Concept explainers

Videos

Ledger accounts,

The unadjusted

| Recessive Interiors Unadjusted Trial Balance January 31, 2018 | |||

| Account No. | Debit Balances | Credit Balances | |

| Cash..................................................... | 11 | 13,100 | |

| Supplies................................................. | 13 | 8,000 | |

| Prepaid Insurance......................................... | 14 | 7,500 | |

| Equipment............................................... | 16 | 113,000 | |

| 17 | 12,000 | ||

| Trucks.................................................... | 18 | 90,000 | |

| Accumulated Depreciation—Trucks........................ | 19 | 27,100 | |

| Accounts Payable......................................... | 21 | 4,500 | |

| Common Stock........................................... | 31 | 30,000 | |

| Retained Earnings........................................ | 32 | 96,400 | |

| Dividends................................................ | 33 | 3,000 | |

| Service Revenue.......................................... | 41 | 155,000 | |

| Wages Expense........................................... | 51 | 72,000 | |

| Rent Expense............................................. | 52 | 7,600 | |

| Truck Expense............................................ | 53 | 5,350 | |

| Miscellaneous Expense.................................... | 59 | 5,450 | |

| 325,000 | 325,000 | ||

The data needed to determine year-end adjustments are as follows:

(A) Supplies on hand at January 31 are $2,850.

(B) Insurance premiums expired during the year are $3,1 SO.

(C) Depreciation of equipment during the year is $5,250.

(D) Depreciation of trucks during the year is $4,000.

(E) Wages accrued but not paid at January 31 are $900.

Instructions

1. For each account listed in the unadjusted trial balance, enter the balance in the appropriate Ba lance column of a four-column account and place a check mark (✓) in the Posting Reference column.

2. (Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet. Add the accounts listed in part (3) as needed.

3. Journalize and post the adjusting entries, inserting balances in the accounts affected. Record the adjusting entries on Page 26 of the journal. The following additional accounts from Recessive Interiors’ chart of accounts should be used: Wages Payable, 22; Depreciation Expense—Equipment, 54; Supplies Expense, 55; Depreciation Expense—Trucks, 56; Insurance Expense, 57.

4. Prepare an adjusted trial balance.

5. Prepare an income statement, a retained earnings statement, and a balance sheet.

6. Journalize and

7. Prepare a post-closing trial balance.

1.

Journal:

Journal is the book of original entry. Journal consists of the day-to-day financial transactions in a chronological order. The journal has two aspects; they are debit aspect and the credit aspect.

T-Accounts:

T-accounts are referred as T-account because its format represents the letter “T”. The T-accounts consists of the following:

- The title of accounts.

- The debit side (Dr) and,

- The credit side (Cr).

Adjusted trial balance:

The unadjusted trial balance is the summary of all the ledger accounts that appears on the ledger accounts before making adjusting journal entries.

Adjusting entries:

An adjusting entry is prepared when the trial balance is not up-to-date, and complete, and they are usually prepared at the end of the accounting period. This adjusting entry is essential for preparing the financial statements of the business.

Spreadsheet:

A spreadsheet is a worksheet. It is used while preparing a financial statement. It is a type of form having multiple columns and it is used in the adjustment process. The use of a worksheet is optional for any organization. A worksheet can neither be considered as a journal nor a part of the general ledger.

Statement of owners’ equity:

This statement reports the beginning owner’s equity and all the changes, which led to ending owners’ equity. Additional capital, net income from income statement is added to and drawing is deducted from beginning owner’s equity to arrive at the end result, ending owner’s equity.

Income statement:

An income statement is one of the financial statements which shows the revenues, and expenses of the company. The income statement is prepared to ascertain the net income/loss of the company, by deducting the expenses from the revenues.

Balance sheet:

A balance sheet is a financial statement consists of the assets, liabilities, and the stockholder’s equity of the company. The balance of the assets account must be equal to that of the liabilities and the stockholder’s equity account.

Closing entries:

Closing entries are recorded in order to close the temporary accounts such as incomes and expenses by transferring them to the permanent accounts. It is passed at the end of the accounting period, to transfer the final balance.

Post-Closing Trial Balance:

After passing all the journal entries and the closing entries of the permanent accounts and then further posting them to each of the respective accounts, a post-closing trial balance is prepared which consists of a list of all the permanent accounts. A post-closing trial balance serves as an evidence to prove that the balance of the permanent accounts is equal.

To prepare: The T-accounts.

Explanation of Solution

Record the transactions directly in their respective T-accounts, and determine their balances.

| Account: Cash Account no. 11 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| January | 31 | Balance | ✓ | 13,100 | |||

| Account: Supplies Account no. 13 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| January | 31 | Balance | ✓ | 8,000 | |||

| 31 | Adjusting | 26 | 5,150 | 2,850 | |||

| Account: Prepaid Insurance Account no. 14 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| January | 31 | Balance | ✓ | 7,500 | |||

| 31 | Adjusting | 26 | 3,150 | 4,350 | |||

| Account: Equipment Account no. 16 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| January | 31 | Balance | ✓ | 113,000 | |||

| Account: Accumulated Depreciation-Office equipment Account no. 17 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| January | 31 | Balance | ✓ | 12,000 | |||

| 31 | Adjusting | 26 | 5,250 | 17,250 | |||

| Account: Trucks Account no. 18 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| January | 31 | Balance | ✓ | 90,000 | |||

| Account: Accumulated Depreciation- Truck Account no. 19 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| January | 31 | Balance | ✓ | 27,100 | |||

| 31 | Adjusting | 26 | 4,000 | 31,100 | |||

| Account: Accounts Payable Account no. 21 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| January | 31 | Balance | ✓ | 4,500 | |||

| Account: Wages Payable Account no. 22 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| January | 31 | Adjusting | 26 | 900 | 900 | ||

| Account: Common Stock Account no. 31 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| January | 31 | Balance | ✓ | 900 | 30,000 | ||

| Account: Retained Earnings Account no. 32 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| January | 31 | Balance | ✓ 1 | 96,400 | |||

| 31 | Closing | 27 | 46,150 | 142,550 | |||

| 31 | Closing | 27 | 3,000 | 139,550 | |||

| Account: Dividends Account no. 33 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| January | 31 | Balance | ✓ | 3,000 | |||

| 31 | Closing | 27 | 3,000 | ||||

| Account: Income Summary Account no. 34 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| January | 31 | Closing | 27 | 155,000 | 155,000 | ||

| 31 | Closing | 27 | 108,850 | 46,150 | |||

| 31 | Closing | 27 | 46,150 | ||||

| Account: Service revenue Account no. 41 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| January | 31 | Balance | ✓ | 155,000 | |||

| 31 | Closing | 27 | 155,000 | ||||

| Account: Wages expense Account no. 51 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| January | 1 | Balance | ✓ | 72,000 | |||

| 31 | Adjusting | 26 | 900 | 72,900 | |||

| 31 | Closing | 27 | 72,900 | ||||

| Account: Rent expense Account no. 52 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| January | 31 | Balance | ✓ | 7,600 | |||

| 31 | Closing | 27 | 7,600 | ||||

| Account: Truck Expense Account no. 53 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| January | 31 | Balance | ✓ | 5,350 | |||

| 31 | Closing | 27 | 5,350 | ||||

| Account: Depreciation Expense- Equipment Account no. 54 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| January | 31 | Adjusting | 26 | 5,250 | 5,250 | ||

| 31 | Closing | 27 | 5,250 | ||||

| Account: Supplies Expenses Account no. 55 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| January | 31 | Adjusting | 26 | 5,150 | 5,150 | ||

| 31 | Closing | 27 | 5,150 | ||||

| Account: Depreciation Expense- Trucks Account no. 56 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| January | 31 | Adjusting | 26 | 4,000 | 4,000 | ||

| 31 | Closing | 27 | 4,000 | ||||

| Account: Insurance expense Account no. 57 | ||||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | |||

| Debit ($) | Credit ($) | |||||||

| 2018 | ||||||||

| January | 31 | Adjusting | 26 | 3,150 | 3,150 | |||

| 31 | Closing | 27 | 3,150 | |||||

| Account: Miscellaneous expense Account no. 59 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| January | 1 | Balance | ✓ | 5,450 | |||

| 31 | Closing | 27 | 5,450 | ||||

2.

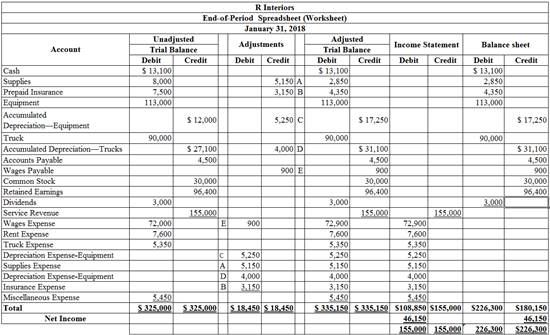

To enter: The unadjusted trial balance on an end-of-period spreadsheet, and complete the spreadsheet.

Explanation of Solution

The unadjusted trial balance on an end-of-period spreadsheet is prepared as follows:

Table (1)

Hence, the unadjusted trial balance on an end-of-period spreadsheet is prepared and completed.

3.

To Journalize and post: The adjusting entries.

Explanation of Solution

The adjusting entries are journalized as follows:

| Date | Description |

Post Ref. |

Debit ($) | Credit ($) | |

| 2018 | Wages expense | 51 | 900 | ||

| January | 31 | Wages payable | 22 | 900 | |

| (To record the wages accrued) | |||||

Table (2)

- Wages expense is an expense account, and it is increased. Hence, debit the wages expense account by $900.

- Wages payable is a liability account, and it is increased. Hence, credit the wages payable account by $900.

| Date | Description |

Post Ref. |

Debit ($) | Credit ($) | |

| 2018 | Depreciation expense-Equipment | 54 | 5,250 | ||

| January | 31 | Accumulated depreciation- Equipment | 17 | 5,250 | |

| (To record the equipment depreciation) | |||||

Table (3)

- Depreciation expense is an expense account, and it is increased. Hence, debit the wages expense account by $5,250.

- Accumulated depreciation is a contra asset account, and it is increased. Hence, credit the accumulated depreciation account by $5,250.

| Date | Description |

Post Ref. |

Debit ($) | Credit ($) | |

| 2018 | Depreciation expense-Truck | 56 | 4,000 | ||

| January | 31 | Accumulated depreciation- Truck | 19 | 4,000 | |

| (To record the truck depreciation) | |||||

Table (4)

- Depreciation expense is an expense account, and it is increased. Hence, debit the wages expense account by $4,000.

- Accumulated depreciation is a contra asset account, and it is increased. Hence, credit the accumulated depreciation account by $4,000.

| Date | Description |

Post Ref. |

Debit ($) | Credit ($) | |

| 2018 | Supplies expense | 55 | 5,150 | ||

| January | 31 | Supplies

|

13 | 5,150 | |

| (To record the supplies used) | |||||

Table (5)

- Supplies expense is an expense account, and it is increased. Hence, debit the supplies expense account by $5,150.

- Supplies are the asset account, and it is increased. Hence, credit the supplies account by $5,150.

| Date | Description |

Post Ref. |

Debit ($) | Credit ($) | |

| 2018 | Insurance expense | 57 | 3,150 | ||

| January | 31 | Prepaid insurance | 14 | 3,150 | |

| (To record the insurance expense) | |||||

Table (6)

- Insurance expense is an expense account, and it is increased. Hence, debit the insurance expense account by $3,150.

- Prepaid insurance is an asset account, and it is decreased. Hence, credit the prepaid insurance account by $3,150.

4.

To prepare: An adjusted trial balance for R interiors, as of January 31, 2018.

Explanation of Solution

Prepare an adjusted trial balance for R interiors, as of January 31, 2018.

| R interiors | |||

| Adjusted Trial Balance | |||

| January 31, 2018 | |||

| Accounts | Account Number | Debit Balances | Credit Balances |

| Cash | 11 | 13,100 | |

| Supplies | 13 | 2,850 | |

| Prepaid Insurance | 14 | 4,350 | |

| Equipment | 16 | 113,000 | |

| Accumulated depreciation- Equipment | 17 | 17,250 | |

| Trucks | 18 | 90,000 | |

| Accumulated depreciation- Trucks | 19 | 31,100 | |

| Accounts payable | 21 | 4,500 | |

| Wages Payable | 22 | 900 | |

| Common Stock | 31 | 30,0 00 | |

| Retained earnings | 32 | 96,400 | |

| Dividends | 33 | 3,000 | |

| Service revenue | 41 | 155,000 | |

| Wages expense | 51 | 72,900 | |

| Rent expense | 52 | 7,600 | |

| Truck Expense | 53 | 5,350 | |

| Depreciation Expense- Equipment | 54 | 5,250 | |

| Supplies expense | 55 | 5,150 | |

| Depreciation Expense- Trucks | 56 | 4,000 | |

| Insurance Expense | 57 | 3,150 | |

| Miscellaneous Expense | 59 | 5,450 | |

| 335,150 | 335,150 | ||

Table (7)

5.

Explanation of Solution

The net income of R interiors for the month of January is $46,150.

| R interiors | ||

| Income Statement | ||

| For the year ended January 31, 2018 | ||

| Particulars | Amount ($) | Amount ($) |

| Revenue: | ||

| Laundry revenue | $155,000 | |

| Expenses: | ||

| Wages Expense | $72,900 | |

| Rent Expense | 7,600 | |

| Truck Expense | 5,350 | |

| Depreciation Expense-Equipment | 5,250 | |

| Supplies Expense | 5,150 | |

| Depreciation Expense-Trucks | 4,000 | |

| Insurance Expense | 3,150 | |

| Miscellaneous Expense | 5,450 | |

| Total Expenses | 108,850 | |

| Net Income | $46,150 | |

Table (8)

Hence, the net income of R interiors for the year ended January 31, 2018 is $46,150.

6.

To Journalize: The closing entries for R interiors.

Explanation of Solution

Closing entry for revenue and expense accounts:

| Journal Page 27 | ||||

| Date | Accounts title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 31, 2018 | Service Revenue | 41 | 155,000 | |

| Income Summary | 34 | 155,000 | ||

| (To record the closure of revenues account ) | ||||

| January 31 | Income Summary | 34 | 108,850 | |

| Wages Expense | 51 | 72,900 | ||

| Rent Expense | 52 | 7,600 | ||

| Truck Expense | 53 | 5,350 | ||

| Depreciation Expense-Equipment | 54 | 5,250 | ||

| Supplies Expense | 55 | 5,150 | ||

| Depreciation Expense-Truck | 56 | 4,000 | ||

| Insurance Expense | 57 | 3,150 | ||

| Miscellaneous Expense | 59 | 5,450 | ||

| (To close the revenues and expenses account. Then the balance amount are transferred to income summary account) | ||||

| January 31 | Income Summary | 34 | 46,150 | |

| Retained earnings | 32 | 46,150 | ||

| (To record the closure of net income from income summary to retained earnings) | ||||

| January 31 | Retained earnings | 32 | 3,000 | |

| Dividends | 33 | 3,000 | ||

| (To record the closure of dividend to retained earnings) | ||||

Table (11)

Service revenue account has a normal credit balance of $155,000 in total, now to close this account, the service revenue account must be debited with $155,000 and, income summary account must be credited with $155,000.

- In this closing entry, the fees earned account balance is being transferred to the income summary account, to bring the revenues account balance to zero.

- Thereby, the income summary account balance gets increased by $155,000 and, the revenue account balance gets decreased by $155,000.

All expenses accounts have a normal debit balance, the total of expenses are $108,850 have to be closed by transferring these account balances to the income summary account. All expenses account must be credited, and the income summary account must be debited with $108,850.

- In this closing entry, all the expenses account balances are transferred to the income summary account, to bring the expenses account balances to zero.

- Thereby, both the income summary account, and the expenses account balances get decreased by $108,850.

Determined amount balance of income summary is $46,150, which has to be closed by debiting the income summary account with $46,150, and crediting the retained earnings account with $46,150.

- In this closing entry, the income summary account balance is being transferred to the retained earnings account, to bring the income summary account balance to zero.

- Thereby, the income summary account gets decreased, and the retained earnings account balance gets increased by $46,150.

Dividends account has a normal debit balance of $3,000, now to close this account, retained earnings account must be debited with $3,000 and, dividend account must be credited with $3,000.

- In this closing entry, the dividend account balance is being transferred to the retained earnings account, to bring the dividend account balance to zero.

- Thereby, the retained earnings account balance gets increased by $3,000 and, the dividend account balance gets decreased by $3,000.

7.

To prepare: The post–closing trial balance of R interiors for the month ended January 31, 2018.

Explanation of Solution

Prepare a post–closing trial balance of R interiors for the month ended January 31, 2018 as follows:

|

R interiors Post-closing Trial Balance January 31, 2018 |

|||

| Particulars |

Account Number |

Debit $ | Credit $ |

| Cash | 11 | 13,100 | |

| Supplies | 13 | 2,850 | |

| Prepaid insurance | 14 | 4,350 | |

| Equipment | 16 | 113,000 | |

| Accumulated depreciation- Equipment | 17 | 17,250 | |

| Trucks | 18 | 90,000 | |

| Accumulated depreciation- Trucks | 19 | 31,100 | |

| Accounts payable | 21 | 4,500 | |

| Wages payable | 22 | 900 | |

| Common Stock | 31 | 30,000 | |

| Retained earnings | 32 | 139,550 | |

| Total | 223,300 | 223,300 | |

Table (12)

The debit column and credit column of the post–closing trial balance are agreed, both having balance of $223,300

Want to see more full solutions like this?

Chapter 4 Solutions

CengageNOWv2, 2 terms Printed Access Card for Warren/Reeve/Duchac’s Financial & Managerial Accounting, 14th

Additional Business Textbook Solutions

Managerial Accounting: Tools for Business Decision Making

Accounting for Governmental & Nonprofit Entities

Financial Accounting, Student Value Edition (5th Edition)

Fundamentals of Cost Accounting

Construction Accounting And Financial Management (4th Edition)

Introduction To Managerial Accounting

- Percent Uncollectible Age Class Balance Not past due 1-30 days past due 31-60 days past due 61-90 days past due 91-180 days past due Over 180 days past due $ 892,000 4% 285,000 1 101,000 8. 63,000 16 43,100 50 17,700 80 $1,401,800 a. Estimate what the total balance of the allowance for doubtful accounts should be as of December 31. b. Journalize the adjusting entry for uncollectible accounts as of December 31.arrow_forwardQuestion Content Area Determine the amount to be added to Allowance for Doubtful Accounts in each of the following cases and indicate the ending balance in each case. a. Credit balance of $460 in Allowance for Doubtful Accounts just prior to adjustment. Using the aging method, the balance of Allowance for Doubtful Accounts is estimated as $7,630. Amount added $fill in the blank 1 Ending balance $fill in the blank 2 b. Credit balance of $460 in Allowance for Doubtful Accounts just prior to adjustment. Bad debt expense is estimated at 2% of credit sales, which totaled $1,045,000 for the year. Amount added $fill in the blank 3 Ending balance $fill in the blank 4arrow_forwardPrêpare a Journal Entries for Accounts Receivables. Is not a graded question If can't the part B is : what would the year-end adjusting journal entry be given the following Allow to DA 375arrow_forward

- Fill in the blaknks: A debit entry of 150 to .................. blank........... and a credit entry to .........blank............... A debit entry of ................. blank.......... to ................. blank.......... and a credit entry to suppl The adjusting entries would include:A ................. blank..........entry of 400 to ................. blank.......... and a ................. blank.......... entry of 400 to b................. blank.......... The closing entries would involve a debit entry of ................. blank.......... to service revenue and a debit entry of 3600 to ................. blank..........arrow_forwardThe income statement and a schedule reconciling cash flows from operating activities to net income are provided below for Mike Roe Computers. MIKE ROE COMPUTERS Income Statement For the Year Ended December 31, 2021 ($ in millions) Sales $150.20 (90.10) Cost of goods sold Gross margin Salaries expense 60.10 $20.20 Insurance expense 12.20 Depreciation expense Interest expense 5.10 6.10 (43.60) Gains and losses: Gain on sale of equipment 12.20 Loss on sale of land (3.20) Income before tax 25.50 Income tax expense (12.75) $ 12.75 Net income Reconciliation of Net Income to Net Cash Flows from Operating Activities ($ in millions) Net income $ 12.75 Adjustments for noncash effects: Decrease in accounts receivable 5.10 Gain on sale of equipment Increase in inventory (12.20) (6.10) Increase in accounts payable Increase in salaries payable Depreciation expense 9.10 3.10 5.10 Decrease in bond discount 3.05 Decrease in prepaid insurance 2.10 Loss on sale of land 3.20 Increase in income tax payable…arrow_forwardUse the following items taken from the financial statements of the Postal Service for the year ending December 31, 2018 to answer questions: Accounts payable ..............................................................$10,000 Accounts receivable ............................................................11,000 Accumulated depreciation – equipment ..........................28,000 Advertising expense ............................................................21,000 Cash ......................................................................................14,000 Owner’s capital (1/1/18) ...................................................105,000 Owner’s drawings ...............................................................14,000 Depreciation expense ........................................................12,000 Insurance expense ...............................................................3,000 Note payable, due 6/30/19…arrow_forward

- Journalize the following transactions, using the direct write-off method of accounting for uncollectible receivables: Question Content Area Mar. 17. Received $325 from Shawn McNeely and wrote off the remainder owed of $500 as uncollectible. If an amount box does not require an entry, leave it blank. Date Account Debit Credit Mar. 17 - Select - - Select - - Select - - Select - - Select - - Select - Question Content Area July 29. Reinstated the account of Shawn McNeely and received $500 cash in full payment. If an amount box does not require an entry, leave it blank. Date Account Debit Credit July 29 - Select - - Select - - Select - - Select - July 29 - Select - - Select - - Select - - Select -arrow_forward1. What amount should be reported as accounts receivable on December 31?a. 1,300,000b. 1,426,000c. 1,280,000d. 1,220,000 2. What amount should be reported as allowance for doubtful accounts on December 31?a. 120,000b. 200,000c. 250,000d. 170,000arrow_forwardC. Aging Accounts Assume that accounts are aged from the date of billing. If you are aging accounts on 10/30/XX, select the letter of the correct length of time that each of the following accounts has been outstanding. a. Current (0 to 30 days) b. 31 to 60 days c. 61 to 90 days d. 91 to 120 days e. Older than 120 days 1. Service provided on 7/4/XX, billed on 8/1/XX 2. Service provided on 9/22/XX, billed on 10/3/XX 3. Service provided on 8/13/XX, billed on 8/22/XX 4. Service provided on 4/18/XX, billed on 4/25/XX 5. Service provided on 5/13/XX, billed on 6/6/XX 6. Service provided on 6/19/XX, billed on 7/12/XX 7. Service provided on 6/25/XX, billed on 7/18/XX 8. Service provided on 7/18/XX, billed on 8/15/XXarrow_forward

- om te x O Indian X Conten X O My App X Reset F X Cengag x O Mail -E X Indian m/ilm/takeAssignment/takeAssignmentMain.do?invoker=assignments&takeAssignmentSessionLocator=assignment-take&inpro.. Q < * * eBook Show Me How Providing for Doubtful Accounts At the end of the current year, the accounts receivable account has a debit balance of $6,800,000 and sales for the year total $81,500,000. a. The allowance account before adjustment has a debit balance of $68,250. Bad debt expense is estimated at % of 1% of sales. b. The allowance account before adjustment has a debit balance of $68,250. An aging of the accounts in the customer ledger indicates estimated doubtful accounts of $575,000. c. The allowance account before adjustment has a credit balance of $45,000. Bad debt expense is estimated at % of 1% of sales. d. The allowance account before adjustment has a credit balance of $45,000. An aging of the accounts in the customer ledger indicates estimated doubtful accounts of $450,000.…arrow_forwardThe following selected transactions are from Garcia Company. Year 1 Dec. 16 Accepted a $20,400, 60-day, 12% note in granting Rita Griffin a time extension on his past-due account receivable. 31 Made an adjusting entry to record the accrued interest on the Griffin note. Year 2 Feb. 14 Received Griffin's payment of principal and interest on the note dated December 16. 2 Accepted a $9,000, 6%, 90-day note in granting a time extension on the past-due account receivable from Wright Co. 17 Accepted a $7, 200, 30-day, 10% note in granting Wang Lee a time extension on her past-due account receivable. Mar. Apr. 16 May 31 Wright Co. dishonored its note. Aug. 7 Accepted a $22,000, 90-day, 10% note in granting a time extension on the past-due accourt receivable of Collins Co. Lee dishonored her note. 3 Accepted a $11,400, 60-day, 10% note in granting Maria Gonzalez a time extension on his past-due account receivable. 2 Received payment of principal plus interest from Gonzalez for the September 3…arrow_forwardMULTIPLE CHOICE 1. These represent open accounts with customers. a. Trade receivables b. Nontrade receivables c. Accounts receivable d. Notes receivables 2. Upon initial recognition, accounts receivable are measured at а. Face value b. Discounted value c. Maturity value d. Net realizable value 3. Trade receivables that are expected to be collected within 12 months after the reporting period shall be presented in the statement of financial position at a. Net realizable value b. Maturity amounts c. Face amounts d. Discounted values 4. Receivables denominated in a foreign currency should be a. Translated to local currency using the exchange rate at the time of recognition b. Shown at face value of the foreign currency c. Translated to local currency using the exchange rate at closing rate d. Translated to local currency using the exchange rate when the financial statements are authorized for issue 5. Which valuation allowance is a proper deduction from trade accounts receivable in…arrow_forward

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage