Concept explainers

Videos

Ledger accounts,

The unadjusted

| Lakota Freight Co. Unadjusted Trial Balance March 31, 2018 |

|||

| Account No. | Debit Balances | Credit Balances | |

| Cash................................................ | 11 | 12,000 | |

| Supplies............................................ | 13 | 30,000 | |

| Prepaid Insurance.................................... | 14 | 3,600 | |

| Equipment.......................................... | 16 | 110,000 | |

| 17 | 25,000 | ||

| Trucks............................................... | 18 | 60,000 | |

| Accumulated Depreciation—Trucks................... | 19 | 15,000 | |

| Accounts Payable.................................... | 21 | 4,000 | |

| Common Stock...................................... | 31 | 26,000 | |

| Retained Earnings................................... | 32 | 70,000 | |

| Dividends........................................... | 33 | 15,000 | |

| Service Revenue..................................... | 41 | 160,000 | |

| Wages Expense...................................... | 51 | 45,000 | |

| Rent Expense........................................ | 53 | 10,600 | |

| Truck Expense....................................... | 54 | 9,000 | |

| Miscellaneous Expense............................... | 59 | 4,800 | |

| 300,000 | 300,000 | ||

The data needed to determine year-end adjustments are as follows:

(A) Supplies on hand at March 31 are $7,500.

(B) Insurance premiums expired during year are $1,800.

(C) Depreciation of equipment during year is $8,350.

(D) Depreciation of trucks during year is $6,200.

(E) Wages accrued but not paid at March 31 are $600.

Instructions

1. For each account listed in the trial balance, enter the balance in the appropriate Balance column of a four-column account and place a check mark (✓) in the Posting Reference column.

2. (Optional) Enter the unadjusted trial balance on an end-of-period spread sheet and complete the spreadsheet. Add the accounts listed in part (3) as needed.

3. Journalize and post the adjusting entries, inserting balances in the accounts affected. Record the adjusting entries on Page 26 of the journal. The following additional accounts from Lakota Freight Co.’s chart of accounts should be used: Wages Payable, 22; Supplies Expense, 52; Depreciation Expense—Equipment, 55; Depreciation Expense—Trucks, 56; Insurance Expense, 57.

4. Prepare an adjusted trial balance.

5. Prepare an income statement, a retained earnings statement, and a balance sheet.

6. Journalize and

7. Prepare a post-closing trial balance.

1.

Journal:

Journal is the book of original entry. Journal consists of the day-to-day financial transactions in a chronological order. The journal has two aspects; they are debit aspect and the credit aspect.

T-Accounts:

T-accounts are referred as T-account because its format represents the letter “T”. The T-accounts consists of the following:

- The title of accounts.

- The debit side (Dr) and,

- The credit side (Cr).

Adjusted trial balance:

The unadjusted trial balance is the summary of all the ledger accounts that appears on the ledger accounts before making adjusting journal entries.

Adjusting entries:

An adjusting entry is prepared when the trial balance is not up-to-date, and complete, and they are usually prepared at the end of the accounting period. This adjusting entry is essential for preparing the financial statements of the business.

Spreadsheet:

A spreadsheet is a worksheet. It is used while preparing a financial statement. It is a type of form having multiple columns and it is used in the adjustment process. The use of a worksheet is optional for any organization. A worksheet can neither be considered as a journal nor a part of the general ledger.

Statement of owners’ equity:

This statement reports the beginning owner’s equity and all the changes, which led to ending owners’ equity. Additional capital, net income from income statement is added to and drawing is deducted from beginning owner’s equity to arrive at the end result, ending owner’s equity.

Income statement:

An income statement is one of the financial statements which shows the revenues, and expenses of the company. The income statement is prepared to ascertain the net income/loss of the company, by deducting the expenses from the revenues.

Balance sheet:

A balance sheet is a financial statement consists of the assets, liabilities, and the stockholder’s equity of the company. The balance of the assets account must be equal to that of the liabilities and the stockholder’s equity account.

Closing entries:

Closing entries are recorded in order to close the temporary accounts such as incomes and expenses by transferring them to the permanent accounts. It is passed at the end of the accounting period, to transfer the final balance.

Post-Closing Trial Balance:

After passing all the journal entries and the closing entries of the permanent accounts and then further posting them to each of the respective accounts, a post-closing trial balance is prepared which consists of a list of all the permanent accounts. A post-closing trial balance serves as an evidence to prove that the balance of the permanent accounts is equal.

To prepare: The T-accounts.

Explanation of Solution

Record the transactions directly in their respective T-accounts, and determine their balances.

| Account: Cash Account no. 11 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Balance | ✓ | 12,000 | |||

| Account: Supplies Account no. 13 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Balance | ✓ | 30,000 | |||

| 31 | Adjusting | 26 | 22,500 | 7,500 | |||

| Account: Prepaid Insurance Account no. 14 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Balance | ✓ | 3,600 | |||

| 31 | Adjusting | 26 | 1,800 | 1,800 | |||

| Account: Equipment Account no. 16 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Balance | ✓ | 110,000 | |||

| Account: Accumulated Depreciation-Office equipment Account no. 17 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Balance | ✓ | 25,000 | |||

| 31 | Adjusting | 26 | 8,350 | 33,350 | |||

| Account: Trucks Account no. 18 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Balance | ✓ | 60,000 | |||

| Account: Accumulated Depreciation- Truck Account no. 19 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Balance | ✓ | 15,000 | |||

| 31 | Adjusting | 26 | 6,200 | 21,200 | |||

| Account: Accounts Payable Account no. 21 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Balance | ✓ | 4,000 | |||

| Account: Wages Payable Account no. 22 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Adjusting | 26 | 600 | 600 | ||

| Account: Common Stock Account no. 31 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Balance | ✓ 1 | 26,000 | 26,000 | ||

| Account: Retained Earnings Account no. 32 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Balance | ✓ | 70,000 | |||

| 31 | Closing | 27 | 51,150 | 121,150 | |||

| 31 | Closing | 27 | 15,000 | 106,150 | |||

| Account: Dividends Account no. 33 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Balance | ✓ 1 | 15,000 | |||

| 31 | Closing | 27 | 15,000 | ||||

| Account: Income Summary Account no. 34 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Closing | 27 | 160,000 | 160,000 | ||

| 31 | Closing | 27 | 108,850 | 51,150 | |||

| 31 | Closing | 27 | 51,150 | ||||

| Account: Service revenue Account no. 41 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Balance | ✓ | 160,000 | |||

| 31 | Closing | 27 | 160,000 | ||||

| Account: Wages expense Account no. 51 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Balance | ✓ | 45,000 | |||

| 31 | Adjusting | 26 | 600 | 45,600 | |||

| 31 | Closing | 27 | 45,600 | ||||

| Account: Supplies Expense Account no. 52 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Adjusting | 26 | 22,500 | 22,500 | ||

| 31 | Closing | 27 | 22,500 | ||||

| Account: Rent expense Account no. 53 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Balance | ✓ | 10,600 | |||

| 31 | Closing | 27 | 10,600 | ||||

| Account: Truck Expense Account no. 54 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Balance | ✓ | 9,000 | |||

| 31 | Closing | 27 | 9,000 | ||||

| Account: Depreciation Expense- Equipment Account no. 55 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Adjusting | 26 | 8,350 | 8,350 | ||

| 31 | Closing | 27 | 8,350 | ||||

| Account: Depreciation Expense- Equipment Account no. 55 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Adjusting | 26 | 8,350 | 8,350 | ||

| 31 | Closing | 27 | 8,350 | ||||

| Account: Depreciation Expense- Trucks Account no. 56 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| March | 31 | Adjusting | 26 | 6,200 | 6,200 | ||

| 31 | Closing | 27 | 6,200 | ||||

| Account: Insurance expense Account no. 57 | |||||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||||

| Debit ($) | Credit ($) | ||||||||

| 2018 | |||||||||

| March | 31 | Adjusting | 26 | 1,800 | 1,800 | ||||

| 31 | Closing | 27 | 1,800 | ||||||

| Account: Miscellaneous expense Account no. 59 | |||||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||||

| Debit ($) | Credit ($) | ||||||||

| 2018 | |||||||||

| March | 31 | Balance | ✓ | 4,800 | |||||

| 31 | Closing | 27 | 4,800 | ||||||

2.

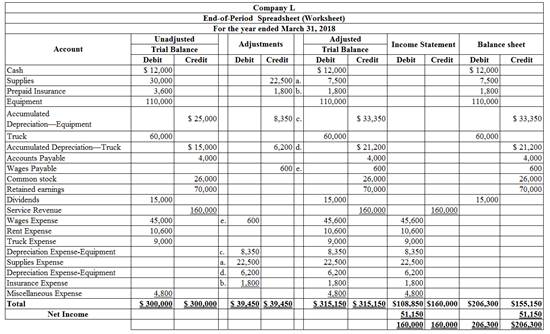

To enter: The unadjusted trial balance on an end-of-period spreadsheet, and complete the spreadsheet.

Explanation of Solution

The unadjusted trial balance on an end-of-period spreadsheet is prepared as follows:

Table (1)

Hence, the unadjusted trial balance on an end-of-period spreadsheet is prepared and completed.

3.

To Journalize and post: The adjusting entries.

Explanation of Solution

The adjusting entries are journalized as follows:

| Date | Description |

Post Ref. |

Debit ($) | Credit ($) | |

| 2018 | Supplies expense | 52 | 22,500 | ||

| March | 31 | Supplies

|

13 | 22,500 | |

| (To record the supplies used) | |||||

Table (2)

- Supplies expense is an expense account, and it is increased. Hence, debit the supplies expense account by $22,500.

- Supplies are the asset account, and it is increased. Hence, credit the supplies account by $22,500.

| Date | Description |

Post Ref. |

Debit ($) | Credit ($) | |

| 2018 | Insurance expense | 57 | 1,800 | ||

| March | 31 | Prepaid insurance | 14 | 1,800 | |

| (To record the insurance expired) | |||||

Table (3)

- Insurance expense is an expense account, and it is increased. Hence, debit the insurance expense account by $1,800.

- Prepaid insurance is an asset account, and it is decreased. Hence, credit the prepaid insurance account by $1,800.

| Date | Description |

Post Ref. |

Debit ($) | Credit ($) | |

| 2018 | Depreciation expense-Equipment | 55 | 8,350 | ||

| March | 31 | Accumulated depreciation- Equipment | 17 | 8,350 | |

| (To record the equipment depreciation) | |||||

Table (4)

- Depreciation expense is an expense account, and it is increased. Hence, debit the wages expense account by $8,350.

- Accumulated depreciation is a contra asset account, and it is increased. Hence, credit the accumulated depreciation account by $8,350.

| Date | Description |

Post Ref. |

Debit ($) | Credit ($) | |

| 2018 | Depreciation expense-Truck | 56 | 6,200 | ||

| March | 31 | Accumulated depreciation- Truck | 19 | 6,200 | |

| (To record the truck depreciation) | |||||

Table (5)

- Depreciation expense is an expense account, and it is increased. Hence, debit the wages expense account by $6,200.

- Accumulated depreciation is a contra asset account, and it is increased. Hence, credit the accumulated depreciation account by $6,200.

| Date | Description |

Post Ref. |

Debit ($) | Credit ($) | |

| 2018 | Wages expense | 51 | 600 | ||

| March | 31 | Wages payable | 22 | 600 | |

| (To record the wages accrued) | |||||

Table (6)

- Wages expense is an expense account, and it is increased. Hence, debit the wages expense account by $600.

- Wages payable is a liability account, and it is increased. Hence, credit the wages payable account by $600.

4.

To prepare: An adjusted trial balance for Company L, as of March 31, 2018.

Explanation of Solution

Prepare an adjusted trial balance for Company L, as of March 31, 2018.

| Company L | |||

| Adjusted Trial Balance | |||

| March 31, 2018 | |||

| Accounts | Account Number | Debit Balances | Credit Balances |

| Cash | 11 | 12,000 | |

| Supplies | 13 | 7,500 | |

| Prepaid Insurance | 14 | 1,800 | |

| Equipment | 16 | 110,000 | |

| Accumulated depreciation- Equipment | 17 | 33,350 | |

| Trucks | 18 | 60,000 | |

| Accumulated depreciation- Trucks | 19 | 21,200 | |

| Accounts payable | 21 | 4,000 | |

| Wages Payable | 22 | 600 | |

| Common stock | 31 | 26,000 | |

| Retained earnings | 32 | 70,000 | |

| Dividends | 15,000 | ||

| Service revenue | 41 | 160,000 | |

| Wages expense | 51 | 45,600 | |

| Supplies expense | 52 | 22,500 | |

| Rent Expense | 53 | 10,600 | |

| Truck Expense | 54 | 9,000 | |

| Depreciation Expense- Equipment | 55 | 8,350 | |

| Depreciation Expense- Trucks | 56 | 6,200 | |

| Insurance Expense | 57 | 1,800 | |

| Miscellaneous Expense | 59 | 4,800 | |

| 315,150 | 315,150 | ||

Table (7)

5.

Explanation of Solution

The net income of Company L for the month of March is $51,150.

| Company L | ||

| Income Statement | ||

| For the year ended March 31, 2018 | ||

| Particulars | Amount ($) | Amount ($) |

| Revenue: | ||

| Service revenue | $160,000 | |

| Expenses: | ||

| Wages Expense | 45,600 | |

| Supplies Expense | 22,500 | |

| Rent Expense | 10,600 | |

| Truck Expense | 9,000 | |

| Depreciation Expense-Equipment | 8,350 | |

| Depreciation Expense-Trucks | 6,200 | |

| Insurance Expense | 1,800 | |

| Miscellaneous Expense | 4,800 | |

| Total Expenses | 108,850 | |

| Net Income | $51,150 | |

Table (8)

Hence, the net income of Company L for the year ended March 31, 2018 is $51,150.

6.

To Journalize: The closing entries for Company L.

Explanation of Solution

Closing entry for revenue and expense accounts:

| Date | Accounts title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| March 31, 2018 | Service revenue | 41 | 160,000 | |

| Income summary | 34 | 160,000 | ||

| (To close the balances of revenue account) | ||||

| March 31, 2018 | Income summary | 34 | 108,850 | |

| Wages expense | 51 | 45,600 | ||

| Supplies Expense | 52 | 22,500 | ||

| Rent Expense | 53 | 10,600 | ||

| Truck Expense | 54 | 9,000 | ||

| Depreciation Expense–Equipment | 55 | 8,350 | ||

| Depreciation Expense–Trucks | 56 | 6,200 | ||

| Insurance Expense | 57 | 1,800 | ||

| Miscellaneous Expense | 59 | 4,800 | ||

| (To close the balances of expense account) | ||||

| March 31, 2018 | Income summary | 34 | 51,150 | |

| Retained earnings | 32 | 51,150 | ||

| (To Close the excess of revenue to expenses) | ||||

| March 31, 2018 | Retained earnings | 32 | 15,000 | |

| Dividends | 33 | 15,000 | ||

| (To close the dividend account to retained earnings account) | ||||

Table (11)

- Laundry revenue is revenue account. Since the amount of revenue is closed and transferred to Income summary account. Here, Company L earned an income of $160,000. Therefore, it is debited.

- Wages Expense, Rent Expense, Insurance Expense, Supplies Expense, Depreciation Expenses, and Miscellaneous Expense are expense accounts. Since the amount of expenses are closed to Income Summary account. Therefore, it is credited.

- Closing entries are also passed in order to close the excess of revenue over the expenses, and the dividend account.

7.

To prepare: The post–closing trial balance of Company L for the month ended March 31, 2018.

Explanation of Solution

Prepare a post–closing trial balance of Company L for the month ended March 31, 2018 as follows:

|

Company L Post-closing Trial Balance March 31, 2018 |

|||

| Particulars |

Account Number |

Debit $ | Credit $ |

| Cash | 11 | 12,000 | |

| Supplies | 13 | 7,500 | |

| Prepaid insurance | 14 | 1,800 | |

| Equipment | 16 | 110,000 | |

| Accumulated depreciation- Equipment | 17 | 33,350 | |

| Trucks | 18 | 60,000 | |

| Accumulated depreciation- Trucks | 19 | 21,200 | |

| Accounts payable | 21 | 4,000 | |

| Wages payable | 22 | 600 | |

| Common stock | 31 | 26,000 | |

| Retained earnings | 106,150 | ||

| Total | 191,300 | 191,300 | |

Table (12)

The debit column and credit column of the post–closing trial balance are agreed, both having balance of $191,300

Want to see more full solutions like this?

Chapter 4 Solutions

CengageNOWv2, 2 terms Printed Access Card for Warren/Reeve/Duchac’s Financial & Managerial Accounting, 14th

Additional Business Textbook Solutions

Construction Accounting And Financial Management (4th Edition)

Accounting For Governmental & Nonprofit Entities

Principles Of Taxation For Business And Investment Planning 2020 Edition

Financial Accounting, Student Value Edition (5th Edition)

Managerial Accounting (5th Edition)

Managerial Accounting: Tools for Business Decision Making

- UNCOLLECTIBLE ACCOUNTSALLOWANCE METHOD Lewis Warehouse used the allowance method to record the following transactions, adjusting entries, and closing entries during the year ended December 31, 20--: Selected accounts and beginning balances on January 1, 20--, are as follows: REQUIRED 1. Open the three selected general ledger accounts. 2. Enter the transactions and the adjusting and closing entries in a general journal (page 6). After each entry, post to the appropriate selected accounts. 3. Determine the net realizable value as of December 31, 20--.arrow_forwardThe following trial balance was taken from the books of Venus Corporation at December 31, 2020: Account Debit Credit Cash........................................................................................................... $ 40,000 Accounts Receivable.................................................................................... 106,000 Prepaid Rent ............................................................................................... 12,800 Note Receivable................................................................................................ 8,000 Merchandise Inventory................................................................................... 54,000 Unexpired Insurance......................................................................................... 4,800 Furniture and…arrow_forwardThe following trial balance was taken from the books of Venus Corporation at December 31, 2020: Account Debit Credit Cash........................................................................................................... $ 40,000 Accounts Receivable.................................................................................... 106,000 Prepaid Rent ............................................................................................... 12,800 Note Receivable................................................................................................ 8,000 Merchandise Inventory................................................................................... 54,000 Unexpired Insurance......................................................................................... 4,800 Furniture and…arrow_forward

- The post-closing trial balance of Beamer Manufacturing Co. onApril 30 is reproduced as follows:Beamer Manufacturing Co.Post-Closing Trial BalanceApril 30, 2011 Cash . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 25,000Accounts Receivable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65,000Finished Goods .................................. 120,000Work in Process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35,000Materials . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18,000Building . . . ...................................... 480,000Accumulated Depreciation—Building ............. $ 72,000Factory Equipment . . ............................ 220,000Accumulated Depreciation—Factory Equipment . . . 66,000Office Equipment ................................ 60,000Accumulated Depreciation—Office Equipment . . . . 36,000Accounts Payable . . .............................. 95,000Capital Stock…arrow_forwardThe adjusted Trail Balance of Saudi Gold Co Contained the following accounts at November 30, the end of the company’s fiscal year : Saudi Gold Co. Adjusted Trial Balance November 30, 2019 Dr. Cr. Cash............................................................... Sr 28,700 Accounts Receivable..................................... 33,700 Inventory........................................................ 45,000 Supplies......................................................... 1,500 Equipment...................................................... 133,000 Accumulated Depreciation—Equipment..... Sr 39,000 Notes Payable................................................ 51,000 Accounts Payable......................................... 48,500 Share Capital—Ordinary............................... 90,000 Retained…arrow_forwardPA5. 7.4 Brown Inc. records purchases in a purchases journal and purchase returns in the general journal. Record the following transactions using a purchases journal, a general journal, and an accounts payable subsidiary ledger. The company uses the periodic method of accounting for inventory. Oct.1 Purchased inventory on account from Price Inc. for $2,000 Oct.1 Purchased inventory on account from Cabrera Inc. for $3,000 Oct.8 Returned half of the inventory to Price Inc. Oct.9 Purchased inventory on account from Price Inc. for $4,200arrow_forward

- Prepare a November 30 balance sheet in proper form for Green Bay Delivery Service from the following alphabetical list of the accounts at November 30: Accounts receivable....................... $10,000Accounts payable................................ 18,000Building.............................................. 28,000Cash.................................................. 8,000Notes payable..................................... 45,000Office equipment................................... 12,000R. Perkins, Capital................................ 50,000Trucks............................................... 55,000[Hint: Please follow the balance sheet format. You need to re-organize the order of the account. Remember to include the heading (name of company...etc)]arrow_forwardThe Trial Balance TBA Limited contained the following accounts (alphabetically) at December 31, 2020, the end of company's fiscal year. Accounts..... ..... ** Balances ($)....||| .... Accounts ... ........... ...... ..... Balances ($) Accumulated Depreciation-Building.... ..... 121000 . ... ||| .... Loss on Sale of Property Accumulated Depreciation-Equipment. . 36000.... ||| .... Merchandise Inventory Additional Paid in Capital-Common Stock.. 222000.... ||| - . . . Mortgage Loan.. . . **** .... .... ... 7380 231000 ............. 109000 Auditors Fee ... .... .... .... ... ... ... ..* 209000.... III.... Rent Revenue .. .... ... .... .... .. 53000 Retained Earnings .. . 52900 Buildings.. 410000.... |II - .......... ................... ............ Cash ... ......... ****** 150710.. .. |||. ... Salaries and Wages Expense 104000 Common Stock ($2 each).... ... .... .... .... ... ....... 104000....II.... Sales .... ........ .... .... .... ..... .*.* *.** 1754000 Cost of Goods Sold 1086000....…arrow_forwardNO. : Date : | The following was the trial balance extract from ABC Tradina as at 31 March 2019 Particulars Purchases and sales Inventory on IAprl 2018 Capital Bank overdraft Cash Discount allowad and received Return inwards and outwards Carriage outwards Office expenses Fixturos and fittings Delivery van Account receivables and account payab les Rent and insurance Credit CRm) 41,000 Debit CRM) 22/860 5, 100 8,170 4,300 140 1.440 790 2/180 930 570 450 1/210 2,000 IL, 900 1.790 6,720 Drawings Wages and Sal aries Total 2,850 8,980 611690 61.690 Additional information as at 31 March 2019 : ca) Inventory on 31 March 2019 was (b) Wages and salaries accrued as at 31 March 2019 was Rm210 ; Outstanding office expen ses was RM 30 Cc) Rent and insurance prepaid was km 150 RM 4250 Raquired: (1) Preapare the Statement of Piofit or Loss and Other Comprehensive Income for the year ended 31 March 2019 |(ii) Preapare statement of Financial Position as at 31 March 2019 .arrow_forward

- The Trial Balance of BMR Limited contained the following accounts (alphabetically) at December 31, 2020, the end of company's fiscal year.Accounts …… …… …… …… …… …… …… Balances ($) . . . . ||| . . . . Accounts …… …… …… …… …… Balances ($)Accumulated Depreciation-Building…. …… 130000 . . . . ||| . . . . Loss on Sale of Property …. …. …. …. 7680Accumulated Depreciation-Equipment….…. 36000 . . . . ||| . . . . Merchandise Inventory …. …. ……. 230000Additional Paid in Capital-Common Stock.. 233000 . . . . ||| . . . . Mortgage Loan …. …. …. …. …. …… 114000Auditors Fee …. …. …. …. …. …. ….. ….. ….. .. 207000 . . . . ||| . . . . Rent Revenue …. …. …. …. …. …. … 53000Buildings…. …. …. …. …. …. ….. ….. ….. ….. ... 401000 . . . . ||| . . . . Retained Earnings …. …. …. …. …… 52600Cash …. …. …. …. …. …. ….. ….. ….. ….. ….. …. 204340 . . . . ||| . . . . Salaries and Wages Expense …. …. 106000Common Stock ($2 each)…. …. …. …. …. ….. 113000 . . . . ||| . . . . Sales …. …. …. …. …. …. ….. ….. …….…arrow_forward! Required information of 2 [The following information applies to the questions displayed below.] Nix'lt Company's ledger on July 31, its fiscal year-end, includes the following selected accounts that have normal balances (Nix'lt uses the perpetual inventory system). Merchandise inventory Retained earnings Dividends Sales $ 37,800 Sales returns and allowances Cost of goods sold Depreciation expense Salaries expense Miscellaneous expenses $ 6,500 105,000 10,300 32,500 5,000 ped 115,300 7,e00 160, 200 4,700 Sales discounts pok int A physical count of its July 31 year-end inventory discloses that the cost of the merchandise inventory still available is $35,900. rint rences Prepare journal entries to close the balances in temporary revenue and expense accoints. Remember to consider the entry for shrinkage from QS 4-9. (The solution from QS 4-9 is required to complete this question.) In Fn Lock F10 F11 F12 F4 EZ F7 F8 F9 28 F5 F6arrow_forwardThe Trial Balance of BMR Limited contained the following accounts (alphabetically) at December 31, 2020, the end of company's fiscal year.Accounts …… …… …… …… …… …… …… Balances ($) . . . . ||| . . . . Accounts …… …… …… …… …… Balances ($)Accumulated Depreciation-Building…. …… 130000 . . . . ||| . . . . Loss on Sale of Property …. …. …. …. 7680Accumulated Depreciation-Equipment….…. 36000 . . . . ||| . . . . Merchandise Inventory …. …. ……. 230000Additional Paid in Capital-Common Stock.. 233000 . . . . ||| . . . . Mortgage Loan …. …. …. …. …. …… 114000Auditors Fee …. …. …. …. …. …. ….. ….. ….. .. 207000 . . . . ||| . . . . Rent Revenue …. …. …. …. …. …. … 53000Buildings…. …. …. …. …. …. ….. ….. ….. ….. ... 401000 . . . . ||| . . . . Retained Earnings …. …. …. …. …… 52600Cash …. …. …. …. …. …. ….. ….. ….. ….. ….. …. 204340 . . . . ||| . . . . Salaries and Wages Expense …. …. 106000Common Stock ($2 each)…. …. …. …. …. ….. 113000 . . . . ||| . . . . Sales …. …. …. …. …. …. ….. ….. …….…arrow_forward

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning- Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning

Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning