. | $27,000 | ||

| Total | $170,000 | ||

| Service revenue | |||

| Jan. 1 | $0 | ||

| Bal. | $186,300 | ||

| $11,800 | |||

| Total | $198,100 | ||

| Insurance expense | |||

| Jan. 1 | $0 | ||

| $7,000 | $7,000 | ||

| $0 | |||

| Prepaid Insurance | |||

| $12,000 | |||

| $7,000 | |||

| $5,000 | |||

| Accounts payable | |||

| $6.700 | |||

| $11,400 | $9.200 | ||

| $4,500 | |||

| Retained earnings | |||

| Jan. 1 | 44,500 | ||

| Bal. | $44,500 | ||

| Property Tax Expense | |||

| $0 | |||

| $8,500 | $8,500 | ||

| $0 | |||

| Supplies expense | |||

| $0 | |||

| $6,300 | $6,300 | ||

| $0 | |||

Requirement – 11

To prepare: A post-closing trial balance of Company Z.

Explanation of Solution

Post-closing trial balance:

The post-closing trial balance is a summary of all ledger accounts, and it shows the debit and the credit balances after the closing entries are journalized and posted. The post-closing trial balance contains only permanent (balance sheet) accounts, and the debit and the credit balances of permanent accounts should agree.

Post-closing trial balance of Company R is as follows:

| Company Z | ||

| Post-closing trial balance | ||

| December 31, 2018 | ||

| Accounts | Debit Amount($) |

Credit Amount($) |

| Cash | $103,800 | |

| Accounts Receivable | 16,100 | |

| Prepaid Insurance | 5,000 | |

| Supplies | 2,900 | |

| Land | 148,000 | |

| Accounts payable | 4,500 | |

| Deferred revenue | 6,900 | |

| Common stock | 170,000 | |

| Retained Earnings | 94,400 | |

| Totals | $275,800 | $275,800 |

Table (9)

Therefore, the total of debit, and credit columns of post-closing trial balance is $275,800 and agree.

Want to see more full solutions like this?

Chapter 3 Solutions

FINANCIAL ACCOUNTINGLL W/CONNECT >IC<

- On January 1, 2021, the general ledger of Big Blst Fireworks includes the following account balances: Debit $ 23, 300 Accounts Credit Cash Accounts Receivable Allowance for Uncollectible Accounts Inventory Land Accounts Payable Notes Payable (6%, due in 3 years) 48, e00 $ 4, 580 37,e00 72,100 28,900 37,8ee 63,0ne 39,eee Common Stack Retained Earnings Totals $172, 488 $172,480 The $37,000 beginning balance of inventory consists of 370 units, esch costing $100. During Janusry 2021, Big Blest Fireworks had the following inventory transactions: January 3 Purchase 1,688 units for $168,888 on account ($18s each). January 8 Purchase 1,78e units for $187, 800 on account ($118 cach). January 12 Purchase 1,88e units for $287, e00 on account ($115 cach). January 15 Return 135 of the units purchased on January 12 because of defects. January 19 Sell 5,2ee units on account for $788,eee. The cost of the units sold is deternined using a FIFO perpetual inventory systen. January 22 Receive $753, eee…arrow_forwardRequired Information On January 1, 2024, the general ledger of TNT Fireworks includes the following account balances: Accounts Cash Accounts Receivable Debit Credit $ 58,800 25,200 Allowance for Uncollectible Accounts $ 2,300 Inventory 36,400 Notes Receivable (5%, due in 2 years) 13,200 156,000 Common Stock 14,900 221,800 51,488 Land Accounts Payable Retained Earnings Totals $ 289,600 $ 289,600 During January 2024, the following transactions occur: January 1 Purchase equipment for $19,600. The company estimates a residual value of $1,608 and a six-year service life. January 4 Pay cash on accounts payable, $9,600. January 8 Purchase additional inventory on account, $83,980. January 15 Receive cash on accounts receivable, $22,100. January 19 Pay cash for salaries, $29,900. January 28 Pay cash for January utilities, $16,500. January 30 Firework sales for January total $221,088. All of these sales are on account. The cost of the units sold is $115,500. Information for adjusting entries: a.…arrow_forwardThe details of the accounts receivable of AA Corporation as December 31, 2022 shows the following: Beginning balance P3,450,000 Sales on account made to customers 2,800,000 Collection of accounts receivable during the year 4,200,000 Accounts written off as uncollectible 90,000 The following transactions were included in the recorded transactions during the year: 1. Invoice dated December 28, 2022 for P350,000 was shipped and received by the buyer on December 31, 2022, this invoice was recorded in the book at P35,000. 2. Invoice dated and recorded on November 30, 2022 was erroneously priced at P32 per unit. There were 11,000 units of goods delivered which were received on December 10, 2022. The agreed price should be at P22 per unit only. AA's policy is to provide 5% of the outstanding balance of accounts receivable as uncollectible and there is beginning balance of allowance for bad debts of P40,000. Statement 1: The amount of bad debt expense in 2022 is P158,250. Statement 2: The…arrow_forward

- On January 1, 2021, the general ledger of Big Blest Fireworks includes the following account balances: Accounts Cash Debit Credit $ 23,300 48, e00 Accounts Receivable Allowance for Uncollectible Accounts $ 4, See Inventory Land 37,800 72,108 Accounts Payable Notes Payable (6%, due in 3 years) Comnon Stack 28,9ee 37,000 63, 0e0 Retained Earnings 39,0e0 Totals $172,400 $172,48e The $37,000 beginning balance of inventory consists of 370 units, eoch costing $100. During Janusry 2021, Big Blast Fireworks had the following inventory transections: January 3 Purchase 1,6e0 units for $168,80e on account ($18s cach). January 8 Purchase 1,78e units for $187,000 on account ($11e cach). January 12 Purchase 1,8e0 units for $287, B0e on account ($115 cach). January 15 Return 135 of the units purchased on 3anuary 12 because of defcects. January 19 sell 5,280 units on account for $788,eee. The cost of the units sold is deternined using a FIFO perpetual inventory systen. January 22 Receive $753, eee…arrow_forwardOn January 1, 2021, the general ledger of TNT Fireworks includes the following account balances: Accounts Debit Credit Cash $ 59,000 Accounts Receivable 25,600 Allowance for Uncollectible Accounts $ 2,500 36,600 Inventory Notes Receivable (5%, due in 2 years) 15,600 Land 158,000 Accounts Payable 15,100 Common Stock 223,000 Retained Earnings 54,200 Totals $294,800 $294,800 During January 2021, the following transactions occur: January 1 Purchase equipment for $19,800. The company estimates a residual value of $1,800 and a six-year service life. January 4 Pay cash on accounts payable, $9,800. January 8 Purchase additional inventory on account, $85,900. January 15 Receive cash on accounts receivable, $22,30O. January 19 Pay cash for salaries, $30,100. January 28 Pay cash for January utilities, $16,800. January 30 Sales for January total $223,000. All of these sales are on account. The cost of the units sold is $116,500. Information for adjusting entries: a. Depreciation on the equipment…arrow_forwardOn January 1, 2021, the general ledger of Big Blest Fireworks includes the following account balances: Accounts Debit Credit Cash $ 23, 308 Accounts Receivable Allowance for Uncollectible Accounts 48, B00 $ 4, 580 Inventory Land Accounts Payable Notes Payable (6%, due in 3 years) 37, e00 72,100 28,980 37,000 Comnon Stack Retained Earnings 63, eee 39,eee Totals $172,400 $172,400 The $37,000 beginning belance of inventory consists of 370 units, each costing S100. During Janusry 2021, Big Blast Fireworks had the following inventory transactions: January 3 Purchase 1,68e units for 168,088 on account ($10s cach). January 8 Purchase 1,78e units for $187, 880 on account ($110 cach). January 12 Purchase 1,88e units for $287,000 on account ($115 cach). January 15 Return 135 of the units purchased on 3anuary 12 because of defccts. January 19 Sell 5,2ee units on account for $788,8ee. The cost of the units sold is deternined using a FIFO perpetual inventory systen. January 22 Receive $753, eee…arrow_forward

- Ablema has provided you with the following bank statement and bank account details in respect of the month ended 31 January 2018. Statement date - 31 January, 2018. Account No 1452800 Date Particulars Debit Credit Balance GH¢ GH¢ GH¢ 01-Jan-18 Balance forward 67,580 Cr 06-Jan-18 Cheque 597 120 67,460 Cr 06-Jan-18 Direct debit 2,020 65,440 Cr 12-Jan-18 Credit transfer 4,660 70,100 Cr 13-Jan-18 Cheque 600 1,420 68,680 Cr 14-Jan-18 Cheque 601 12,028 56,652 Cr 16-Jan-18 Lodgement 9,000 65,652 Cr 19-Jan-18 Cheque 599 18,004 47,648 Cr 23-Jan-18 Bank charges for December 2017 422 47,226 Cr 25-Jan-18 Quarterly interest received 62 47,288 Cr 27-Jan-18 Dishonoured cheque 1,600 45,688 Cr 27-Jan-18 Cheque 598 26,090 19,598 Cr 30-Jan-18 Cheque 603 5,048 14,550 Cr 31-Jan-18 Lodgement 14,500 29,050 Cr 31-Jan-18 Standing order: rent first quarter 2018 27,000 2,050 Cr The books and records of Ablema show the followings transactions through the bank account for the month of January 2018: Date Receipts…arrow_forwardFinancial statement data for the years ended December 31 for Parker Corporation are as follows: Sales Accounts receivable: Beginning of year End of year Current Year Current Year $2,595,600 Current Year 390,000 434,000 a. Determine the accounts receivable turnover for each year. Round your answers to one decimal place. Accounts Receivable Turnover times times Prior Year $2,409,500 400,000 390,000 Prior Year b. Determine the days' sales in receivables for each year. Round your answers to nearest day. Assume 365 days per year. Number of Days' Sales in Receivables days days Prior Year c. Does the change in accounts receivable turnover and days' sales in receivables from the first year to the second year indicate a favorable or unfavorable change?arrow_forwardThe following is the summary of transactions of AA Company in 2021 and 2022: 2022 2021 Credit sales P6,000,000 P5,620,000 Collections of outstanding receivables 5,830,000 4,800,000 Accounts written off 60,000 20,000 Recovery of accounts previously written off 15,000 none Days past invoice date at December 31 2022 2021 0-30 600,000 500,000 31 90 150,000 180,000 91 180 110,000 Over 180 30,000 The company's policy to provide allowance on its account receivable at year end as follows: 0-30 days - 2%; 31-90 days - 5%; 91-180 days - 10%; and over 180 days - 20%. Statement 1; The balance of allowance for uncollectible account as of December 31, 2021 is P34,000. Statement 2:The balance of allowance for uncollectible accounts as of December 31, 2022 is P39,500.arrow_forward

- On January 1, 2021, the general ledger of Big Bles: Fireworks includes the following account balances: Accounts Cash Debit Credit $ 23, 308 48, e0e Accounts Receivable Allowance for Uncollectible Accounts $ 4, 580 37, eee Inventory Land 72,100 Accounts Payable Notes Payable (6%, duc in 3 years) 28,98e 37,eee 63,0ee 39,8ee Comnon Stock Retained Earnings Totals $172,400 $172, 400 The $37,000 beginning belance of inventory consists of 370 units, each costing $100. During January 2021, Big Blast Fireworks had the following inventory transactions: January 3 Purchase 1,680 units for $168,89e on account ($185 cach). January 8 Purchase 1,78e units for $187, e0e on account ($110 each). January 12 Purchase 1,88e units for $207, B00 on account ($115 cach). January 15 Return 135 of the units purchased on January 12 because of defects. January 19 Sell 5,2ee units on account for $788, eee. The cost of the units sold is deternined using a FIFO perpetual inventory syston. January 22 Receive $753, eee…arrow_forwardOn January 1, 2021, the general ledger of Big Blest Fireworks includes the following account balances: Accounts Debit Credit Cash Accounts Receivable Allowance for Uncollectible Accounts $ 23, 300 48, e00 $ 4, 580 Inventory Land Accounts Payable Notes Payable (6%, due in 3 ycars) 37, 200 72,188 28,980 37,000 63, 0ee 39, 0ee Common Stock Retained Earnings Totals $172,400 $172,480 The $37,000 beginning balance of inventory consists of 370 units, eoch costing $100. During Janusry 2021, Big Blast Fireworks had the following inventory transections: January 3 Purchase 1,62e units for $168, 800 on account ($1es cach). January 8 Purchase 1,7e8 units for $187,800 on account ($118 cach). January 12 Purchase 1,88e units for $207, 8ee on account ($115 cach). January 15 Return 135 of the units purchased on January 12 because of defects. January 19 Sell 5,200 units on account for $780,eee. The cost of the units sold is deternined using a FIFO perpetual inventory systen. January 22 Receive $753, eee…arrow_forwardThe following data are taken from the financial statements of Colby Company. Accounts receivable (net), end of year Net sales on account Terms for all sales are 1/10, n/45 Accounts Receivable turnover Average collection period (b) 2022 $550,000 2022 2021 4,300,000 4,000,000 7.9 times $540,000 2021 7.5 times 46.2 days 48.7 days What conclusions about the management of accounts receivable can be drawn from the accounts receivable turnover and the average collections period.arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education