Concept explainers

Videos

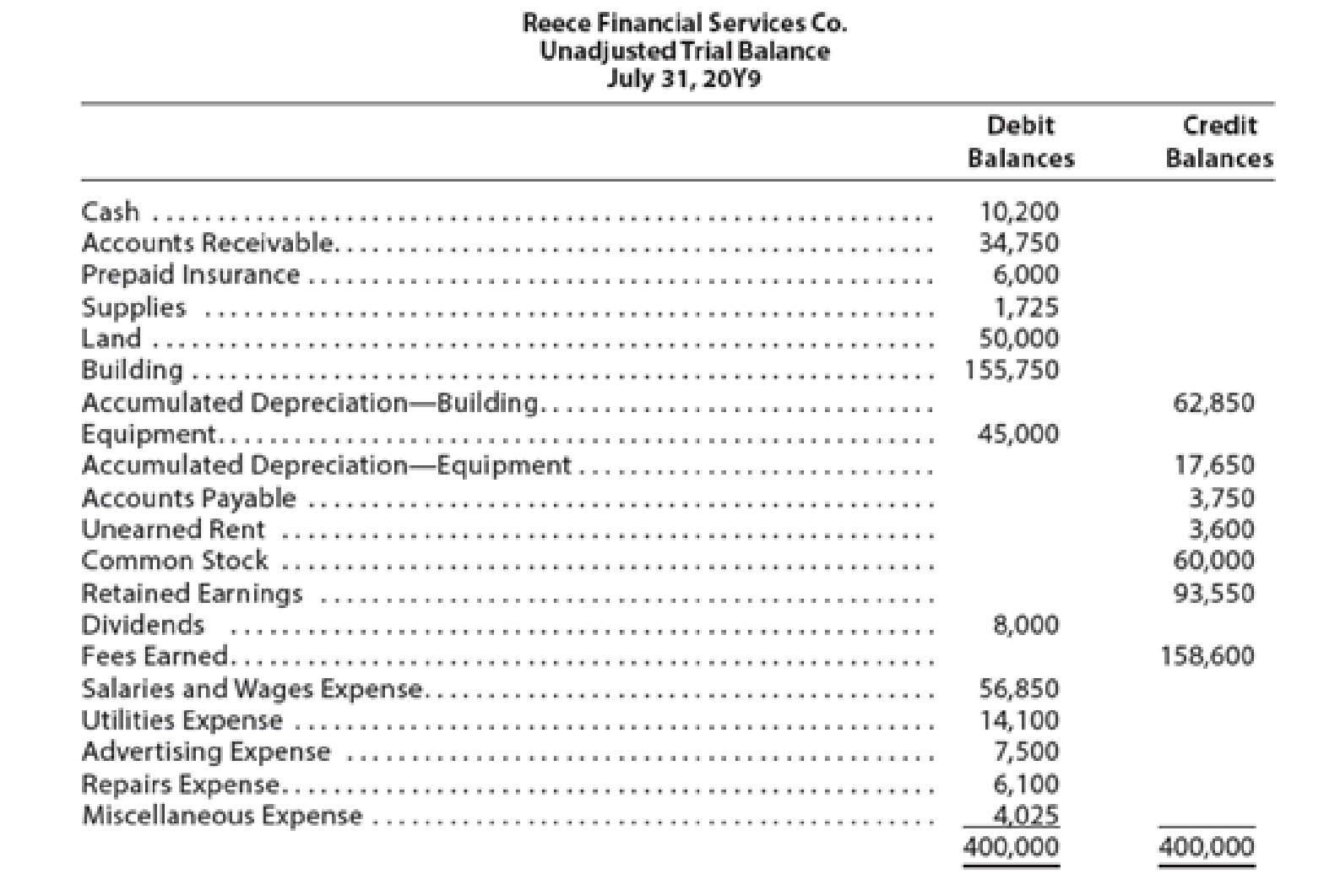

Reece Financial Services Co., which specializes in appliance repair services, is owned and operated by Joni Reece. Reece Financial Services’ accounting clerk prepared the following unadjusted

The data needed to determine year-end adjustments are as follows:

•

• Depreciation of equipment for the year, $2,800.

• Accrued salaries and wages at July 31, $900.

• Unexpired insurance at July 31, $1,500.

• Fees earned but unbilled on July 31, $10,200.

• Supplies on hand at July 31, $615.

• Rent unearned at July 31, $300.

Instructions

1. Journalize the adjusting entries using the following additional accounts: Salaries and Wages Payable; Rent Revenue; Insurance Expense; Depreciation Expense—Building; Depreciation Expense— Equipment; and Supplies Expense.

2. Determine the balances of the accounts affected by the adjusting entries, and prepare an adjusted trial balance.

1.

Prepare the adjusting entries on July 31, 20Y9 of Company RFS.

Explanation of Solution

Adjusting Entries:

Adjusting entries indicates those entries, which are passed in the books of accounts at the end of one accounting period. These entries are passed in the books of accounts as per the revenue recognition principle and the expenses recognition principle to adjust the revenue, and the expenses of a business in the period of their occurrence.

Rule of Debit and Credit:

Debit - Increase in all assets, expenses & dividends, and decrease in all liabilities and stockholders’ equity.

Credit - Increase in all liabilities and stockholders’ equity, and decrease in all assets & expenses.

The adjusting entry for recording depreciation for building is as follows:

| Date | Account Titles and Explanation | Debit ($) | Credit ($) |

| July 31 | Depreciation expense | 6,400 | |

| Accumulated Depreciation- building | 6,400 | ||

| (To record the depreciation on building for the current year.) |

Table (1)

- Depreciation expense is component of stockholders’ equity and decreased it, so debit depreciation expense by $6,400.

- Accumulated depreciation is a contra asset account, and it decreases the asset value by $6,400. So credit accumulated depreciation by $6,400.

The adjusting entry for recording depreciation for equipment is as follows:

| Date | Account Titles and Explanation | Debit ($) | Credit ($) |

| July 31 | Depreciation expense | 2,800 | |

| Accumulated Depreciation- equipment | 2,800 | ||

| (To record the depreciation on equipment for the current year.) |

Table (2)

- Depreciation expense is component of stockholders’ equity and decreased it, so debit depreciation expense by $2,800.

- Accumulated depreciation is a contra asset account, and it decreases the asset value by $2,800. So credit accumulated depreciation by $2,800.

The following entry shows the adjusting entry for Salary and wages expense on July 31.

| Date | Account Titles and Explanation | Debit ($) | Credit ($) |

| July 31 | Salary and wages expense | 900 | |

| Wages Payable | 900 | ||

| (To record the salary and wages accrued but not paid at the end of the accounting period.) |

Table (3)

- Salary and wages expense is a component of Stockholders ‘equity, and it decreased it by $900. So debit wage expense by $900.

- Salary and wages payable is a liability, and it is increased by $900. So credit Salary and wages payable by $900.

The following entry shows the adjusting entry for unexpired insurance on July 31.

| Date | Description |

Post. Ref |

Debit ($) |

Credit ($) |

| July 31 | Insurance expense (1) | 4,500 | ||

| Prepaid insurance | 4,500 | |||

| (To record the insurance expense incurred at the end of the year) |

Table (4)

Working note (1):

Calculate the value of insurance expense at the end of the year:

- Insurance expense is a component of owners’ equity, and decreased it by $4,500 hence debit the insurance expense for $4,500.

- Prepaid insurance is an asset, and it decreases the value of asset by $4,500, hence credit the prepaid insurance for $4,500.

The following entry shows the adjusting entry for accrued fees unearned on July 31.

| Date | Account Titles and Explanation | Debit ($) | Credit ($) |

| July 31 | Accounts Receivable | 10,200 | |

| Fees earned | 10,200 | ||

| (To record the accounts receivable at the end of the year.) |

Table (5)

- Accounts Receivable is an asset, and it is increased by $10,200. So debit Accounts receivable by $10,200.

- Fees earned are component of stockholders’ equity, and it increased it by $10,200. So credit fees earned by $10,200.

The following entry shows the adjusting entry for supplies on July 31.

| Date | Account Titles and Explanation | Debit ($) | Credit ($) |

| July 31 | Supplies Expense (2) | 1,110 | |

| Supplies | 1,110 | ||

| (To record the supplies expense at the end of the accounting period) |

Table (6)

- Supplies expense is a component of stockholders’ equity, and it decreased the stockholders’ equity by $1,110. So debit supplies expense by $1,110.

- Supplies are an asset for the business, and it is decreased by $1,110. So credit supplies by $1,110.

Working Note (2):

Calculation of Supplies expense for the accounting period

The following entry shows the adjusting entry for unearned Rent on July 31.

| Date | Account Titles and Explanation | Debit ($) | Credit ($) |

| July 31 | Unearned Rent | 3,300 | |

| Rent revenue (3) | 3,300 | ||

| (To record the Rent revenue from services at the end of the accounting period.) |

Table (7)

- Unearned Rent is a liability, and it is decreased by $3,300. So debit unearned rent by $3,300.

- Rent revenue is a component of Stockholders’ equity, and it is increased by $3,300. So credit rent revenue by $3,300.

Working Notes (3):

Calculation of Rent Revenue for the accounting period

2.

Prepare the adjusted trial balance of the Company RFS on July 31, 20Y9.

Explanation of Solution

Adjusted Trial Balance

Adjusted trial balance is a trial balance prepared at the end of a financial period, after all the adjusting entries are journalized and posted. It is prepared to prove the equality of the total debit and credit balances.

The adjusted trial balance of the Company RFS is as follows:

| Company RFS | ||

| Trial Balance after Adjustments | ||

| July 31, 20Y9 | ||

| Particulars | Debit $ | Credit $ |

| Cash | 10,200 | |

| Accounts Receivable(5) | 44,950 | |

| Prepaid Insurance | 1,500 | |

| Supplies | 615 | |

| Land | 50,000 | |

| Building | 155,750 | |

| Accumulated Depreciation - Building(1) | 69,250 | |

| Equipment | 45,000 | |

| Accumulated Depreciation - Equipment(2) | 20,450 | |

| Accounts Payable | 3,750 | |

| Unearned Rent | 300 | |

| Salaries and Wages Payable | 900 | |

| Capital | 153,550 | |

| Drawing | 8,000 | |

| Fees earned | 168,800 | |

| Rent Revenue (7) | 3,300 | |

| Salaries and Wages Expense (3) | 57,750 | |

| Utilities Expense | 14,100 | |

| Advertising Expense | 7,500 | |

| Repairs Expense | 6,100 | |

| Depreciation Expense - building | 6,400 | |

| Depreciation Expense - equipment | 2,800 | |

| Insurance Expense (4) | 4,500 | |

| Supplies Expense (6) | 1,110 | |

| Miscellaneous Expense | 4,025 | |

| 420,300 | 420,300 | |

Table (8)

1. Calculation of accumulated depreciation- building

2. Calculation of accumulated depreciation- equipment

3. Calculation of Salaries and Wages expenses

4. Calculate the value of insurance expense at the end of the year

5. Calculation of accounts receivable

6. Calculation of Supplies expense for the accounting period

7. Calculation of rent revenue:

Want to see more full solutions like this?

Chapter 3 Solutions

Financial And Managerial Accounting

- Prepare adjusting journal entries, as needed, considering the account balances excerpted from the unadjusted trial balance and the adjustment data. A. supplies actual count at year end, $6,500 B. remaining unexpired insurance, $6,000 C. remaining unearned service revenue, $1,200 D. salaries owed to employees, $2,400 E. depreciation on property plant and equipment, $18,000arrow_forwardWolfpack Corp. has determined it should record depreciation expense of $40,000 for the year ending 12/31/X7. Required: In the general journal below, complete the year-end entry to record depreciation. Debit Credit Dec 31 ? 40,000 ? 40,000arrow_forwardCALCULATING AND JOURNALIZING DEPRECIATION Equipment records for Byerly Construction Co. for the year follow. Byerly Construction uses the straight-line method of depreciation. In the case of assets acquired by the fifteenth day of the month, depreciation should be computed for the entire month. In the case of assets acquired after the fifteenth day of the month, no depreciation should be considered for the month in which the asset was acquired. REQUIRED 1. Calculate the depreciation expense for Byerly Construction as of December 31, 20--. 2. Prepare the entry for depreciation expense using a general journal.arrow_forward

- Complete the work sheet for Ramey Company, dated December 31, 20, through the adjusted trial balance using the following adjustment information: a. Expired or used-up insurance, 460. b. Depreciation expense on equipment, 870. (Remember to credit the Accumulated Depreciation account for equipment, not Equipment.) c. Wages accrued or earned since the last payday, 120 (owed and to be paid on the next payday). d. Supplies remaining, 80.arrow_forwardPrepare adjusting journal entries, as needed, considering the account balances excerpted from the unadjusted trial balance and the adjustment data. A. depreciation on buildings and equipment, $17,500 B. advertising still prepaid at year end, $2,200 C. interest due on notes payable, $4,300 D. unearned rental revenue, $6,900 E. interest receivable on notes receivable, $1,200arrow_forwardCALCULATING AND JOURNALIZING DEPRECIATION Equipment records for Johnson Machine Co. for the year follow. Johnson Machine uses the straight-line method of depreciation. In the case of assets acquired by the fifteenth day of the month, depreciation should be computed for the entire month. In the case of assets acquired after the fifteenth day of the month, no depreciation should be considered for the month in which the asset was acquired. REQUIRED 1. Calculate the depreciation expense for Johnson Machine as of December 31, 20--. 2. Prepare the entry for depreciation expense using a general journal.arrow_forward

