Concept explainers

Videos

Sales and Purchases

Ms. Valli of All About You Spa has decided to expand her business by adding two lines of merchandise—a selection of products used in the salon for the body, the feet, and the face, as well as logo mugs, T-shirts, and baseball caps that can provide advertising benefits. She believes she will be able to increase her profits significantly.

July

So that you can complete the journal entries for the month of July, Ms. Valli has also left the information you will need and directions on how to proceed.

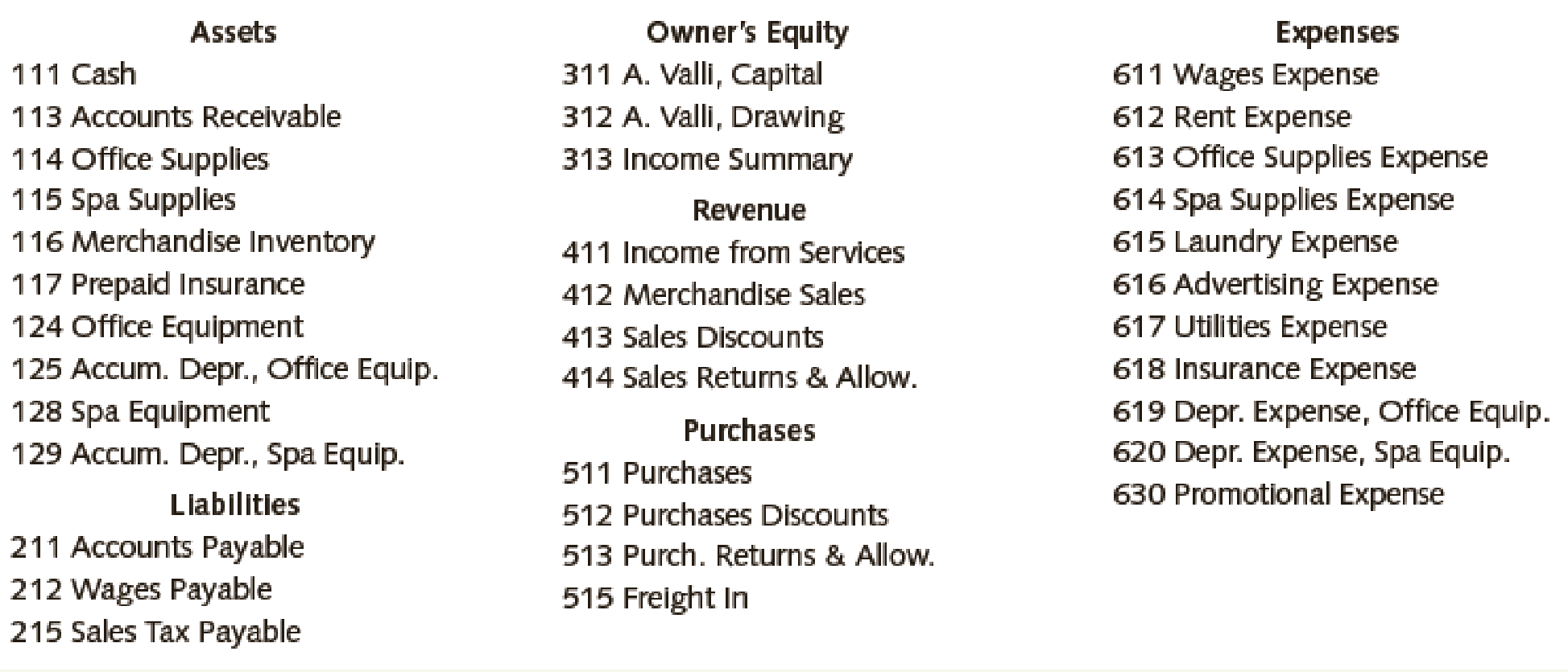

Note that with the expansion of the business into merchandising, new accounts have been added to the chart of accounts. For example, an additional revenue account, Merchandise Sales, is needed. Because All About You Spa now needs a Purchases account, the chart of accounts needs to be modified as follows: The 500–599 range is used for the purchase-related accounts (for example, Purchases 511 and Freight In 515). Your new chart of accounts is as follows:

CHART OF ACCOUNTS FOR ALL ABOUT YOU SPA

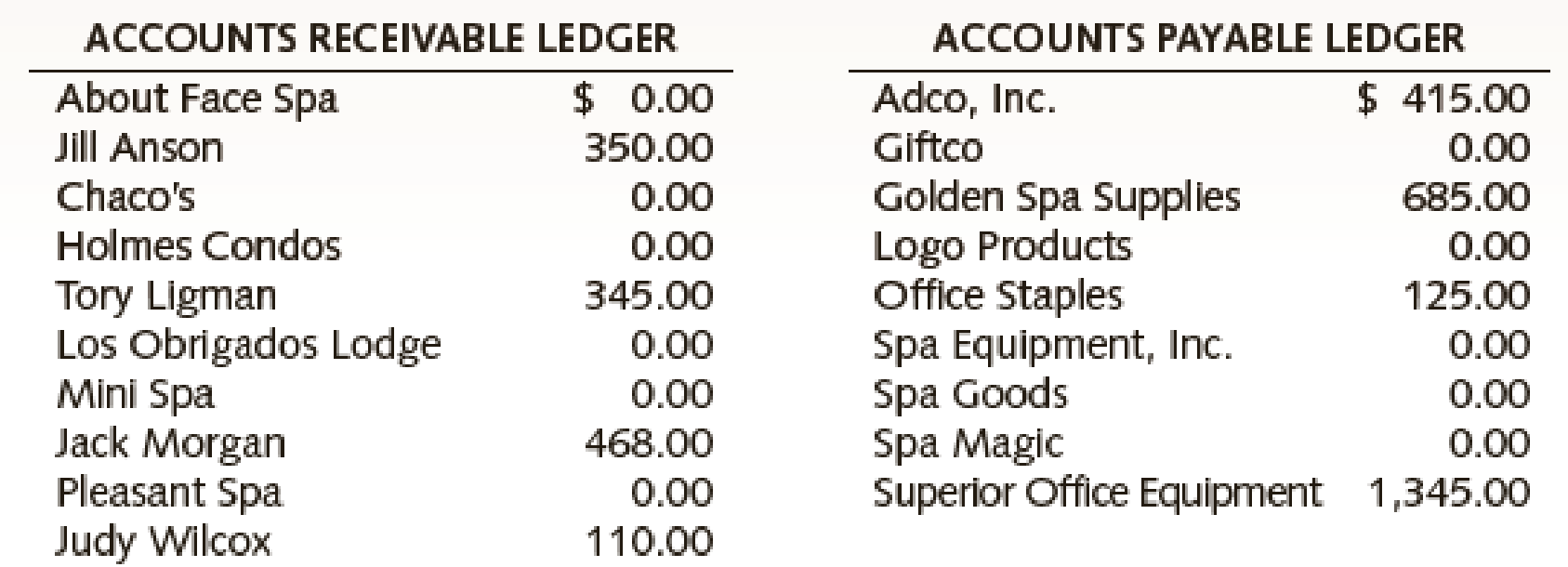

Also note that because you will be making purchases on account and sales on account, subsidiary ledgers will be needed to track what is due from individual customers and owed to individual vendors. A listing of customers and vendors with current balances are as follows:

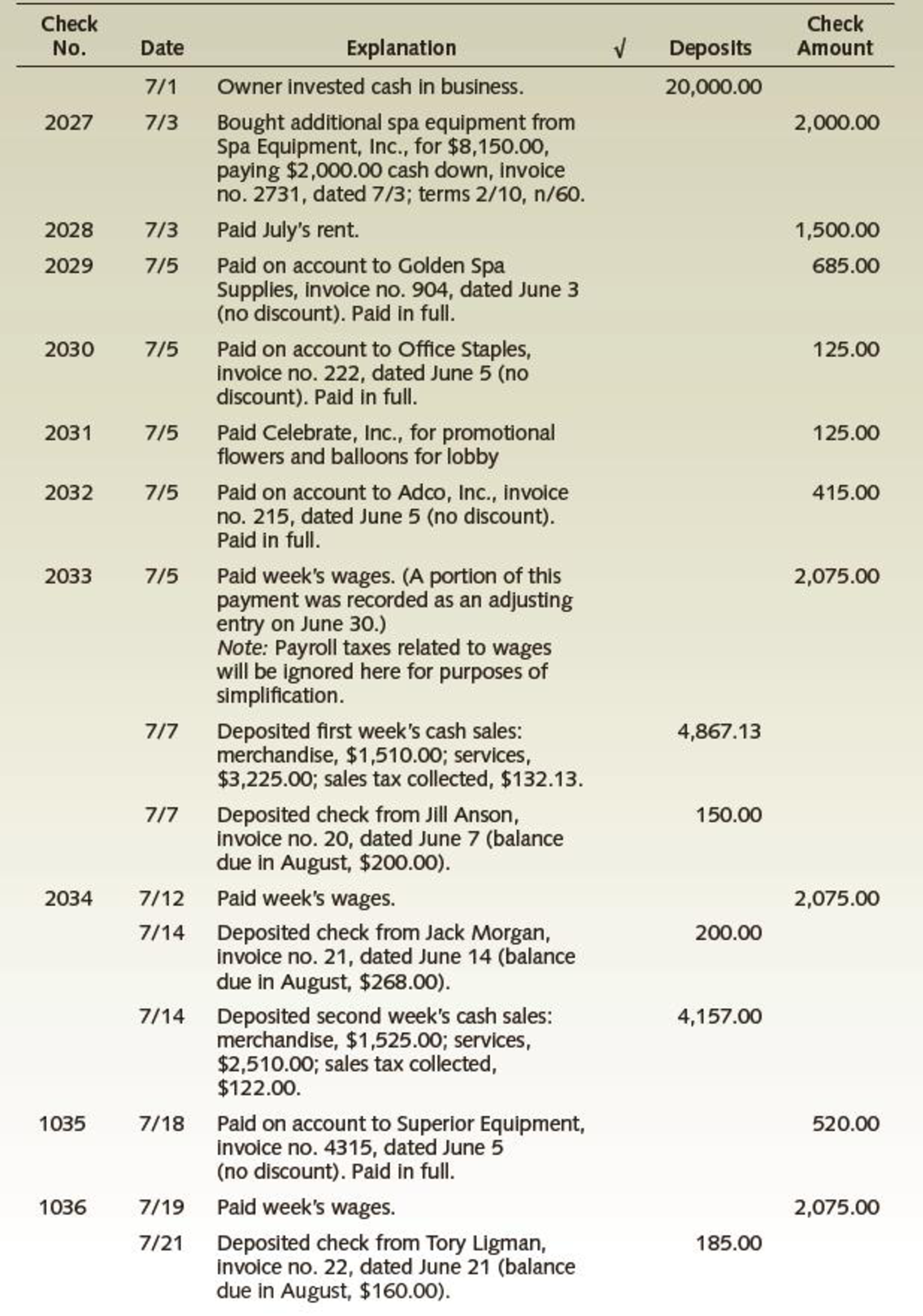

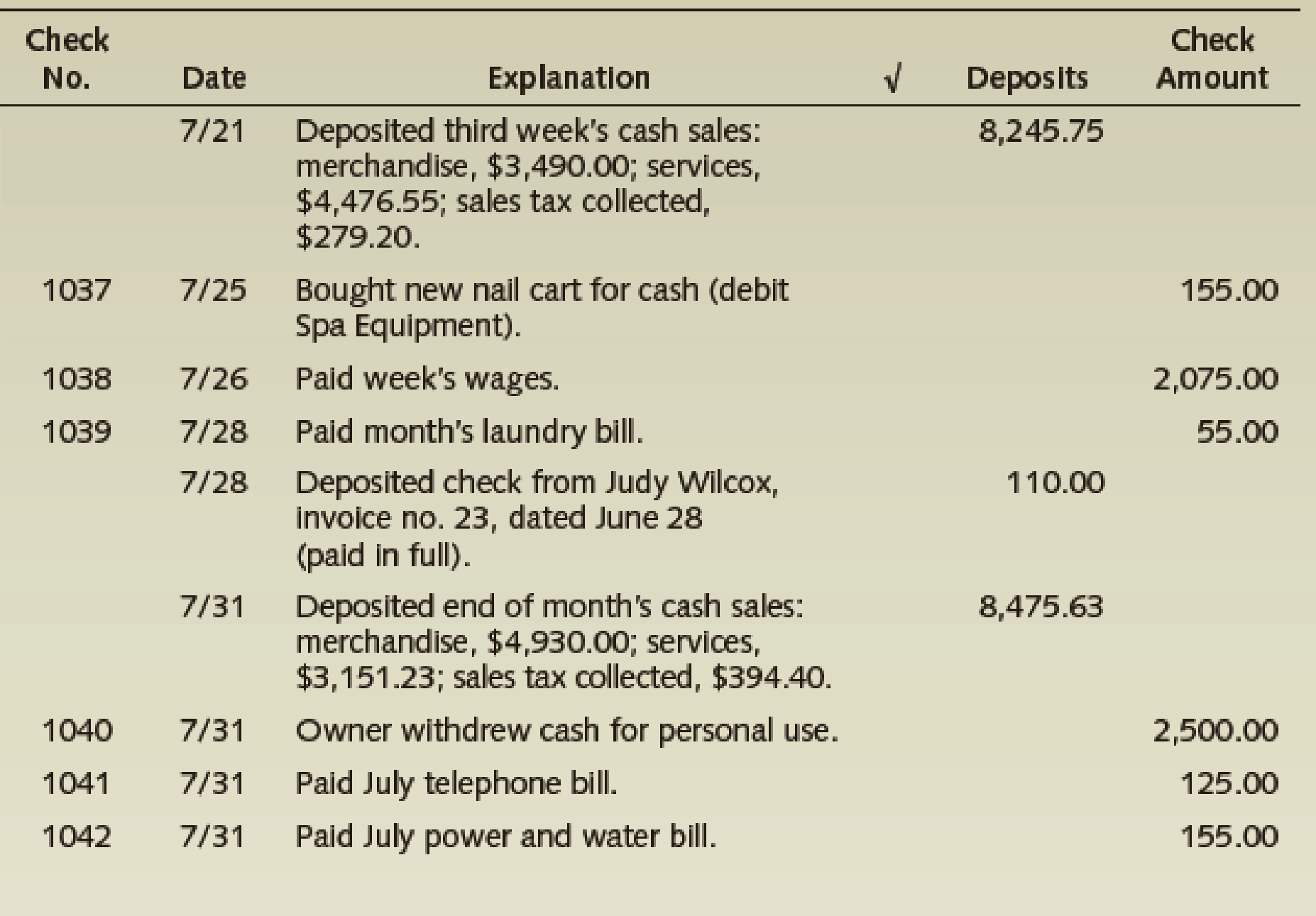

Checkbook Register

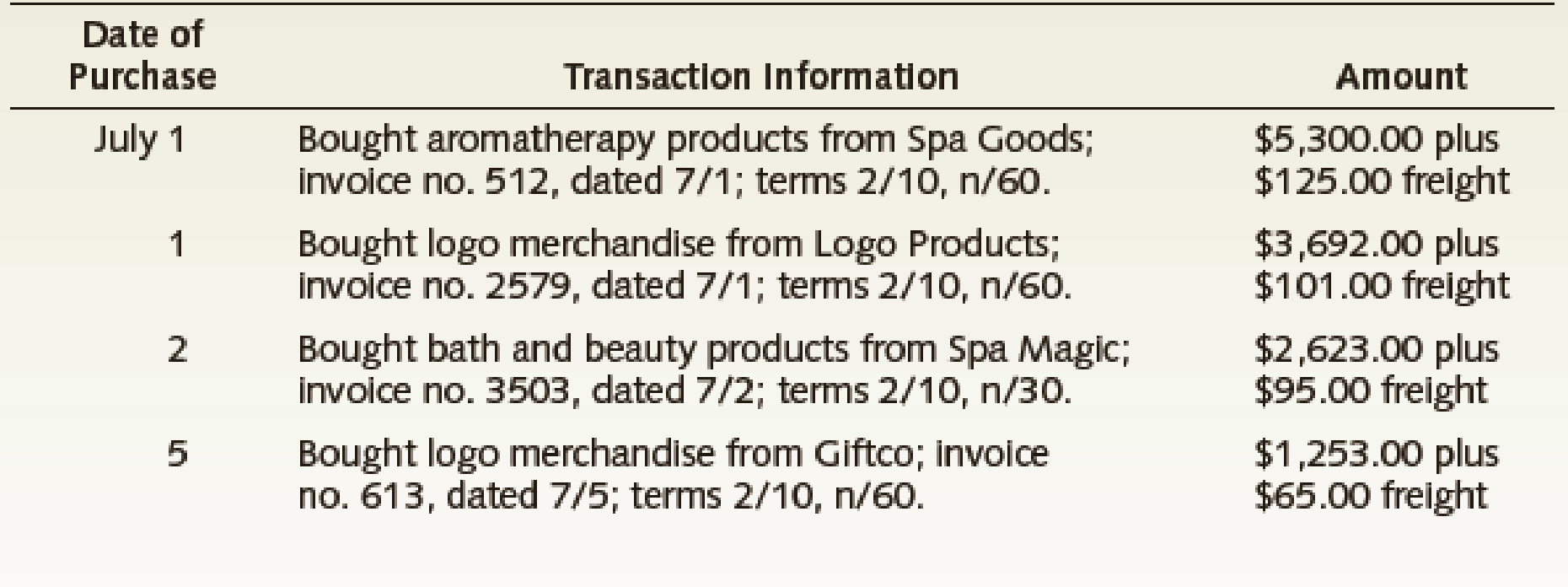

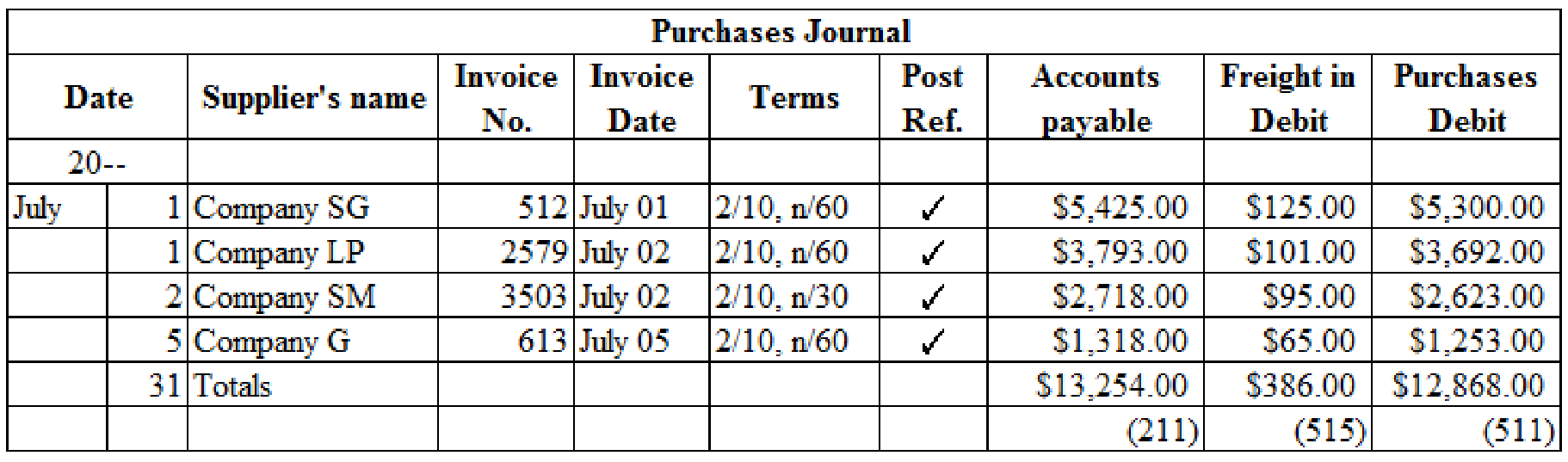

Purchases Invoices for Merchandise Bought on Account During July

All About You Spa will pay all freight costs associated with purchases of merchandise to the supplier. Use the new accounts Purchases 511 and Freight In 515.

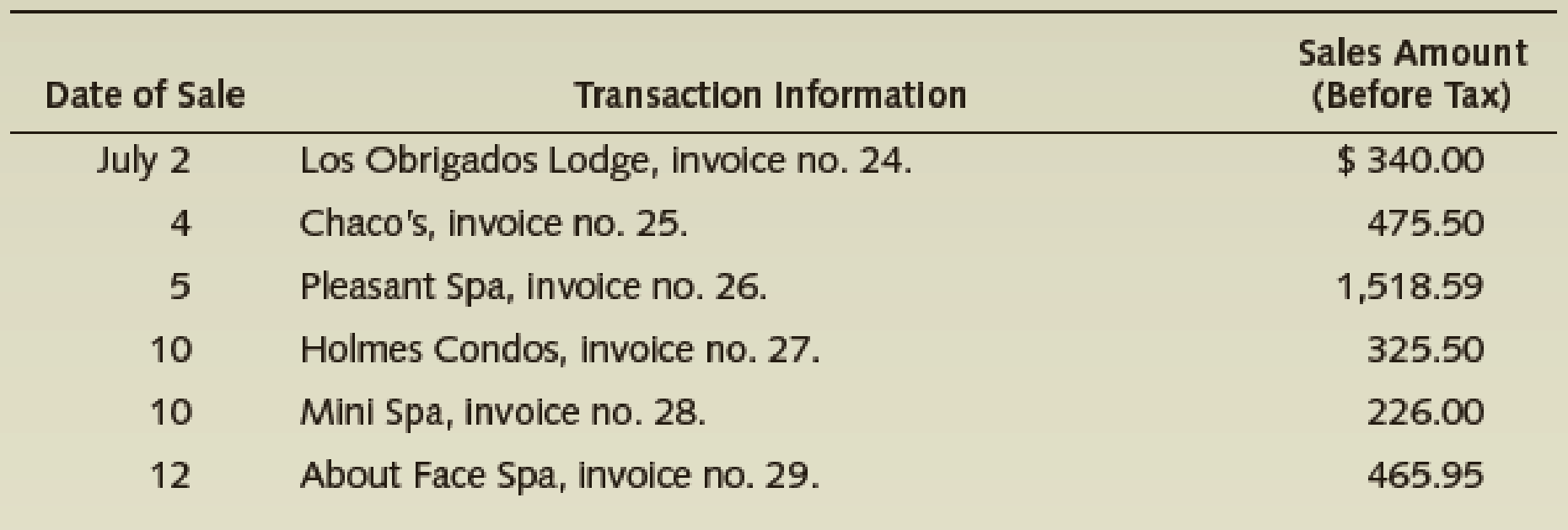

Sales Invoices for Gift Certificates Sold on Account During July

All About You Spa is responsible for collecting and paying the sales tax on merchandise that it sells. The sales tax rate where All About You Spa does business is 8 percent of each sale (for example, $340.00 × 0.08 = $27.20).

Note: All gift certificates were redeemed for merchandise by the end of the month.

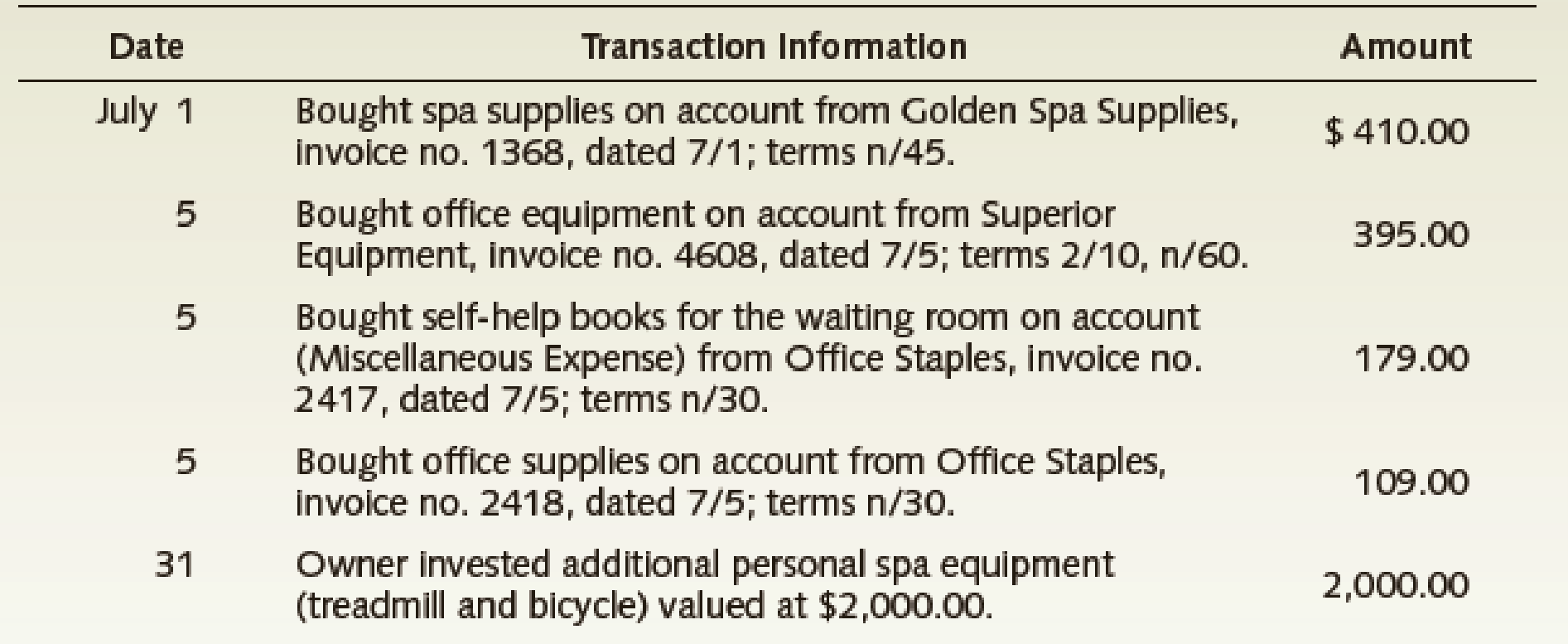

Other July Transactions

There were five other transactions in July. None involved cash.

Required

- 1. Journalize the transactions for July (in date order). Ask your instructor whether you should use the special journals or the general journal for this problem.

- If you are preparing the journal entries using Working Papers, enter your transactions beginning on page 6.

- 2.

Post the entries to the accounts receivable, accounts payable, and general ledgers.- Ignore this step if you are using CLGL.

- 3. Prepare a

trial balance as of July 31, 20--. - 4. Prepare a schedule of accounts receivable as of July 31, 20--.

- 5. Prepare a schedule of accounts payable as of July 31, 20--.

1.

Journalize the transactions for the month of July.

Explanation of Solution

Journal entry: Journal entry is a set of economic events which can be measured in monetary terms. These are recorded chronologically and systematically.

Rules of Debit and Credit: Following rules are followed for debiting and crediting different accounts while they occur in business transactions:

- Debit, all increase in assets, expenses and dividends, all decrease in liabilities, revenues and stockholders’ equities.

- Credit, all increase in liabilities, revenues, and stockholders’ equities, all decrease in assets, expenses.

Journalize the transactions for the month of July:

| Date | Account title and explanation | Post Ref. | Amount | ||

| Debit | Credit | ||||

| 20-- | |||||

| July | 1 | Cash | 111 | $20,000 | |

| Person AV's Capital | 311 | $20,000 | |||

| 1 | Spa Supplies | 115 | $410 | ||

| Accounts Payable - Company GSS | 211/✓ | $410 | |||

| 1 | Purchases | 511 | $5,300 | ||

| Freight In | 515 | $125 | |||

| Accounts Payable - Company SG | 211/✓ | $5,425 | |||

| 1 | Purchases | 511 | $3,692 | ||

| Freight In | 515 | $101 | |||

| Accounts Payable – Company LP | 211/✓ | $3,793 | |||

| 2 | Purchases | 511 | $2,623 | ||

| Freight In | 515 | $95 | |||

| Accounts Payable - Company SM | 211/✓ | $2,718 | |||

| 2 | Accounts receivable - Company LO | 113/✓ | $367 | ||

| Merchandise Sales | 412 | $340 | |||

| Sales Tax Payable | 215 | $27 | |||

| 3 | Spa Equipment | 128 | $8,150 | ||

| Accounts Payable -Incorporation SE | 211/✓ | $6,150 | |||

| Cash | 111 | $2,000 | |||

| 3 | Rent Expense | 612 | $1,500 | ||

| Cash | 111 | $1,500 | |||

| 4 | Accounts Receivable- Company C | 113/✓ | $514 | ||

| Merchandise Sales | 412 | $476 | |||

| Sales Tax Payable | 215 | $38 | |||

| 5 | Accounts Payable - Company GSS | 211/✓ | $685 | ||

| Cash | 111 | $685 | |||

| 5 | Accounts Payable - Company OS | 211/✓ | $125 | ||

| Cash | 111 | $125 | |||

| 5 | Promotional Expense | 630 | $125 | ||

| Cash | 111 | $125 | |||

| 5 | Accounts Payable - Incorporation A | 211/✓ | $415 | ||

| Cash | 111 | $415 | |||

| 5 | Wages Payable | 212 | $415 | ||

| Wages Expense | 611 | $1,660 | |||

| Cash | 111 | $2,075 | |||

| 5 | Office Equipment | 124 | $395 | ||

| Accounts Payable - Company SE | 211/✓ | $395 | |||

| 5 | Promotion Expense | 630 | $179 | ||

| Accounts Payable - Company OS | 211/✓ | $179 | |||

| 5 | Office Supplies | 114 | $109 | ||

| Accounts Payable -Company OS | 211/✓ | $109 | |||

| 5 | Purchases | 511 | $1,253 | ||

| Freight In | 515 | $65 | |||

| Accounts Payable - Company G | 211/✓ | $1,318 | |||

| 5 | Accounts receivable - Company PS | 113/✓ | $1,640 | ||

| Merchandise Sales | 412 | $1,519 | |||

| Sales Tax Payable | 215 | $121 | |||

| 7 | Cash | 111 | $4,867 | ||

| Merchandise Sales | 412 | $1,510 | |||

| Income from Services | 411 | $3,225 | |||

| Sales Tax Payable | 215 | $132 | |||

| 7 | Cash | 111 | $150 | ||

| Accounts Receivable - Company JA | 113/✓ | $150 | |||

| 10 | Accounts Receivable - Company HC | 113/✓ | $352 | ||

| Merchandise Sales | 412 | $326 | |||

| Sales Tax Payable | 215 | $26 | |||

| 10 | Accounts Receivable - Company MS | 113/✓ | $244 | ||

| Merchandise Sales | 412 | $226 | |||

| Sales Tax Payable | 215 | $18 | |||

| 12 | Wages Expense | 611 | $2,075 | ||

| Cash | 111 | $2,075 | |||

| 12 | Accounts Receivable - Company AFS | 113/✓ | $503 | ||

| Merchandise Sales | 412 | $466 | |||

| Sales Tax Payable | 215 | $37 | |||

| 14 | Cash | 111 | $200 | ||

| Accounts Receivable - Company JM | 113/✓ | $200 | |||

| 14 | Cash | 111 | $4,157 | ||

| Merchandise Sales | 412 | $1,525 | |||

| Income from Services | 411 | $2,510 | |||

| Sales Tax Payable | 215 | $122 | |||

| 18 | Accounts Payable - Company SE | 211/✓ | $520 | ||

| Cash | 111 | $520 | |||

| 19 | Wages Expense | 611 | $2,075 | ||

| Cash | 111 | $2,075 | |||

| 21 | Cash | 111 | $185 | ||

| Accounts Receivable - Company TL | 113/✓ | $185 | |||

| 21 | Cash | 111 | $8,246 | ||

| Merchandise Sales | 412 | $3,490 | |||

| Income from Services | 411 | $4,477 | |||

| Sales Tax Payable | 215 | $279 | |||

| 25 | Spa Equipment | 128 | $155 | ||

| Cash | 111 | $155 | |||

| 26 | Wages Expense | 611 | $2,075 | ||

| Cash | 111 | $2,075 | |||

| 28 | Laundry Expense | 615 | $55 | ||

| Cash | 111 | $55 | |||

| 28 | Cash | 111 | $110 | ||

| Accounts Receivable - Company JW | 113/✓ | $110 | |||

| 31 | Cash | 111 | $8,476 | ||

| Merchandise Sales | 412 | $4,930 | |||

| Income from Services | 411 | $3,151 | |||

| Sales Tax Payable | 215 | $394 | |||

| 31 | Person AV's Drawing | 312 | $2,500 | ||

| Cash | 111 | $2,500 | |||

| 31 | Utilities Expense | 617 | $125 | ||

| Cash | 111 | $125 | |||

| 31 | Utilities Expense | 617 | $155 | ||

| Cash | 111 | $155 | |||

| 31 | Spa Equipment | 128 | $2,000 | ||

| Person AV's Capital | 311 | $2,000 | |||

Table (1)

2.

Post the entries to the accounts receivable, accounts payable and general ledger.

Explanation of Solution

Post the entries to the accounts receivable, accounts payable and general ledger:

General Ledger:

| Sales journal | |||||||

| Date | Invoice No. | Customer's name | Post Ref. | Accounts Receivable debit | Sales tax payable credit | Merchandise sales credit | |

| 20-- | |||||||

| July | 2 | 24 | Company LO | 367.20 | 27.20 | 340.00 | |

| 4 | 25 | Company C | 513.54 | 38.04 | 475.50 | ||

| 5 | 26 | Company PS | 1,640.08 | 121.49 | 1,518.59 | ||

| 10 | 27 | Company HC | 351.54 | 26.04 | 325.50 | ||

| 10 | 28 | Company MS | 244.08 | 18.08 | 226.00 | ||

| 12 | 29 | Company AFS | 503.23 | 37.28 | 465.95 | ||

| 31 | Totals | 3,619.67 | 268.13 | 3,351.54 | |||

| (113) | (215) | (412) | |||||

Table (2)

Table (3)

| Account: Cash | Account No. 111 | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | ||

| Debit | Credit | ||||||

| 20-- | |||||||

| July | 1 | Balance | ✓ | $24,597.00 | |||

| 1 | J6 | $20,000.00 | $44,597.00 | ||||

| 3 | J6 | $2,000.00 | $42,597.00 | ||||

| 3 | J6 | $1,500.00 | $41,097.00 | ||||

| 5 | J7 | $685.00 | $40,412.00 | ||||

| 5 | J7 | $125.00 | $40,287.00 | ||||

| 5 | J7 | $125.00 | $40,162.00 | ||||

| 5 | J7 | $415.00 | $39,747.00 | ||||

| 5 | J7 | $2,075.00 | $37,672.00 | ||||

| 7 | J8 | $4,867.13 | $42,539.13 | ||||

| 7 | J8 | $150.00 | $42,689.13 | ||||

| 12 | J8 | $2,075.00 | $40,614.13 | ||||

| 14 | J8 | $200.00 | $40,814.13 | ||||

| 14 | J9 | $4,157.00 | $44,971.13 | ||||

| 18 | J9 | $520.00 | $44,451.13 | ||||

| 19 | J9 | $2,075.00 | $42,376.13 | ||||

| 21 | J9 | $185.00 | $42,561.13 | ||||

| 21 | J9 | $8,245.75 | $50,806.88 | ||||

| 25 | J9 | $155.00 | $50,651.88 | ||||

| 26 | J9 | $2,075.00 | $48,576.88 | ||||

| 28 | J9 | $55.00 | $48,521.88 | ||||

| 28 | J9 | $110.00 | $48,631.88 | ||||

| 31 | J9 | $8,475.63 | $57,107.51 | ||||

| 31 | J10 | $2,500.00 | $54,607.51 | ||||

| 31 | J10 | $125.00 | $54,482.51 | ||||

| 31 | J10 | $155.00 | $54,327.51 | ||||

Table (4)

| Account: Accounts receivable | Account No. 113 | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | ||

| Debit | Credit | ||||||

| 20-- | |||||||

| July | 1 | Balance | ✓ | $1,273.00 | |||

| 2 | J6 | $367.20 | $1,640.20 | ||||

| 4 | J7 | $513.54 | $2,153.74 | ||||

| 5 | J8 | $1,639.39 | $3,793.82 | ||||

| 7 | J8 | $150.00 | $3,643.82 | ||||

| 10 | J8 | $351.54 | $3,995.36 | ||||

| 10 | J8 | $244.08 | $4,239.44 | ||||

| 12 | J8 | $503.23 | $4,742.67 | ||||

| 14 | J8 | $200.00 | $4,542.67 | ||||

| 21 | J9 | $185.00 | $4,357.67 | ||||

| 28 | J9 | $110.00 | $4,247.67 | ||||

Table (5)

| Account: Office supplies | Account No. 114 | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | ||

| Debit | Credit | ||||||

| 20-- | |||||||

| July | 1 | Balance | ✓ | $1,273.00 | |||

| 2 | J6 | $367.20 | $1,640.20 | ||||

Table (6)

| Account: Spa supplies | Account No. 115 | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | ||

| Debit | Credit | ||||||

| 20-- | |||||||

| July | 1 | Balance | ✓ | $255.00 | |||

| 5 | J7 | $410.00 | $665.00 | ||||

Table (7)

| Account: Prepaid insurance | Account No. 117 | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | ||

| Debit | Credit | ||||||

| 20-- | |||||||

| July | 1 | Balance | ✓ | $700.00 | |||

Table (8)

| Account: Office equipment | Account No. 124 | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | ||

| Debit | Credit | ||||||

| 20-- | |||||||

| July | 1 | Balance | ✓ | $1,345.00 | |||

| 5 | J7 | $395.00 | $1,740.00 | ||||

Table (9)

| Account: Accumulated Depreciation, Office equipment | Account No. 125 | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | ||

| Debit | Credit | ||||||

| 20-- | |||||||

| July | 1 | Balance | ✓ | $13.25 | |||

Table (10)

| Account: Spa equipment | Account No. 128 | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | ||

| Debit | Credit | ||||||

| 20-- | |||||||

| July | 1 | Balance | ✓ | $9,125.00 | |||

| 3 | J6 | $8,150.00 | $17,275.00 | ||||

| 25 | J9 | $155.00 | $17,430.00 | ||||

| 31 | J10 | $2,000.00 | $19,430.00 | ||||

Table (11)

| Account: Accumulated Depreciation, Spa equipment | Account No. 129 | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | ||

| Debit | Credit | ||||||

| 20-- | |||||||

| July | 1 | Balance | ✓ | $150.00 | |||

Table (12)

| Account: Accounts payable | Account No. 211 | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | ||

| Debit | Credit | ||||||

| 20-- | |||||||

| July | 1 | Balance | ✓ | $2,570.00 | |||

| 1 | J6 | $410.00 | $2,980.00 | ||||

| 1 | J6 | $5,425.00 | $8,405.00 | ||||

| 1 | J6 | $3,793.00 | $12,198.00 | ||||

| 2 | J6 | $2,718.00 | $14,916.00 | ||||

| 3 | J6 | $6,150.00 | $21,066.00 | ||||

| 5 | J7 | $685.00 | $20,381.00 | ||||

| 5 | J7 | $125.00 | $20,236.00 | ||||

| 5 | J7 | $415.00 | $19,841.00 | ||||

| 5 | J7 | $395.00 | $20,236.00 | ||||

| 5 | J7 | $179.00 | $20,415.00 | ||||

| 5 | J7 | $109.00 | $20,524.00 | ||||

| 5 | J8 | $1,318.00 | $21,842.00 | ||||

| 18 | J9 | $520.00 | $21,322.00 | ||||

Table (13)

| Account: Wages payable | Account No. 212 | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | ||

| Debit | Credit | ||||||

| 20-- | |||||||

| July | 1 | Balance | ✓ | $415.00 | |||

| 5 | J7 | $415.00 | |||||

Table (14)

| Account: Sales tax payable | Account No. 215 | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | ||

| Debit | Credit | ||||||

| 20-- | |||||||

| July | 2 | J6 | $27.20 | $27.20 | |||

| 4 | J7 | $38.04 | $65.24 | ||||

| 5 | J8 | $121.49 | $186.73 | ||||

| 7 | J8 | $132.13 | $318.86 | ||||

| 10 | J8 | $26.04 | $344.90 | ||||

| 10 | J8 | $18.08 | $362.98 | ||||

| 12 | J8 | $37.28 | $400.26 | ||||

| 14 | J9 | $122.00 | $522.26 | ||||

| 21 | J9 | $279.20 | $801.46 | ||||

| 31 | J9 | $394.40 | $1,195.86 | ||||

Table (15)

| Account: Person AV, Capital | Account No. 311 | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | ||

| Debit | Credit | ||||||

| 20-- | |||||||

| July | 1 | Balance | ✓ | $34,271.75 | |||

| 1 | J6 | $20,000.00 | 54,271.75 | ||||

| 31 | J10 | $2,000.00 | 56,271.75 | ||||

Table (16)

| Account: Person AV, Drawing | Account No. 312 | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | ||

| Debit | Credit | ||||||

| 20-- | |||||||

| July | 31 | J10 | $2,500.00 | $2,500.00 | |||

Table (17)

| Account: Income summary | Account No. 313 | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | ||

| Debit | Credit | ||||||

| 20-- | |||||||

Table (18)

| Account: Income from services | Account No. 411 | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | ||

| Debit | Credit | ||||||

| 20-- | |||||||

| July | 7 | J8 | $3,225.00 | $3,225.00 | |||

| 14 | J9 | $2,510.00 | $5,735.00 | ||||

| 21 | J9 | $4,476.55 | $10,211.55 | ||||

| 31 | J9 | $3,151.23 | $13,362.78 | ||||

Table (19)

| Account: Merchandise sales | Account No. 412 | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | ||

| Debit | Credit | ||||||

| 20-- | |||||||

| July | 2 | J6 | $340.00 | $340.00 | |||

| 4 | J7 | $475.50 | $815.50 | ||||

| 5 | J8 | $1,518.59 | $2,334.09 | ||||

| 7 | J8 | $1,510.00 | $3,844.09 | ||||

| 10 | J8 | $325.50 | $4,169.59 | ||||

| 10 | J8 | $226.00 | $4,395.59 | ||||

| 12 | J8 | $465.95 | $4,861.54 | ||||

| 14 | J9 | $1,525.00 | $6,386.54 | ||||

| 21 | J9 | $3,490.00 | $9,876.54 | ||||

| 31 | J9 | $4,930.00 | $14,806.54 | ||||

Table (20)

| Account: Purchases | Account No. 511 | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | ||

| Debit | Credit | ||||||

| 20-- | |||||||

| July | 1 | J6 | $5,300.00 | $5,300.00 | |||

| 1 | J6 | $3,692.00 | $8,992.00 | ||||

| 2 | J6 | $2,623.00 | $11,615.00 | ||||

| 5 | J8 | $1,253.00 | $12,868.00 | ||||

Table (21)

| Account: Freight In | Account No. 515 | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | ||

| Debit | Credit | ||||||

| 20-- | |||||||

| July | 1 | J6 | $125.00 | $125.00 | |||

| 1 | J6 | $101.00 | $226.00 | ||||

| 2 | J6 | $95.00 | $321.00 | ||||

| 5 | J8 | $65.00 | $386.00 | ||||

Table (22)

| Account: Wages expense | Account No. 611 | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | ||

| Debit | Credit | ||||||

| 20-- | |||||||

| July | 5 | J7 | $1,660.00 | $1,660.00 | |||

| 12 | J8 | $2,075.00 | $2,075.00 | ||||

| 19 | J9 | $2,075.00 | $5,810.00 | ||||

| 26 | J9 | $2,075.00 | $7,885.00 | ||||

Table (23)

| Account: Rent expense | Account No. 612 | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | ||

| Debit | Credit | ||||||

| 20-- | |||||||

| July | 3 | J6 | $1,500.00 | $1,500.00 | |||

Table (24)

| Account: Office supplies expense | Account No. 613 | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | ||

| Debit | Credit | ||||||

| 20-- | |||||||

Table (25)

| Account: Spa supplies expense | Account No. 614 | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | ||

| Debit | Credit | ||||||

| 20-- | |||||||

Table (26)

| Account: Laundry expense | Account No. 615 | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | ||

| Debit | Credit | ||||||

| 20-- | |||||||

| July | 28 | J9 | $55.00 | $55.00 | |||

Table (27)

| Account: Advertising expense | Account No. 616 | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | ||

| Debit | Credit | ||||||

| 20-- | |||||||

Table (28)

| Account: Utilities expense | Account No. 617 | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | ||

| Debit | Credit | ||||||

| 20-- | |||||||

| July | 31 | J10 | $125.00 | $125.00 | |||

| 31 | J10 | $155.00 | $280.00 | ||||

Table (29)

| Account: Insurance expense | Account No. 618 | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | ||

| Debit | Credit | ||||||

| 20-- | |||||||

Table (30)

| Account: Depreciation expense, Office equipment | Account No. 619 | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | ||

| Debit | Credit | ||||||

| 20-- | |||||||

Table (31)

| Account: Depreciation expense, Spa equipment | Account No. 620 | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | ||

| Debit | Credit | ||||||

| 20-- | |||||||

Table (32)

| Account: Promotional expense | Account No. 630 | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | ||

| Debit | Credit | ||||||

| 20-- | |||||||

| July | 5 | J7 | $125.00 | $125.00 | |||

| $179.00 | $179.00 | ||||||

Table (33)

Accounts receivable ledger:

| Accounts receivable ledger | ||||||

| Name : Company AFS | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | |

| 20-- | ||||||

| July | 12 | J8 | $503.23 | $503.23 | ||

Table (34)

| Accounts receivable ledger | ||||||

| Name : Company JA | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | |

| 20-- | ||||||

| July | 1 | ✓ | $350.00 | |||

| 7 | J8 | $150.00 | $200.00 | |||

Table (35)

| Accounts receivable ledger | ||||||

| Name : Company C | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | |

| 20-- | ||||||

| July | 4 | J7 | $513.54 | $513.54 | ||

Table (36)

| Accounts receivable ledger | ||||||

| Name : Company HC | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | |

| 20-- | ||||||

| July | 10 | J8 | $351.54 | $351.54 | ||

Table (37)

| Accounts receivable ledger | ||||||

| Name : Company TL | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | |

| 20-- | ||||||

| July | 1 | Balance | ✓ | $345.00 | ||

| 21 | J9 | $185.00 | $160.00 | |||

Table (38)

| Accounts receivable ledger | ||||||

| Name : Company LO | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | |

| 20-- | ||||||

| July | 2 | J6 | $367.20 | $367.20 | ||

Table (39)

| Accounts receivable ledger | ||||||

| Name : Company MS | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | |

| 20-- | ||||||

| July | 10 | J8 | $244.08 | $244.08 | ||

Table (40)

| Accounts receivable ledger | ||||||

| Name : Company JM | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | |

| 20-- | ||||||

| July | 1 | ✓ | $468.00 | |||

| 14 | J8 | $200.00 | $268.00 | |||

Table (41)

| Accounts receivable ledger | ||||||

| Name : Company PS | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | |

| 20-- | ||||||

| July | 5 | J8 | $1,640.08 | $1,640.08 | ||

Table (42)

| Accounts receivable ledger | ||||||

| Name : Company JW | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | |

| 20-- | ||||||

| July | 1 | Balance | ✓ | $110.00 | ||

| 28 | J8 | $110.00 | $110.00 | |||

Table (43)

Accounts payable ledger:

| Accounts payable ledger | ||||||

| Name : Incorporation A | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | |

| 20-- | ||||||

| July | 1 | Balance | ✓ | $415.00 | ||

| August | 5 | $415.00 | ||||

Table (44)

| Accounts payable ledger | ||||||

| Name : Company G | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | |

| 20-- | ||||||

| July | 5 | J8 | $1,318.00 | $1,318.00 | ||

Table (45)

| Accounts payable ledger | ||||||

| Name : Company GSS | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | |

| 20-- | ||||||

| July | 1 | Balance | ✓ | $685.00 | ||

| 1 | J6 | $410.00 | $1,095.00 | |||

| 5 | J7 | $685.00 | $410.00 | |||

Table (46)

| Accounts payable ledger | ||||||

| Name : Company LP | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | |

| 20-- | ||||||

| July | 1 | Balance | J6 | $3,793.00 | $3,793.00 | |

Table (47)

| Accounts payable ledger | ||||||

| Name : Company OS | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | |

| 20-- | ||||||

| July | 1 | Balance | ✓ | $125.00 | ||

| 5 | J7 | $125.00 | ||||

| 5 | J7 | $179.00 | $179.00 | |||

| 5 | J7 | $109.00 | $288.00 | |||

Table (48)

| Accounts payable ledger | ||||||

| Name : Incorporation SE | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | |

| 20-- | ||||||

| July | 1 | Balance | ✓ | |||

| 3 | J6 | $6,150.00 | $6,150.00 | |||

Table (49)

| Accounts payable ledger | ||||||

| Name : Company SG | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | |

| 20-- | ||||||

| July | 1 | J6 | $5,425.00 | $5,425.00 | ||

Table (50)

| Accounts payable ledger | ||||||

| Name : Company SM | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | |

| 20-- | ||||||

| July | 2 | J6 | $2,718.00 | $2,718.00 | ||

Table (51)

| Accounts payable ledger | ||||||

| Name : Company SE | ||||||

| Date | Item | Post Ref. | Debit | Credit | Balance | |

| 20-- | ||||||

| July | 1 | Balance | ✓ | $1,345.00 | ||

| 5 | J7 | 395 | $1,740.00 | |||

| 18 | J9 | 520 | $1,220.00 | |||

Table (52)

3.

Prepare trial balance as of July 31.

Explanation of Solution

Trial balance: Trial balance is a summary of all the asset, liability, and equity accounts and their balances.

Prepare the trial balance.

| Company AAY | ||

| Trial balance | ||

| As on July 31, 20-- | ||

| Account name | Debit | Credit |

| Cash | $54,327.51 | |

| Accounts Receivable | $4,247.67 | |

| Office Supplies | $234.00 | |

| Spa Supplies | $665.00 | |

| Prepaid Insurance | $700.00 | |

| Office Equipment | $1,740.00 | |

| Accumulated Depreciation, Office Equipment | $13.25 | |

| Spa Equipment | $19,430.00 | |

| Accumulated Depreciation, Spa Equipment | $150.00 | |

| Accounts Payable | $21,322.00 | |

| Sales Tax Payable | $1,195.86 | |

| Person AV, Capital | $56,271.75 | |

| Person AV, Drawing | $2,500.00 | |

| Income from Services | $13,362.78 | |

| Merchandise Sales | $14,806.54 | |

| Purchases | $12,868.00 | |

| Freight In | $386.00 | |

| Wages Expense | $7,885.00 | |

| Rent Expense | $1,500.00 | |

| Laundry Expense | $55.00 | |

| Utilities Expense | $280.00 | |

| Miscellaneous Expense | $304.00 | |

| Total | $107,122.18 | $107,122.18 |

Table (53)

Thus, the total of trial balance of Company AAY is $107,122.18.

4.

Prepare a schedule of accounts receivable.

Explanation of Solution

Schedule of accounts receivable: A schedule of accounts receivable is a subsidiary ledger that list out the accounts of credit customers individually in alphabetical or numeric order with their respective balances.

Prepare a schedule of accounts receivable:

| Company AAY | |

| Schedule of Accounts receivable | |

| July 31, 20-- | |

| Particulars | Amount |

| Company AFS | $503.23 |

| Company JA | $200.00 |

| Company C | $513.54 |

| Company HC | $351.54 |

| Incorporation TL | $160.00 |

| Company LO | $367.20 |

| Company MS | $244.08 |

| Company JM | $268.00 |

| Company PS | 1,640.08 |

| Total Accounts receivable | $4,247.67 |

Table (54)

5.

Prepare a schedule of Accounts payable.

Explanation of Solution

Schedule of accounts payable: A schedule of accounts payable lists is a subsidiary ledger that list out the accounts of creditors (vendors/suppliers) individually in alphabetical or numeric order with their respective balances.

Prepare a schedule of Accounts payable:

| Company AAY | |

| Schedule of Accounts payable | |

| July 31, 20-- | |

| Particulars | Amount |

| Company G | $1,318.00 |

| Company GSS | $410.00 |

| Company LP | $3,793.00 |

| Company OS | $288.00 |

| Incorporation SE | $6,150.00 |

| Company SG | $5,425.00 |

| Company SM | $2,718.00 |

| Company SE | $1,220.00 |

| Total Accounts payable | $21,322.00 |

Table (55)

Want to see more full solutions like this?

Chapter 9 Solutions

EBK COLLEGE ACCOUNTING: A CAREER APPROA

Additional Business Textbook Solutions

Managerial Accounting (4th Edition)

Financial Accounting

Managerial Accounting: Tools for Business Decision Making

Financial Accounting: Tools for Business Decision Making, 8th Edition

FINANCIAL ACCT.FUND.(LOOSELEAF)

Fundamentals Of Financial Accounting

- Identifying and Recording Customer Option for Additional Merchandise A large clothing retailer chain, Koll's, offers a sales incentive program where customers receive direct credit toward future purchases based upon the dollar amount of purchases today. For every $50 spent today, the customer will earn a $6 credit to be used at Koll's in two weeks. The credit expires 5 days after it becomes active. Not all customers will redeem the credit in the 5-day window of time. Based upon historical trends, Koll's estimates that 35% of the credits will be redeemed. a. Determine how many performance obligations are included in a sales transaction during the sales incentive program. Two performance obligations ◆ b. Assuming that Koll's sold $400,000 of merchandise (cost of $160,000) during the first day of the sales incentive period and 8,000, $6 credits were given, record the journal entry(ies) to record sales revenue. Assume all sales were cash sales. Note: Carry all decimals in calculations;…arrow_forwardABC is an online-to-offline platform that sells e-commerce products to offline customers through a network of agents. ABC gives a commission to agents for each sale made. ABC has 4 main product categories: electronics, fashion, supermarket, and others. Please refer to the exhibits for data sets pertaining to the questions below. Today is May 16th. 1. What is the average growth in average sales per agent per month from March to May target? Answer: %2. Which one is the category with the highest and lowest average month-on- month sales growth from March to May target? Answer: Highest: Lowest:3. Today is May We have got the interim result of the sales figures in the first half of May. Typically, the first half of the month constitutes of 40% of sales. Using this assumption, will we reach our May target? What % over the target will we over/under-deliver? Answer: under/over-deliver by % of target4. Using that assumption, which category (or categories) will not reach the targeted sales…arrow_forwardCurrent Attempt in Progress Your answer is partially correct. Splish Brothers Ltd. held a spring promotion in April that enabled new customers to purchase a package of four lawn treatments treatments for $200. Customers received lawn treatments in May, June, July, and August. Splish Brothers normally charges $50 per treatment. Splish Brothers sold 120 of the promotional packages in April. Using the five-step model, determine the amount of revenue that Splish Brothers would recognize in: a. April and b. May. a. Revenue for the month of April b. Revenue for the month of May LA $ LA 6000 6000arrow_forward

- Customer Latitude and Pricing Maria Lorenzi owns an ice cream stand that she operates during the summer months in West Yellowstone, Montana. She is unsure how to price her ice cream cones and has experimented with two prices in successive weeks during the busy August season. The number of people who entered the store was roughly the same each week. During the first week, she priced the cones at $3.50 and 1,800 cones were sold. During the second week, she priced the cones at $4.00 and 1,400 cones were sold. The variable cost of a cone is $0.80 and consists solely of the costs of the ice cream and the cone itself. The fixed expenses of the ice cream stand are $2,675 per week. Required: 1. What profit did Maria earn during the first week when her price was $3.50? 2. At the start of the second week, Maria increased her selling price by what percentage? What percentage did unit sales decrease? (Round your answers to one-tenth of a percent.) 3. What profit did Maria earn during the second…arrow_forwardABC is an online-to-offline platform that sells e-commerce products to offline customers through a network of agents. ABC gives a commission to agents for each sale made. ABC has 4 main product categories: electronics, fashion, supermarket, and others. Please refer to the exhibits for data sets pertaining to the questions below. Today is May 16th. What is the average growth in average sales per agent per month from March to May target? Answer:..... % Which one is the category with the highest and lowest average month-on-month sales growth from March to May target? Answer: Highest : .......... Lowest:............. Today is 16th May We have got the interim result of the sales figures in the first half of May. Typically, the first half of the month constitutes of 40% of sales. Using this assumption, will we reach our May target? What % over the target will we over/under-deliver? Answer: under/over-deliver by ......... % of target Using that assumption, which…arrow_forwardCan you please show all of your work and show where you are getting the numbers from? Thank you. Barbara's Boards sells a snowboard, Xpert, that is popular with snowboard enthusiasts. Information relating to Barbara's purchases of Xpert snowboards during September is shown below. During the same month, 130 Xpert snowboards were sold. Date Explanation Units Unit Cost Total Cost Sept. 1 Inventory 30 $90 $2,700 Sept. 12 Purchases 50 96 4,800 Sept. 19 Purchases 15 100 1,500 Sept. 26 Purchases 50 104 5,200 Totals 145 $14,200 Additional data regarding Barbara's sales of Xpert snowboards are provided below. Assume that Barbara's uses a perpetual inventory system. Date Units Unit Price Total Revenue Sept. 5 Sale 20 $185 $3,700 Sept. 16 Sale 50 185 9,250 Sept. 29 Sale 60 208 12,480 Totals 130 $25,430 Calculate moving average cost at Sept 1, 5, 12, 16, 19, 26 & 29. (Round answers 2 decimal places, e.g. 1.25.) September 1 %24 90 September 5 %24 September 12 %24 93.75 September 16 %24 September 19…arrow_forward

- Heartstrings Gift Shoppe sells an assortment of gifts for any occasion. During October, Heartstrings started a Gift-of-the-Month program. Under the terms of this program, beginning in the month of the sale, Heartstrings would select and deliver a random gift each month, over the next 12 months, to the person the customer selects as a recipient. During October, Heartstrings sold 28 of these packages for a total of $11,496 in cash.arrow_forwardBefore you begin this assignment review the Tying It All Together feature in the chapter. Best Buy Co., Inc. is a leading provider of technology products. Customers can shop at more than 1,700 stores or online. The company is also known for its Geek Squad for technology services. Suppose Best Buy is considering a particular HDTV for a major sales item for Black Friday, the day after Thanksgiving, known as one of the busiest shopping days of the year. Assume the HDTV has a regular sales price of $900, a cost of $500, and a Black Friday proposed discounted sales price of $650. Best Buy’s 2015 Annual Report states that failure to manage costs could have a material adverse effect on its profitability and that certain elements in its cost structure are largely fixed in nature. Best Buy, like most companies, wishes to maintain price competitiveness while achieving acceptable levels of profitability. (Item 1A. Risk Factors.) Requirements Calculate the gross profit of the HDTV at the regular…arrow_forwardCONTINUING PROBLEM: FRONT ROW ENTERTAINMENT In addition to developing online fan communities, Cam and Anna believe that they could increase Front Row Entertainments revenue by selling live-performance DVDs at the concert. Front Row records the following activity between May and August 2019 for one of its artists: Front Row sells all of its DVDs for $15 each and uses a perpetual inventory system. Required: Discuss the advantages and disadvantages of each method.arrow_forward

- Heartstrings Gift Shoppe sells an assortment of gifts for any occasion. During October, Heartstrings started a Gift-of-the-Month program. Under the terms of this program, beginning in the month of the sale, Heartstrings would select and deliver a random gift each month, over the next 12 months, to the person the customer selects as a recipient. During October, Heartstrings sold 34 of these packages for a total of $12,060 in cash. For the month of October, calculate the amount of revenue that Heartstrings will recognize.arrow_forwardJohanna and her sister are developing a business to make branded reusable stainless steel coffee mugs aimed at the Tourist Market, with logos such as "Love Queenstown" and "Love Taupo". They have developed a web page and are successfully attracting customers from the tourist- located cafes and restaurants. Sales for each quarter of 2019 were as follows. Quarter ending Mar-2019 Jun-2019 Sep-2019 Dec-2019 Number of Mugs 3,600 3,800 4,200 4,800 The sisters have changed their sale strategy for 2020 to a person to person approach and believe this new approach will lead to a 10% sales increase in each quarter in 2020 from the December 2019 base of sales of 4,800 mugs - that is they predict that each quarter in 2020 will have 10% more sales than the previous quarter. The unit sales price will be unchanged from the 2019 price of $8 per mug. They have applied for a bank loan to help finance the expansion of their business. The bank has requested detailed financial data to support their loan…arrow_forwardA. Amber, owner of Amber's Flowers and Gifts, produces gift baskets for various special occasions. Each gift basket includes fruit or assorted small gifts (e.g., a coffee mug, deck of cards, novelty cocoa mixes, scented soap) in a basket that is wrapped in colorful cellophane. Amber has estimated the following unit sales of the standard gift basket for the rest of the year and for January of next year. September October 260 250 November 270 December 350 January 170 Amber likes to have 5% of the next month's sales needs on hand at the end of each month. This requirement was met on August 31. Two materials are needed for each fruit basket: |2 pounds Fruit Small Gifts 4 items The materials inventory policy is to have 5% of the next month's fruit needs on hand and 30% of the next month's production needs of small gifts. (The relatively low inventory amo unt for fruit is designed to prevent spoilage.) Materials inventory on August 31 met this company policy. 1. Prepare a production bud get…arrow_forward

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning

College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning