Concept explainers

Videos

The management of Golding Company has determined that the cost to investigate a variance produced by its

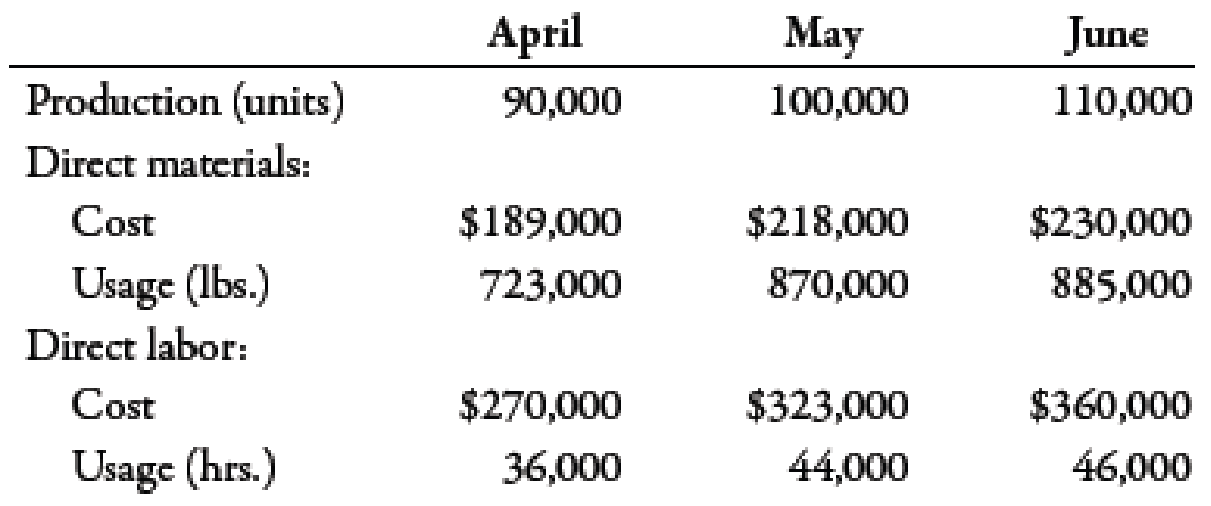

Actual production for the past 3 months follows, with the associated actual usage and costs for materials and labor. There were no beginning or ending raw materials inventories.

Required:

- 1. What upper and lower control limits would you use for materials variances? For labor variances?

- 2. Compute the materials and labor variances for April, May, and June. Identify those that would require investigation by comparing each variance to the amount of the limit computed in Requirement 1. Compute the actual percentage deviation from standard. Round all unit costs to four decimal places. Round variances to the nearest dollar. Round variance rates to three decimal places so that percentages will show to one decimal place.

- 3. CONCEPTUAL CONNECTION Let the horizontal axis be time and the vertical axis be variances measured as a percentage deviation from standard. Draw horizontal lines that identify upper and lower control limits. Plot the labor and material variances for April, May, and June. Prepare a separate graph for each type of variance. Explain how you would use these graphs (called control charts) to assist your

analysis of variances.

1.

Compute the upper and lower limit of materials and labor.

Explanation of Solution

Variance:

The amount obtained when actual cost is deducted from budgeted cost is known as variance. Variance is calculated to find whether the cost is over applied or under applied.

Use the following formula to calculate the value of upper limit of material for April:

Substitute 0.08 for direct material quantity and $180,750 for price standard in the above formula.

Use the following formula to calculate the value of lower limit of material of price standard for April:

Substitute 0.08 for direct material quantity and $180,750 for price standard in the above formula.

Use the following formula to calculate the value of upper limit of material of quantity standard for April:

Substitute 0.08 for direct material quantity and $180,000 for quantity standard in the above formula.

Use the following formula to calculate the value of lower limit of material of quantity standard for April:

Substitute 0.08 for direct material quantity and $180,000 for quantity standard in the above formula.

Use the following formula to calculate the value of upper limit of labor of price standard for April:

Substitute 0.08 for standard quantity and $270,000 for price standard in the above formula.

Use the following formula to calculate the value of lower limit of labor of price standard for April:

Substitute 0.08 for standard quantity and $270,000 for price standard in the above formula.

Use the following formula to calculate the value of upper limit of labor of efficiency standard for April:

Substitute 0.08 for standard quantity and $270,000 for efficiency standard in the above formula.

Use the following formula to calculate the value of lower limit of labor of efficiency standard for April:

Substitute 0.08 for direct material quantity and $270,000 for quantity standard in the above formula.

Use the following formula to calculate the value of upper limit of material for May:

Substitute 0.08 for direct material quantity and $217,500 for price standard in the above formula.

Use the following formula to calculate the value of lower limit of material of price standard for May:

Substitute 0.08 for direct material quantity and $217,500 for price standard in the above formula.

Use the following formula to calculate the value of upper limit of material of quantity standard for May:

Substitute 0.08 for direct material quantity and $200,000 for quantity standard in the above formula.

Use the following formula to calculate the value of lower limit of material of quantity standard for May:

Substitute 0.08 for direct material quantity and $200,000 for quantity standard in the above formula.

Use the following formula to calculate the value of upper limit of labor of price standard for May:

Substitute 0.08 for standard quantity and $330,000 for price standard in the above formula.

Use the following formula to calculate the value of lower limit of labor of price standard for May:

Substitute 0.08 for standard quantity and $330,000 for price standard in the above formula.

Use the following formula to calculate the value of upper limit of labor of efficiency standard for May:

Substitute 0.08 for standard quantity and $300,000 for efficiency standard in the above formula.

Use the following formula to calculate the value of lower limit of labor of efficiency standard for May:

Substitute 0.08 for direct material quantity and $300,000 for quantity standard in the above formula.

Use the following formula to calculate the value of upper limit of material for June:

Substitute 0.08 for direct material quantity and $221,250, for price standard in the above formula.

Use the following formula to calculate the value of lower limit of material of price standard for June:

Substitute 0.08 for direct material quantity and $221,250 for price standard in the above formula.

Use the following formula to calculate the value of upper limit of material of quantity standard for June:

Substitute 0.08 for direct material quantity and $220,000 for quantity standard in the above formula.

Use the following formula to calculate the value of lower limit of material of quantity standard for June:

Substitute 0.08 for direct material quantity and $220,000 for quantity standard in the above formula.

Use the following formula to calculate the value of upper limit of labor of price standard for June:

Substitute 0.08 for standard quantity and $345,000 for price standard in the above formula.

Use the following formula to calculate the value of lower limit of labor of price standard for June:

Substitute 0.08 for standard quantity and $345,000 for price standard in the above formula.

Use the following formula to calculate the value of upper limit of labor of efficiency standard for June:

Substitute 0.08 for standard quantity and $330,000 for efficiency standard in the above formula.

Use the following formula to calculate the value of lower limit of labor of efficiency standard for June:

Substitute 0.08 for direct material quantity and $330,000 for quantity standard in the above formula.

Working Note:

1. Calculation of price standard for material:

2. Calculation of quantity standard for material:

3. Calculation of price standard for labor:

4. Calculation of efficiency standard for labor:

Note: Other calculations are done in a same manner as mentioned above.

2.

Calculate the materials and labor variances for the month of April, May and June.

Explanation of Solution

| Month |

Variances ($) | Limit |

Deviation (%) |

| April | |||

| Material price variance | 8,242(U) | 14,460 | 4.6 |

| Material usage variance | 750(U) | 14,400 | 0.4 |

| Labor rate variance | 0 | 21,600 | 0.0 |

| Labor efficiency variance | 0 | 21,600 | 0.0 |

| May | |||

| Material price variance | 522(U) | 17,400 | 0.2 |

| Material usage variance | 17,500(U) | 16,000 | 8.8 |

| Labor rate variance | 7,000(F) | 26,400 | (2.1) |

| Labor efficiency variance | 30,000(U) | 24,000 | 10.0 |

| June | |||

| Material price variance | 8,762(U) | 17,700 | 4.0 |

| Material usage variance | 1,250(U) | 17,600 | 0.6 |

| Labor rate variance | 15,001(U) | 27,600 | 4.3 |

| Labor efficiency variance | 15,000(U) | 26,400 | 4.5 |

Table (1)

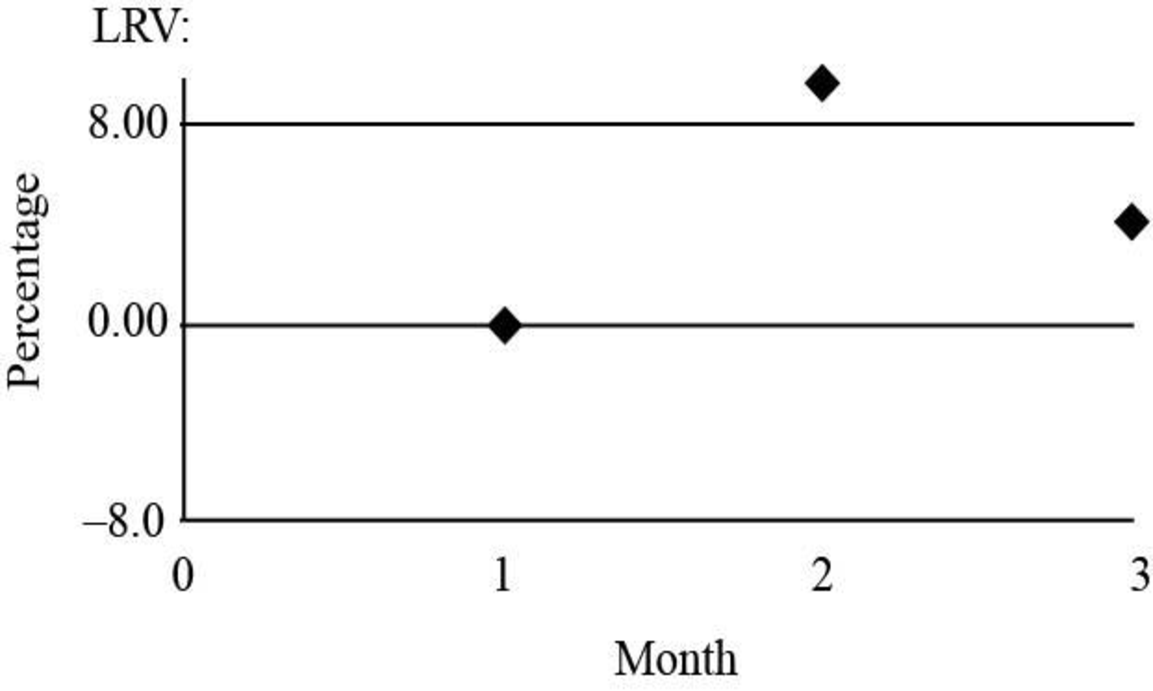

3.

Construct the graph for upper and lower limits for month of April, May and June.

Explanation of Solution

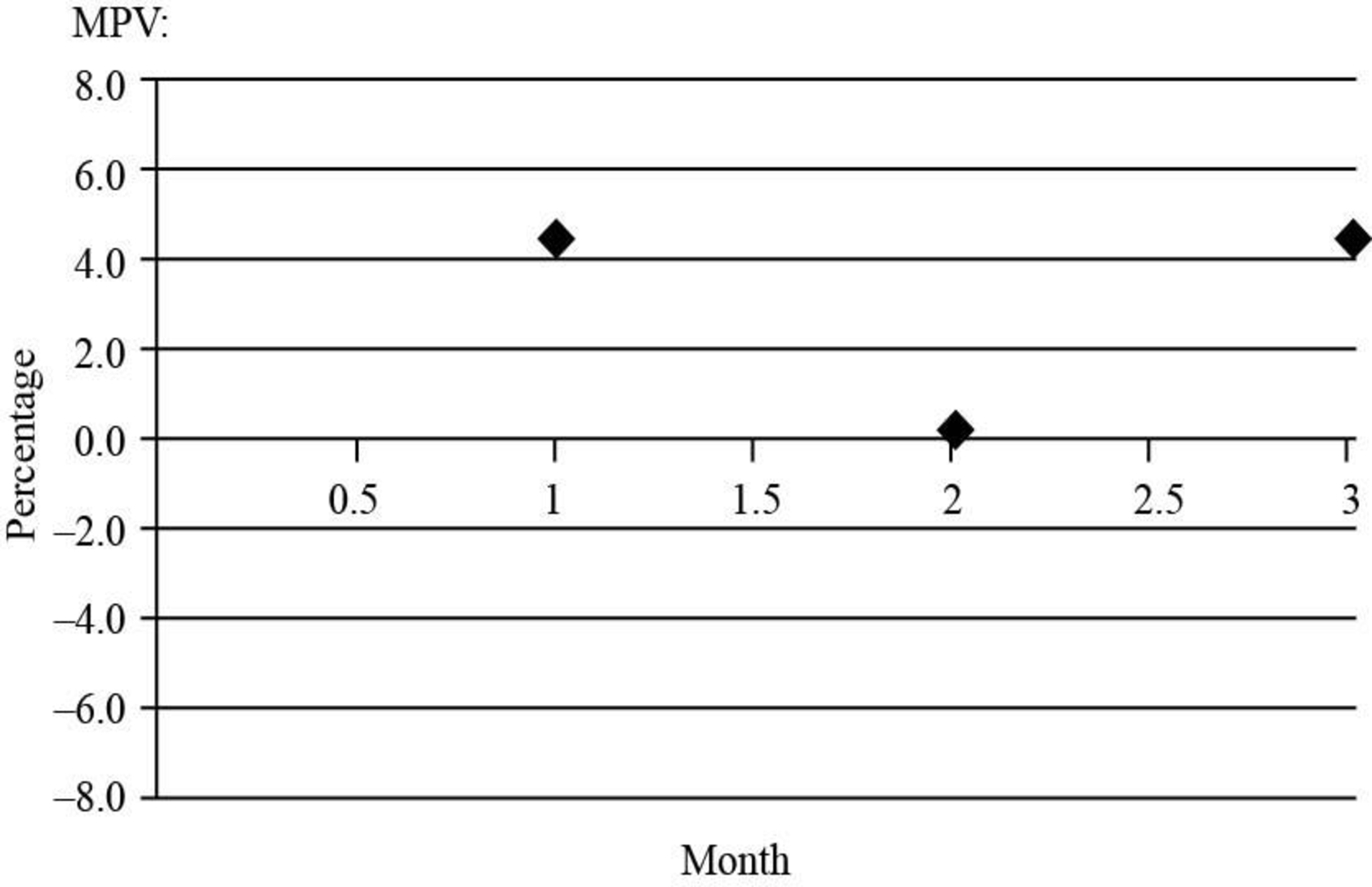

Graph of month of Material price variance:

Fig (1)

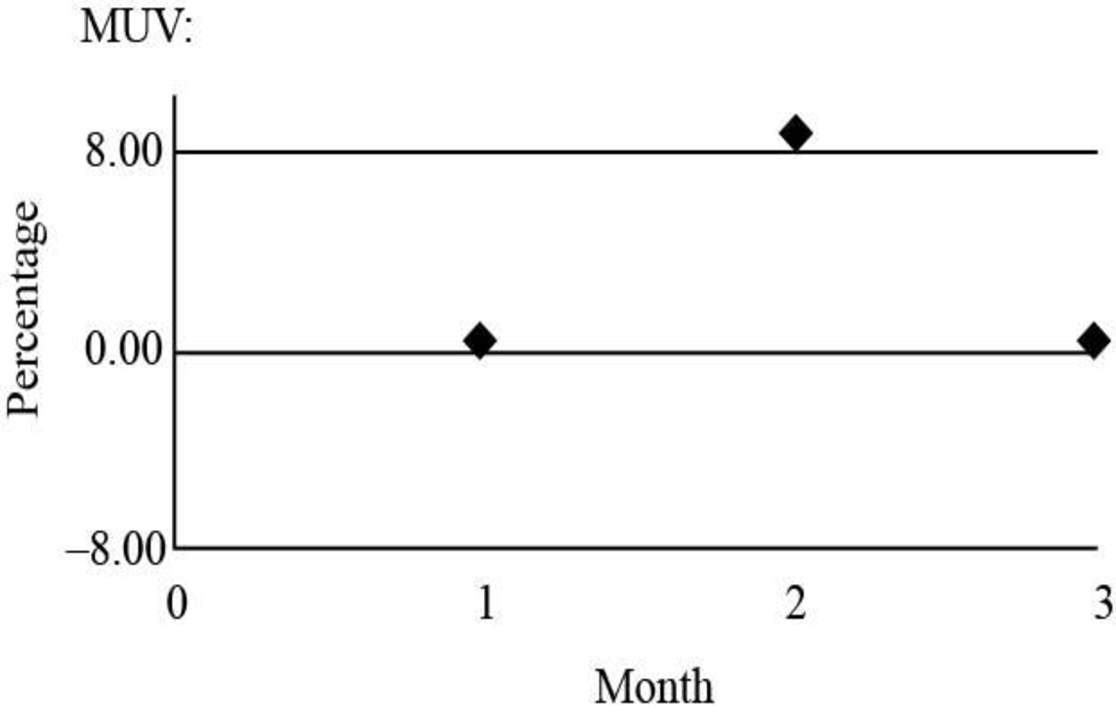

Graph of month of material usage variance:

Fig (2)

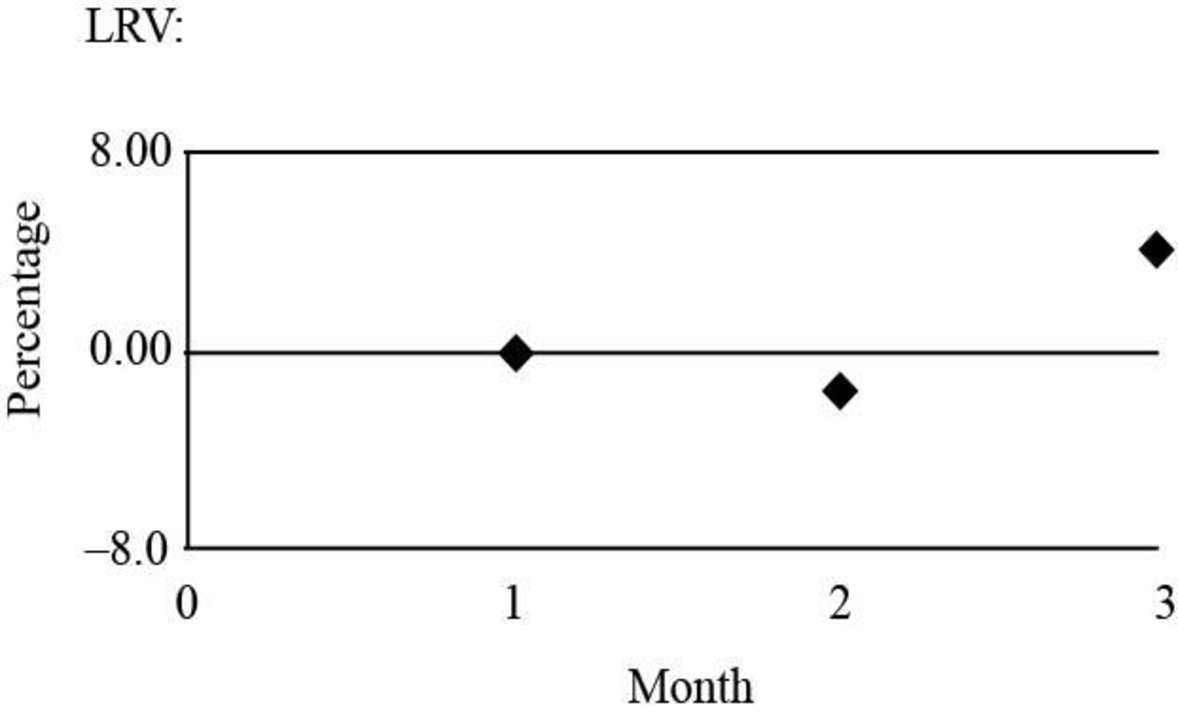

Graph of month of labor rate variance:

Fig (3)

Graph of month of labor efficiency variance

Fig (4)

Want to see more full solutions like this?

Chapter 10 Solutions

Managerial Accounting: The Cornerstone of Business Decision-Making

- In all of the exercises involving variances, use F and U to designate favorable and unfavorable variances, respectively. E8-1 through E8-5 use the following data: The standard operating capacity of Tecate Manufacturing Co. is 1,000 units. A detailed study of the manufacturing data relating to the standard production cost of one product revealed the following: 1. Two pounds of materials are needed to produce one unit. 2. Standard unit cost of materials is 8 per pound. 3. It takes one hour of labor to produce one unit. 4. Standard labor rate is 10 per hour. 5. Standard overhead (all variable) for this volume is 4,000. Each case in E8-1 through E8-5 requires the following: a. Set up a standard cost summary showing the standard unit cost. b. Analyze the variances for materials and labor. c. Make journal entries to record the transfer to Work in Process of: 1. Materials costs 2. Labor costs 3. Overhead costs (When making these entries, include the variances.) d. Prepare the journal entry to record the transfer of costs to the finished goods account. Standard unit cost; variance analysis; journal entries 1,000 units were started and finished. Case 1: All prices and quantities for the cost elements are standard, except for materials cost, which is 8.50 per pound. Case 2: All prices and quantities for the cost elements are standard, except that 1,900 lb of materials were used.arrow_forwardMadison Company uses the following rule to determine whether direct labor efficiency variances ought to be investigated. A direct labor efficiency variance will be investigated anytime the amount exceeds the lesser of 12,000 or 10 percent of the standard labor cost. Reports for the past five weeks provided the following information: Required: 1. Using the rule provided, identify the cases that will be investigated. 2. Suppose that investigation reveals that the cause of an unfavorable direct labor efficiency variance is the use of lower quality direct materials than are usually used. Who is responsible? What corrective action would likely be taken? 3. Suppose that investigation reveals that the cause of a significant favorable direct labor efficiency variance is attributable to a new approach to manufacturing that takes less labor time but causes more direct materials waste. Upon examining the direct materials usage variance, it is discovered to be unfavorable, and it is larger than the favorable direct labor efficiency variance. Who is responsible? What action should be taken? How would your answer change if the unfavorable variance were smaller than the favorable?arrow_forwardKavallia Company set a standard cost for one item at 328,000; allowable deviation is 14,500. Actual costs for the past six months are as follows: Required: 1. Calculate the variance from standard for each month. Which months should be investigated? 2. What if the company uses a two-part rule for investigating variances? The allowable deviation is the lesser of 4 percent of the standard amount or 14,500. Now which months should be investigated?arrow_forward

- Sommers Company uses the following rule to determine whether materials usage variances should be investigated: A materials usage variance will be investigated anytime the amount exceeds the lesser of 12,000 or 10% of the standard cost. Reports for the past 5 weeks provided the following information: Required: 1. Using the rule provided, identify the cases that will be investigated. 2. CONCEPTUAL CONNECTION Suppose investigation reveals that the cause of an unfavorable materials usage variance is the use of lower-quality materials than are normally used. Who is responsible? What corrective action would likely be taken? 3. CONCEPTUAL CONNECTION Suppose investigation reveals that the cause of a significant unfavorable materials usage variance is attributable to a new approach to manufacturing that takes less labor time but causes more material waste. Examination of the labor efficiency variance reveals that it is favorable and larger than the unfavorable materials usage variance. Who is responsible? What action should be taken?arrow_forwardCarlo Lee Corp. has established the following standard cost per unit: Although 10,000 units were budgeted, only 8,800 units were produced. The purchasing department bought 55,000 lb of materials at a cost of $123,750. Actual pounds of materials used were 54,305. Direct labor cost was $186,550 for 18,200 hours worked. Required: Make journal entries to record the materials transactions, assuming that the materials price variance was recorded at the time of purchase. Make journal entries to record the labor variances.arrow_forwardCortez Manufacturing, Inc. has the following flexible budget formulas and amounts: Actual results for May for the production and sale of 5,000 units were as follows: Prepare a performance report for May that includes the identification of the favorable and unfavorable variances.arrow_forward

- USD Inc. has established the following standard cost per unit: Although 10,000 units were budgeted, 12,000 units were produced. The Purchasing department bought 50,000 lb of materials at a cost of $237,500. Actual pounds of materials used were 46,000. Direct labor cost was $287,500 for 25,000 hours worked. Required: Make journal entries to record the materials transactions, assuming that the materials price variance was recorded at the time of purchase. Make journal entries to record the labor variances.arrow_forwardMarten Company has a cost-benefit policy to investigate any variance that is greater than 1,000 or 10% of budget, whichever is larger. Actual results for the previous month indicate the following: The company should investigate: a. neither the materials variance nor the labor variance. b. the materials variance only. c. the labor variance only. d. both the materials variance and the labor variance.arrow_forwardBuenolorl Company produces a well-known cologne. The standard manufacturing cost of the cologne is described by the following standard cost sheet: Management has decided to investigate only those variances that exceed the lesser of 10% of the standard cost for each category or 20,000. During the past quarter, 250,000 four-ounce bottles of cologne were produced. Descriptions of actual activity for the quarter follow: a. A total of 1.35 million ounces of liquids was purchased, mixed, and processed. Evaporation was higher than expected. (No inventories of liquids are maintained.) The price paid per ounce averaged 0.42. b. Exactly 250,000 bottles were used. The price paid for each bottle was 0.048. c. Direct labor hours totaled 48,250, with a total cost of 733,000. Normal production volume for Buenolorl is 250,000 bottles per quarter. The standard overhead rates are computed by using normal volume. All overhead costs are incurred uniformly throughout the year. (Note: Round unit costs to the nearest cent and total amounts to the nearest dollar.) Required: 1. Calculate the upper and lower control limits for materials and labor. 2. Compute the total materials variance, and break it into price and usage variances. Would these variances be investigated? 3. Compute the total labor variance, and break it into rate and efficiency variances. Would these variances be investigated?arrow_forward

- At the beginning of the year, Lopez Company had the following standard cost sheet for one of its chemical products: Lopez computes its overhead rates using practical volume, which is 80,000 units. The actual results for the year are as follows: (a) Units produced: 79,600; (b) Direct labor: 158,900 hours at 18.10; (c) FOH: 831,000; and (d) VOH: 112,400. Required: 1. Compute the variable overhead spending and efficiency variances. 2. Compute the fixed overhead spending and volume variances.arrow_forwardRecompute the variances from the second Acme Inc. exercise using $0.0725 as the standard cost of the material and $14 as the standard labor cost per hour. How has your explanation of the variances changed?arrow_forwardA manufacturer planned to use $45 of variable overhead per unit produced, but in the most recent period, it actually used $47 of variable overhead per unit produced. During this same period, the company planned to produce 200 units but actually produced 220 units. What is the variable overhead spending variance?arrow_forward

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,