- Required: 1. Prepare general journal entries to record the preceding transactions. 2. Post to general ledger T-accounts. 3. Prepare a year-end trial balance on a worksheet and complete the worksheet using the following information: (a) accrued salaries at year-end total $1,000. (b) for simplicity, the building and equipment are being depreciated using the straight- line method over an estimated life of 20 years with no residual value. (c) supplies on hand at the end of the year total $600. (d) bad debts expense for the year totals $610; and (e) the income tax rate is 30%; income taxes are payable in the first quarter of 2017.arrow_forwardAdjustment for Depreciation The estimated amount of depreciation on a building for the current year is $4,680. Journalize the adjusting entry to record the depreciation. If an amount box does not require an entry, leave it blank.arrow_forwardInstructions On December 31, it was estimated that goodwill of $4,084,600 was impaired. In addition, a patent with an estimated useful economic life of 18 years was acquired for $510,720 on April 1. A. Journalize the adjusting entry on December 31 for the impaired goodwill. Refer to the Chart of Accounts for exact wording of account titles. B. Journalize the adjusting entry on December 31 for the amortization of the patent rights. Refer to the Chart of Accounts for exact wording of account titles.arrow_forward

- Required 1. Prepare and complete a 10-column work sheet for fiscal year 2019, starting with the unadjusted trial balance and including adjustments based on these additional facts. a. The supplies available at the end of fiscal year 2019 had a cost of $7,900. b. The cost of expired insurance for the fiscal year is $10,600. c. Annual depreciation on equipment is $7,000. d. The April utilities expense of $800 is not included in the unadjusted trial balance because the bill arrived after the trial balance was prepared. The $800 amount owed needs to be recorded. e. The company’s employees have earned $2,000 of accrued and unpaid wages at fiscal year-end. f. The rent expense incurred and not yet paid or recorded at fiscal year-end is $3,000. g. Additional property taxes of $550 have been assessed for this fiscal year but have not been paid or recorded in the accounts. h. The $300 accrued interest for April on the long-term notes payable has not yet been paid or recorded. 2. Using information…arrow_forwardWillow Creek Company purchased and installed carpet in its new general offices on April 30 for a total cost of $36,288. The carpet is estimated to have a 16-year useful life and no residual value. A. Prepare the journal entry necessary for recording the purchase of the new carpet. Refer to the Chart of Accounts for exact wording of account titles. B. Record the December 31 adjusting entry for the partial-year depreciation expense for the carpet, assuming that Willow Creek Company uses the straight-line method. Refer to the Chart of Accounts for exact wording of account titles. CHART OF ACCOUNTS Willow Creek Company General Ledger ASSETS 110 Cash 111 Petty Cash 112 Accounts Receivable 114 Interest Receivable 115 Notes Receivable 116 Merchandise Inventory 117 Supplies 119 Prepaid Insurance 120 Land 123 Carpet 124 Accumulated Depreciation-Carpet 125 Equipment 126 Accumulated Depreciation-Equipment 130 Mineral Rights 131…arrow_forwardPreparing and Journalizing Adjusting Entries For each of the following separate situations, prepare the necessary adjustments (a) using the finan- cial statement effects template, and (b) in journal entry form. 1. Unrecorded depreciation on equipment is $610. 2.Onthedateforpreparingfinancialstatements,anestimatedutilitiesexpenseof$390hasbeen incurred, but no utility bill has yet been received or paid. 3.Onthefirstdayofthecurrentperiod,rentforfourperiodswaspaidandrecordedasa$2,800 debit to Prepaid Rent and a $2,800 credit to Cash. 4.Ninemonthsago,the Hartford Financial Services Group soldaone-yearpolicytoacustomer andrecordedthereceiptofthepremiumbydebitingCashfor$624andcreditingContract Liabilitiesfor$624.Noadjustingentrieshavebeenpreparedduringthenine-monthperiod. Hartford’s annual financial statements are now being prepared. 5.Attheendoftheperiod,employeewagesof$965havebeenincurredbutnotyetpaidor recorded. 6. At the end of the period, $300 of interest income has been earned but not…arrow_forward

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub