Concept explainers

Videos

1.

Journalize

1.

Explanation of Solution

Adjusting entries: Adjusting entries are those entries which are recorded at the end of the year, to update the income statement accounts (revenue and expenses) and balance sheet accounts (assets, liabilities, and

Record the adjusting entries of Company N.

| Date | Accounts title and explanation | Post Ref. |

Debit ($) |

Credit ($) |

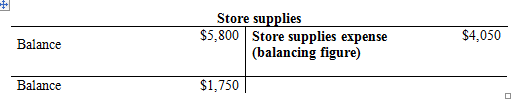

| a. | Store supplies expense (1) | 4,050 | ||

| Store supplies | 4,050 | |||

| (To record store supplies expense) | ||||

| b. | Insurance expenses | 1,400 | ||

| Prepaid expenses | 1,400 | |||

| (To record prepaid selling expenses) | ||||

| c. | 1,525 | |||

| 1,525 | ||||

| (To record depreciation expenses) | ||||

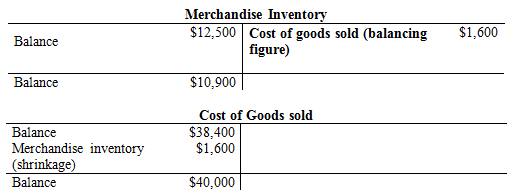

| d. | Cost of goods sold | 1,600 | ||

| Merchandise inventory (2) | 1,600 | |||

| (To record the inventory shrinkage) |

Table (1)

a. To record store supplies expense:

- Store supplies expense is an expense account and it is increased. Therefore, debit office supplies expense with $4,050.

- Store supplies are an asset account and it is decreased. Therefore, credit office supplies with $4,050.

b. To record prepaid insurance expenses:

- Insurance expense is an expense account and it is increased. Therefore, it is debited with $1,400.

- Prepaid expense is an asset account and it is decreased. Therefore, credit prepaid selling expense with $1,400.

c. To record depreciation expenses:

- Depreciation expense is an expense account and it is increased. Therefore, it is debited with $1,525.

- Prepaid expense is an asset account and it is decreased. Therefore, credit prepaid selling expense with $1,525.

d. To record the shrinkage of inventory:

- Cost of goods sold is an expense and they are increased. Thus, it is debited with $1,600.

- Inventory is an asset account, and they are increased. Hence, debit the inventory returns estimated account by $1,600.

Working Note:

Compute the Store supplies expense.

…… (1)

…… (1)

Compute the shrinkage of inventory.

…… (2)

…… (2)

2.

Prepare the multi-step income statement of Company N for the year ended January 31.

2.

Explanation of Solution

Multi-step income statement: The income statement represented in multi-steps with several subtotals, to report the income from principal operations, and separate the other expenses and revenues which affect net income, is referred to as multi-step income statement.

Prepare the income statement of Company N for the year ended January 31.

| Company N | ||

| Statement of Income | ||

| For the year ended January 31 | ||

| Particulars | Amount | Amount |

| Sales | $111,950 | |

| Less: Sales discounts | $2,000 | |

| Sales returns and allowances | $2,200 | ($4,200) |

| Net sales | $1,07,750 | |

| Less: Cost of goods sold (2) | ($40,000) | |

| Gross profit | $67,750 | |

| Expenses | ||

| Selling expenses | ||

| Depreciation expense—Store equipment | $1,525 | |

| Sales salaries expense | $17,500 | |

| Rent expense—Selling space | $7,500 | |

| Store supplies expense (1) | $4,050 | |

| Advertising expense | $9,800 | |

| Total selling expenses | $40,375 | |

| General and administrative expenses | ||

| Insurance expense | $1,400 | |

| Office salaries expense | $17,500 | |

| Rent expense—Office space | $7,500 | |

| Total general and administrative expenses | $26,400 | |

| Total expenses | ($66,775) | |

| Net income | $975 | |

Table (2)

Thus, the net income of Company N for the year ended January 31, 2017 is $975.

3.

Prepare the single-step income statement of Company N for the year ended December 31.

3.

Explanation of Solution

Single-step income statement: This statement displays the total revenues as one line item from which the total expenses including cost of goods sold is subtracted to arrive at the net profit /net loss for the period.

Prepare the income statement of Company N for the year ended January 31.

| Company N | ||

| Statement of Income | ||

| For the year ended January 31 | ||

| Particulars | Amount | Amount |

| Net sales | $107,750 | |

| Less: Expenses | ||

| Cost of goods sold (2) | $40,000 | |

| Selling expenses (Refer Table (2)) | $40,375 | |

| General and administrative expense (Refer Table (2)) | $26,400 | |

| Total expenses | ($1,06,775) | |

| Net income | $975 | |

Table (3)

Thus, the net income of Company N for the year ended January 31 is $975.

4.

Compute

4.

Explanation of Solution

Current ratio: Current ratio is one of the

Acid test ratio: It is a ratio used to determine a company’s ability to pay back its current liabilities by liquid assets that are current assets except inventory and prepaid expenses.

Gross margin ratio: The percentage of gross profit generated by every dollar of net sales is referred to as gross margin ratio. This ratio measures the profitability of a company by quantifying the amount of income earned from sales revenue generated after cost of goods sold are paid. The higher the ratio, the more ability to cover operating expenses. It is calculated by using the formula:

Compute current ratio, acid test ratio and gross margin ratio of Company N.

| Computation of ratios | |

| Particulars | Amount |

| Cash | $1,000 |

| Merchandise inventory (2) | $10,900 |

| Store supplies (1) | $1,750 |

| Prepaid insurance | $1,000 |

| Total current assets (A) | $14,650 |

| Current liabilities (B) | $10,000 |

| Current ratio | 1.47 |

| Quick assets (Cash) (C) | $1,000 |

| Current liabilities (D) | $10,000 |

| Acid-test ratio | 0.10 |

| Net Sales (E) | $107,750 |

| Less: Cost of Goods Sold (2) | ($40,000) |

| Gross margin (F) | $67,750 |

| Gross margin ratio | 0.63 or 63% |

Table (4)

The current ratio, acid- test ratio and gross margin ratio of Company N is 1.47, 0.10 and 0.63 or 63% respectively.

Want to see more full solutions like this?

Chapter 5 Solutions

Principles of Financial Accounting.

- Palisade Creek Co. is a retail business that uses the perpetual inventory system. The account balances for Palisade Creek as of May 1, 20Y6 (unless otherwise indicated), are as follows: During May, the last month of the fiscal year, the following transactions were completed: Record the following transactions on Page 21 of the journal: Instructions 1. Enter the balances of each of the accounts in the appropriate balance column of a four-column account. Write Balance in the item section, and place a check mark () in the Posting Reference column. Journalize the transactions for May, starting on Page 20 of the journal. 2. Post the journal to the general ledger, extending the month-end balances to the appropriate balance columns after all posting is completed. In this problem, you are not required to update or post to the accounts receivable and accounts payable subsidiary ledgers. 3. Prepare an unadjusted trial balance. 4. At the end of May, the following adjustment data were assembled. Analyze and use these data to complete (5) and (6). 5. (Optional) Enter the unadjusted trial balance on a 10-column end-of-period spreadsheet (work sheet), and complete the spreadsheet. 6. Journalize and post the adjusting entries. Record the adjusting entries on Page 22 of the journal. 7. Prepare an adjusted trial balance. 8. Prepare an income statement, a statement of stockholders equity, and a balance sheet. Assume that additional common stock of 10,000 was issued in January 20Y6. 9. Prepare and post the closing entries. Record the closing entries on Page 23 of the journal. Indicate closed accounts by inserting a line in both the Balance columns opposite the closing entry. Insert the new balance in the retained earnings account. 10. Prepare a post-closing trial balance.arrow_forwardWhich of the following describes features of a perpetual inventory system? A. Technology is normally used to record inventory changes. B. Merchandise bought is recorded as purchases. C. An adjusting journal entry is required at year end, to match physical counts to the asset account. D. Inventory is updated at the end of the period.arrow_forwardSelected transactions for Niles Co. during March of the current year are listed in Problem 6-1B. Instructions Journalize the entries to record the transactions of Niles Co. for March using the periodic inventory system.arrow_forward

- Periodic Inventory System Raynolde Company uses a periodic inventory system. At the end of the year, the following information is available: Required: Prepare a schedule to compute Raynoldes cost of goods sold.arrow_forwardPalisade Creek Co. is a merchandising business that uses the perpetual inventory system. The account balances for Palisade Creek Co. as of May 1, 2019 (unless otherwise indicated), are as follows: During May, the last month of the fiscal year, the following transactions were completed: Instructions 1. Enter the balances of each of the accounts in the appropriate balance column of a four-column account. Write Balance in the item section and place a check mark () in the Posting Reference column. Journalize the transactions for May, starting on Page 20 of the journal. 2. Post the journal to the general ledger, extending the month-end balances to the appropriate balance columns after all posting is completed. In this problem, you are not required to update or post to the accounts receivable and accounts payable subsidiary ledgers. 3. Prepare an unadjusted trial balance. 4. At the end of May, the following adjustment data were assembled. Analyze and use these data to complete (5) and (6). 5. (Optional) Enter the unadjusted trial balance on a 10-column end-of-period spreadsheet (work sheet), and complete the spreadsheet. 6. Journalize and post the adjusting entries. Record the adjusting entries on Page 22 of the journal. 7. Prepare an adjusted trial balance. 8. Prepare an income statement, a statement of owners equity, and a balance sheet. 9. Prepare and post the closing entries. Record the closing entries on Page 23 of the journal. Indicate closed accounts by inserting a line in both Balance columns opposite the closing entry. Insert the new balance in the owners capital account. 10. Prepare a post-closing trial balance.arrow_forwardAssume that the business in Exercise 7-9 maintains a perpetual inventory system. Determine the cost of merchandise sold for each sale and the inventory balance after each sale, assuming the last-in, first-out method. Present the data in the form illustrated in Exhibit 4.arrow_forward

- Assume that the business in Exercise 7-9 maintains a perpetual inventory system. Determine the cost of merchandise sold for each sale and the inventory balance after each sale, assuming the first-in, first-out method. Present the data in the form illustrated in Exhibit 3.arrow_forwardAssume that the business in Exercise 6-9 maintains a perpetual inventory system. Determine the cost of goods sold for each sale and the inventory balance after each sale, assuming the first-in, first-out method. Present the data in the form illustrated in Exhibit 3.arrow_forwardThe accounts and their balances in the ledger of Markeys Mountain Shop as of December 31, the end of its fiscal year, are as follows: Data for the adjustments are as follows. Assume that Markeys Mountain Shop uses the perpetual inventory system. a. Merchandise Inventory at December 31, 140,357. b. Store supplies inventory (on hand) at December 31, 540. c. Depreciation of building, 3,400. d. Depreciation of store equipment, 3,800. e. Salaries accrued at December 31, 1,250. f. Insurance expired during the year, 1,480. Required 1. Complete the work sheet after entering the account names and balances onto the work sheet. Ignore this step if using CLGL. 2. Journalize the adjusting entries. If using manual working papers, record adjusting entries on journal page 63.arrow_forward

- Journal entries using the periodic inventory system The following selected transactions were completed by Air Systems Company during January of the current year. Air Systems uses the periodic inventory system. Journalize the entries to record the transactions of Air Systems Company.arrow_forwardMacDonald Bookshop had the following transactions that occurred during February of this year: Required 1. Journalize the transactions for February in the cash payments journal. Assume the periodic inventory method is used. 2. Total and rule the journal. 3. Prove the equality of the debit and credit totals.arrow_forwardMacDonald Bookshop had the following transactions that occurred during February of this year: Required 1. Journalize the transactions for February in the cash payments journal. Assume the periodic inventory method is used. 2. If you are using Working Papers, total and rule the journal. Prove the equality of the debit and credit totals.arrow_forward

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning